Key Takeaways

|

1chap8_p_1This chapter outlines the various credit enhancement mechanisms that may be used in the three instruments described in this User Guide: sustainable finance instruments, debt-for-health swaps, and health public-private partnerships (PPPs) and explains how these mechanisms strengthen the bankability and overall feasibility of health financing transactions.

What is Credit Enhancement, and Why is it Important?

2chap8_p_2Broadly, credit enhancement can be defined as a financial mechanism designed to improve the creditworthiness of a borrower or a specific transaction and includes, among others, guarantees and guarantee-like instruments, insurance, or a combination thereof. As their primary purpose is to share and/or mitigate risk, thereby improving financing terms (including new financing sources, larger volumes, longer tenors, grace periods, and more favourable pricing), these mechanisms play a key role in unlocking financing for governments.

Credit Enhancement for Sustainable Finance Instruments and Debt Conversions

3chap8_p_3In the sovereign finance context, credit enhancement may be provided by multilateral development banks (MDBs), DFIs, ECAs, or private insurers. Sustainable finance instruments can benefit from various forms of credit enhancement, including (i) partial credit guarantees, (ii) political risk insurance, and (iii) collateralisation.

In PPPs exposed to political risks, such as the risk of non-payment by a government or a government-owned entity, or breach of contracts, MDBs also offer partial risk guarantees (PRGs) on government obligations to encourage lenders and investors to participate. In each case, the financial structure and the choice of credit enhancement mechanism need to be tailored to the specific context. In the case of sustainability-linked loans (SLL) and debt swaps, the credit enhancement mechanism needs to reflect the country’s financial situation, implementation capacity, and policy objectives. For health PPPs, credit enhancement mechanisms are informed by the project type and model. Note that there is a growing trend to combine multiple credit enhancement mechanisms to maximise coverage and further reduce the overall cost of financing operations.

4chap8_p_4The following details the most standard credit enhancement tools used in sovereign sustainable finance transactions:

1. Partial Credit Guarantees

Description and Rationale

5chap8_p_5PCGs provide an irrevocable and unconditional commitment from a guarantor to cover a specified portion of scheduled debt service in the event of default by the borrower or issuer. They can be structured to cover any category of risk that could trigger a payment default, including credit or project-related risks. This type of credit enhancement enables the instrument to benefit from the guarantor’s higher credit rating, resulting in more favourable financing terms, such as lower interest rates, longer maturities, and larger financing volumes. In Africa, PCGs for sovereign or sovereign-guaranteed borrowers could be offered by multilateral and regional development banks such as the African Development Bank (AfDB), the World Bank Group through its new guarantees platform, the European Investment Bank (EIB), Asian Infrastructure Investment Bank (AIIB), the African Export-Import Bank, Africa Finance Corporation and others. Other development finance institutions, such as GuarantCo, focus their PCGs on supporting private sector borrowers, including project companies in PPPs and sub-national entities.

6chap8_p_6Within the broad category of PCGs, there are investment guarantees, which support a specific project, and policy-based guarantees, which are linked to the implementation of agreed policy reforms by a sovereign. PCGs can also take the form of portfolio guarantees when they cover a portfolio of transactions (for instance, a PCG can cover a portfolio of loans to health institutions to be constituted by a lender). Another form of PCG is the transaction guarantee offered by the AfDB to support trade transactions specifically (such as the import of medical equipment).

Rationale

7chap8_p_7Under PCGs, and in the context of a loan or bond, the lenders or bondholders benefit from a guarantee agreement with one or more guarantors, who undertake to cover a defined portion of scheduled debt service payments in the event of default by the borrower. The borrower, in turn, typically enters into a counter-indemnity agreement with the guarantor, under which it commits to reimburse the guarantor for any amounts paid under the guarantee.

8chap8_p_8To increase the PCG amount they can provide, MDBs can utilise a guarantor-of-record structure, where risk participants, including co-guarantors and credit insurers, can participate in the exposure while the MDB fronts the guarantee.

