Key Takeaways

|

1chap3_p_1This chapter outlines a set of common considerations that underpin the effectiveness of the various financing instruments for health presented in this User Guide, including sustainability-linked financing (SLF), debt swaps and public-private partnerships (PPPs). Each component is based on international best practices and shaped by lessons from country experiences.

2chap3_p_2For Ministries of Health (MoHs), this chapter explains how to maximise the sectoral impact of financing by identifying priority interventions, strengthening reporting and monitoring systems and ensuring that health results remain central throughout the design process. For Ministries of Finance (MoFs), it emphasises the importance of fiscal prudence, debt sustainability and coherent integration into macroeconomic frameworks. Both institutions share the responsibility of ensuring that any innovative instrument aligns with the country’s institutional capacity, legal frameworks, debt-carrying capacity and broader development strategy.

3chap3_p_3Ultimately, success in health financing innovation depends on collaboration. The design of these instruments must build on, not bypass, national systems and processes. They work best when treated as an extension of sound governance and coordinated reform, not as isolated financial products.

4chap3_p_4By the end of this chapter, readers will understand the common factors that determine whether non-traditional and structured financing instruments, such as SLFs, debt swaps and PPPs, can achieve meaningful and lasting results in a particular country context. Success depends not only on financial design but also on how each mechanism strengthens national systems, aligns with fiscal and health priorities and fosters institutional learning.

Prioritising Health Financing Impact

5chap3_p_5Financing instruments are most effective when financial innovation is matched with strategic alignment. The goal is not simply to mobilise new resources for health, but also to ensure that all funds raised deliver measurable and lasting results. This requires clear linkage to national health strategies, well-defined activities and realistic assessments of financing needs and absorptive capacity.

6chap3_p_6Every transaction should begin with clarity on the health priorities it will support and how the proceeds will be used. These priorities must be anchored in existing national plans or sectoral strategies, transparently costed and matched with a financing mechanism suited to their scale, purpose and timeline.

7chap3_p_7Governments also need credible data and reporting systems to meet the accountability standards tied to these instruments. Where national data systems are still maturing, temporary reliance on established global or regional platforms may be appropriate, but should be paired with efforts to build domestic capacity for tracking both financial and health outcomes. Over time, this ensures that financing arrangements strengthen country systems rather than create parallel ones.

8chap3_p_8For sustainability-linked financing, the careful selection of key performance indicators (KPIs) is essential. Indicators must be measurable, meaningful and achievable - ambitious enough to drive results, but realistic enough to be credible. Well-designed KPIs enhance confidence and attract further investment; weak or superficial ones erode both confidence and investment.

9chap3_p_9The MoH has a vital advocacy role in securing an appropriate share of funds for health within debt or SLF arrangements. Together, MoHs and MoFs must assess the full cost of each mechanism, including the overall costs and expenses of the transaction at inception (including advisory, legal and third-party fees), ongoing costs and expenses and debt servicing costs, to ensure that the net fiscal and health benefits justify the investment.

10chap3_p_10Ultimately, the measure of success is not the volume of financing mobilised, but whether the application of such funding strengthens, sustains and makes health systems more equitable and resilient over time.

11chap3_p_11For more detailed information on KPIs and health systems, see Chapter 4: Health Finance and Key Performance Indicators.

Managing the Fiscal and Debt Implications of Financial Instruments

12chap3_p_12Before considering sustainability-linked or health-related financing, debt management offices (DMOs) must first ensure these instruments fit within the annual borrowing plan defined in the national budget and align with the national Medium-Term Debt Strategy (MTDS). Indeed, potential instruments need to be assessed against the country’s financing needs as well as its debt management objectives, including impact on refinancing risk, interest rate risk and foreign currency risks.

13chap3_p_13DMOs also need to assess, ex ante, the overall impact of the financing instrument on public debt sustainability in the context of the country’s debt carrying capacity. This will often involve modelling debt sustainability analysis (DSA) scenarios reflecting the target structure of the contemplated instruments. This analysis will inform the range of acceptable terms, including the total amount of funding to be raised, acceptable interest rates (and, in this context, whether third-party credit support would be beneficial) and repayment periods. For PPPs, a contingent liability risk assessment enables the safeguarding of longer-term fiscal and debt sustainability.

14chap3_p_14Exploring credit-enhancement mechanisms will be crucial to improving terms and reducing funding costs for borrowers. However, as these solutions often come with additional expenses, such as guarantee or insurance premiums, performing a comprehensive cost assessment is essential to determine whether the participation of credit enhancement providers lowers the overall costs of funding (see also Chapter 8: Credit Enhancement). In some cases, philanthropic or concessional capital can be mobilised to cover these premiums, partially or entirely. In the case of loan-based financing, running a competitive and transparent selection process among several international lenders can also help optimise pricing and terms.