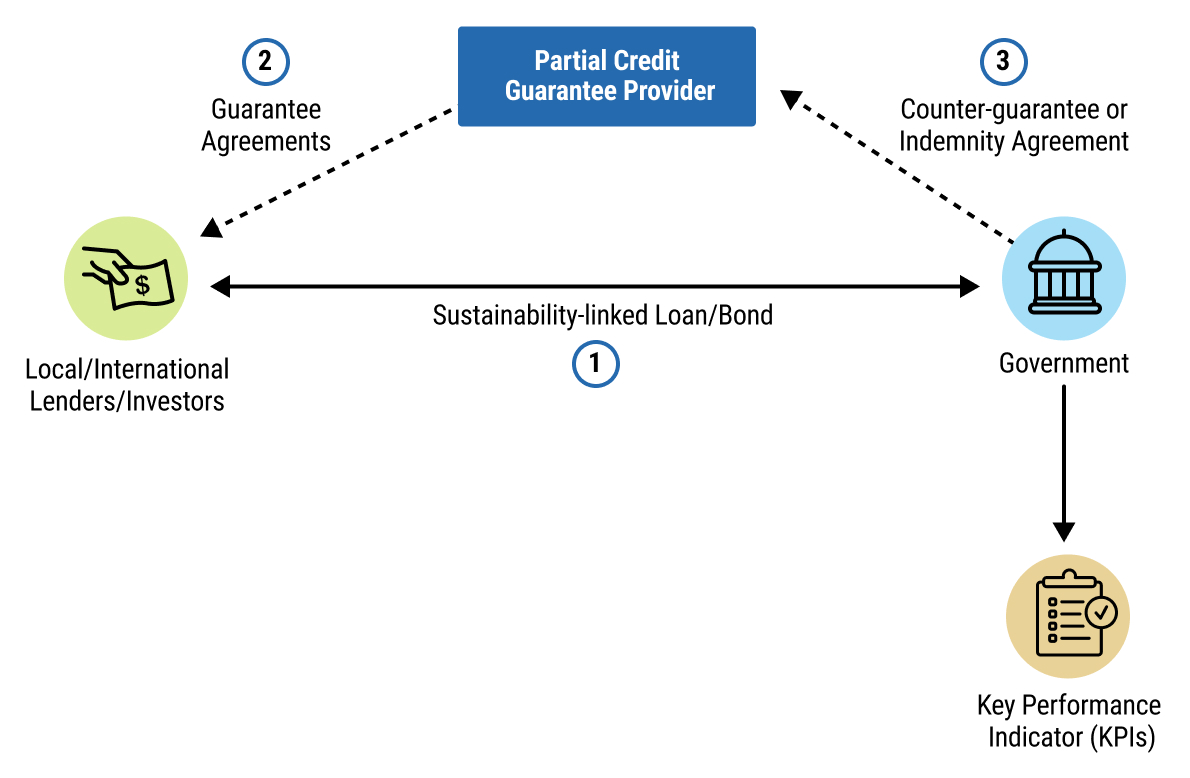

9chap8_p_9Figure 8.1 represents the financial structure of a sustainable loan with a PCG. Refer to Chapter 4: Health Finance and Key Performance Indicators for a detailed discussion of sustainable finance instruments.