15chap3_p_15While these instruments generally signal a strong commitment to macroeconomic fiscal sustainability, governments must remain alert to potential credit perception risks. For instance, some commercial debt swaps could be classified by rating agencies as distressed exchanges, where low-rated countries buyback bonds in the capital markets as part of a debt swap under liquidity stress. Early engagement and transparent communication with rating agencies is therefore essential to understand the rating methodologies of the respective rating agencies and their implications for the proposed debt swap.

16chap3_p_16Finally, countries need to ensure that the proposed transaction aligns with their existing country programmes and those of multilateral development institutions. For example, if the government is supported under an International Monetary Fund (IMF) programme, it is essential to ensure the transaction complies with the agreed-upon programme parameters and conditionalities.

Regulatory and Institutional Framework Alignment

17chap3_p_17When selecting financing instruments, it is crucial to ensure their alignment with the country’s statutory, legal, regulatory and institutional frameworks, thereby ensuring both effectiveness and sustainability.

18chap3_p_18All contracts and agreements should be duly authorised; legal, valid, binding and enforceable under national law as well as any applicable foreign law. They should clearly articulate the roles and responsibilities of the parties involved, their performance obligations, remedies for breaches, including any default or termination rights and incorporate an agreed-upon governing law and dispute resolution mechanism. This means that any proposed sustainability-linked instruments, debt swaps or PPP contracts should be permitted under existing frameworks or that such frameworks may need to be amended or supplemented.

19chap3_p_19Compliance with debt, fiscal and procurement laws should therefore be looked at critically. Debt instruments under consideration should fall within the limits and procedures established by relevant public finance management acts, debt management laws and public procurement frameworks. Some countries may require parliamentary and/or Cabinet approval, as well as listing in national budgets. Early consideration should be given to the approvals needed.

20chap3_p_20To address transparency and accountability issues, instruments should incorporate disclosure, auditing and oversight provisions to meet both domestic and international standards, as applicable in each case. Abiding by budget transparency principles or sectoral transparency tools (e.g. national health accounts) is also essential.

21chap3_p_21Whether through sustainable finance instruments, debt-for-health swaps or PPPs, governments should align disclosure practices with recognised international standards - such as the relevant International Capital Market Association (ICMA) and Loan Market Association (LMA) Principles for bonds and loans or the World Bank PPP Disclosure Framework for partnerships. This entails publishing key transaction terms, establishing appropriate governance and management of the funds raised, as well as regular performance and spend reports, capable of verification by independent reviewers when necessary. This can help trace how resources are mobilised, allocated and translated into measurable health outcomes.

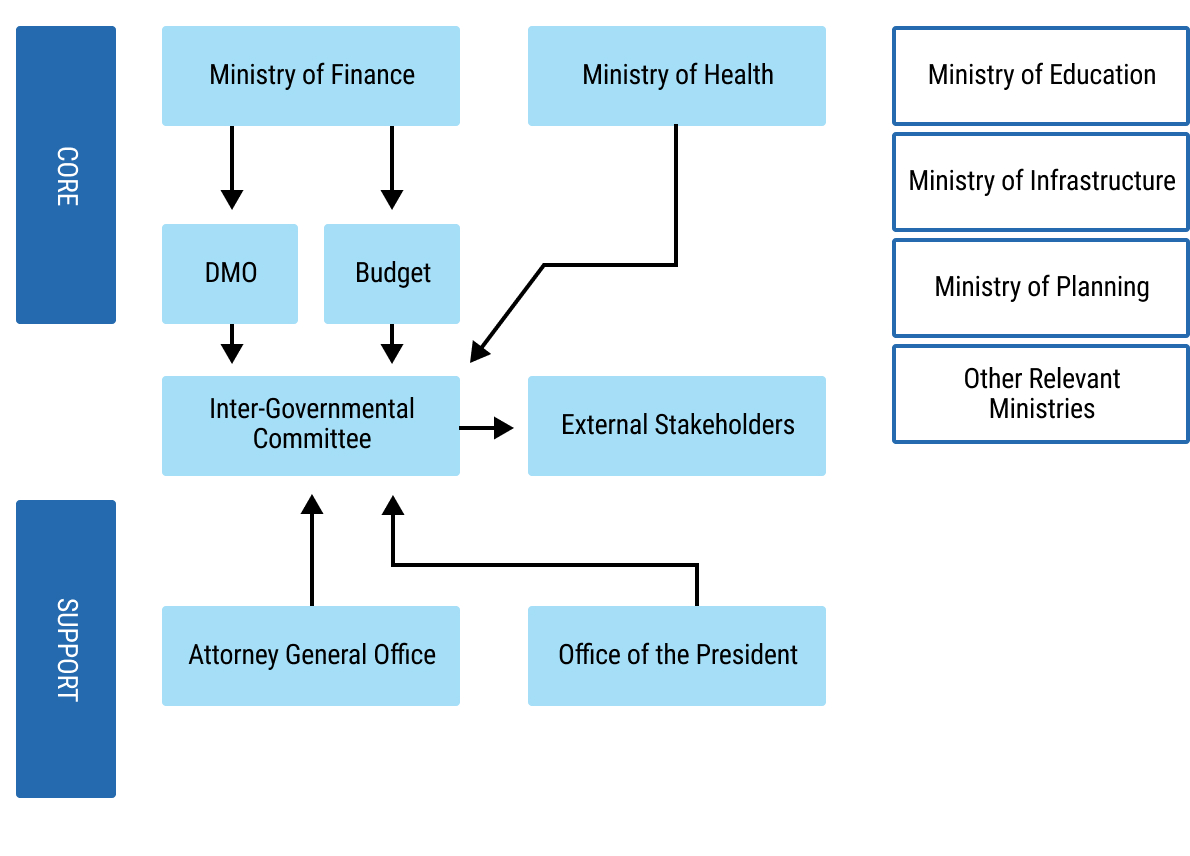

22chap3_p_22Institutional capacity is another critical dimension: both lead ministries need adequate technical skills, operational systems, and coordination mechanisms to evaluate, manage and monitor the funding instruments and related contractual arrangements. Clarifying the roles of the MoF, specifically their existing debt management office or PPP unit, and that of the MoH, is critical, especially regarding who leads negotiations, execution and ongoing monitoring.

Intra-governmental Coordination

23chap3_p_23Every non-traditional and structured financing transaction, whether an SLF instrument, a debt swap or a PPP, cuts across fiscal, legal and sectoral mandates. Collaboration between ministries and agencies is therefore indispensable, not only for technical soundness but also for political and operational coherence.

24chap3_p_24The MoF and MoH should work together from the outset, jointly defining objectives, suitability of funding type, timelines and communication strategies. The MoF typically leads negotiations with banks, credit enhancement providers and investors, ensuring alignment with the country’s debt management strategy, budgetary cycle and the necessary technical expertise. Meanwhile, the MoH ensures that proposed activities are grounded in national health priorities and that health outcomes remain visible throughout the process. Suppose the transaction involves a third party implementing agreed health spend outcomes or programmes. In that case, the MoH should also lead on these aspects and the structure of any ongoing monitoring and reporting activities.

25chap3_p_25Because ministries have different mandates, each must see the value of the transaction through its own lens. The lead ministry should therefore frame messages in terms of the specific problems or concerns each counterpart is trying to solve, whether debt servicing elements for the MoF, service delivery performance for the MoH or legal safeguards for the Attorney General’s Office. This approach strengthens ownership and minimises resistance as discussions evolve.

26chap3_p_26Relevant MoF officials should include officials from the DMO and budget departments. In contrast, MoH representatives should consist of the Permanent Secretary, Head of Planning and relevant directorate leads, depending on the health programme or intervention being financed.

27chap3_p_27Other key public institutions may include:

- chap3_ul_1

- chap3_li_6The Office of the President or the Cabinet Office provides political backing and facilitates high-level decision-making.

- chap3_li_7The Attorney General’s Office ensures the transaction complies with national laws and provides legal opinions required as part of the transaction.

- chap3_li_8The Ministry of Planning and/or Economy aligns the transaction with national development priorities.

- chap3_li_9The National Statistics Office supports credible, timely and accurate reporting.

- chap3_li_10The Central Bank ensures consistency with foreign exchange management and monetary policy objectives.

- chap3_li_11The Ministry of Foreign Affairs is consulted specifically regarding bilateral debt swaps with other countries.

- chap3_li_12National health sector regulators are responsible for regulatory oversight, standards-setting, licensing, and compliance across the health system.

28chap3_p_28To support effective coordination across all stages of the transaction, countries may establish a dedicated intergovernmental committee with representatives from key institutions. The composition of this committee should reflect each country’s governance context, as there is no single model that fits all. For example, while the Office of the President may be listed here as a source of political support, in some countries, its early involvement is crucial to securing high-level buy-in and sustaining momentum. In other countries, the Office of the President has, through advisors, actually driven the transaction.

29chap3_p_29The list of potential members provided in this User Guide is therefore indicative, not prescriptive. Countries should adapt it to include any additional ministries, agencies or oversight bodies relevant to their context. To prevent duplication or reputational risk, the MoF and MoH should coordinate all external engagement through this mechanism, ensuring consistency, transparency and a unified national voice.

chap3_img_0

chap3_img_0External Stakeholder Engagement

30chap3_p_30In addition to inter-governmental coordination, early and regular engagement with the various external parties involved in the transaction can enhance credibility, mitigate political and reputational risk and reinforce the development impact.

31chap3_p_31Relevant external stakeholders encompass international institutions, the private sector and civil society actors. The engagement process would benefit from identifying dedicated officials within the intergovernmental coordination committee to engage with external partners regarding the envisaged transaction. These officials could include, for example, one person from the MoH and one from the MoF.

32chap3_p_32The following partners would need to be engaged, depending on the type of instrument and each at different parts of the process:

- chap3_ul_2

- chap3_li_13Global health institutions and partners can support activity design and implementation, including monitoring and reporting.

- chap3_li_14Banks and private investors would need to be tested to assess their appetite for the transaction and structure the financial parameters.

- chap3_li_15Credit enhancement providers can critically enable some of the financing structures presented in this User Guide. They can assess the feasibility of different financing structures, specify the availability of specific products and discuss the terms and conditions of their support.

- chap3_li_16Foreign governments, when considering bilateral debt swaps.

- chap3_li_17The IMF, the World Bank and other multilateral partners can ensure that the transaction aligns with the country’s programme objectives, if relevant, and, in the case of the IMF and World Bank specifically, is consistent with their debt sustainability assessments.

- chap3_li_18Credit rating agencies will need to be brought on board early to share relevant information and understand credit rating considerations.

- chap3_li_19Engaging private sector companies early on is crucial for PPPs to ensure early market sounding and transparent procurement, thereby attracting qualified operators and financiers.

- chap3_li_20Civil society organisations can input on the objectives of the transaction and help socialise the positive impact of the transaction.

- chap3_li_21The media can help ensure accurate reporting on the transaction and its health benefits.

Transparency and Communication Management

33chap3_p_33How governments communicate around financing mechanisms can be as important as the design of the mechanisms themselves. In the early stages, careful control of information is essential. Premature or poorly coordinated announcements can be easily misinterpreted by markets, creditors or rating agencies, potentially creating reputational, market and fiscal risks.

34chap3_p_34Confidentiality during the exploration and negotiation phases of any transaction allows the government to refine its proposal, align internal stakeholders and shape the narrative before it enters the public domain. Such confidentiality is vital in the case of commercial debt swaps involving the potential buyback of publicly traded bonds, as any announcement of a transaction could lead to a rally in the country’s bond prices, resulting in reduced fiscal savings from the debt swap. Once the design is finalised, transparency should take precedence. Public communication should focus on the transaction’s purpose, its alignment with national priorities and the mechanisms for accountability and reporting.

35chap3_p_35Effective communication strategies build confidence, both domestically and internationally. They signal that the government is managing innovation responsibly, safeguarding fiscal stability and ensuring that citizens and partners understand the rationale for new approaches to financing health.

36chap3_p_36Ideally, communication should evolve with the process: discreet and coordinated in early stages, open and transparent once agreements are finalised.

Building Country Ownership and Learning

37chap3_p_37The true legacy of any financing transaction should be a stronger national capacity. Beyond mobilising additional funds, each transaction provides an opportunity to build institutional knowledge, refine systems and strengthen governance.

38chap3_p_38Governments should document lessons learned, develop best practices, create templates and retain experienced teams to create continuity for future transactions. Over time, this institutional learning reduces transaction costs, accelerates timelines and increases national autonomy in managing complex financial instruments.

39chap3_p_39Every transaction, regardless of size, should therefore be seen not only as a means of mobilising resources but also as an investment in institutional capability. When capacity grows, credibility follows, and with it, greater access to sustainable financing opportunities in the future.

|

40chap3_p_40Debt management is consolidated at the DMO and governments should ensure that any fundraising, whether for health or other policy objectives, follows international best practices in public debt management. To support this, the IMF and World Bank have developed a set of voluntary principles to help debt managers strengthen institutional frameworks and reduce financial vulnerability. The key principles are summarised below:

41chap3_p_41For more details, the reader is referred to the Guidelines for Public Debt Management (2014) by the World Bank and IMF. |