chap8_img_0

chap8_img_0

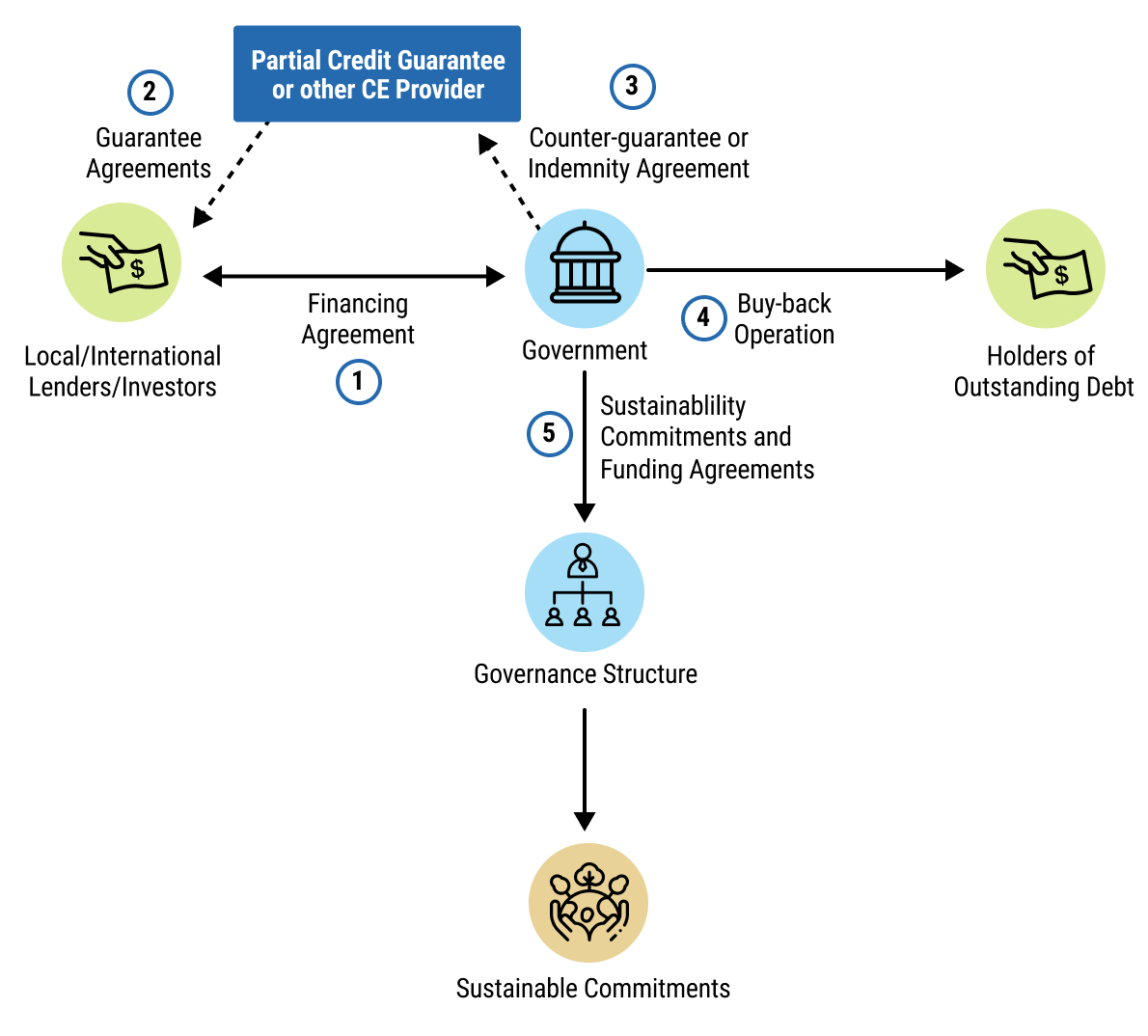

10chap8_p_10In the context of a commercial debt-for-health swap (also known as debt conversion), credit enhancement is used to de-risk the new-money transaction and attract private investors by partially or fully guaranteeing payments under the new debt instrument. As such, the credit enhancement will cover only the debt being issued to finance the buyback. The government will utilise the proceeds from the newly issued, credit-enhanced debt to retire outstanding, and/or more expensive discounted debt, thereby generating fiscal savings that will be used to fund agreed-upon health sector investments or programmes. Refer to Chapter 5: Sustainable Finance Instruments for a detailed discussion of debt conversions.

chap8_img_1

chap8_img_111chap8_p_11Notably, in recent debt conversions, PCGs have often been combined with PRI, other public or private co-guarantees, or private credit insurance instruments to mobilise additional private capital and enhance the scale and developmental impact of the transactions.

12chap8_p_12PCGs can support governments, government-owned entities and private sector entities in their debt mobilisation efforts to fund healthcare projects.

2. Political Risk Insurance

Description and Rationale

13chap8_p_13PRI can protect investors against non-commercial risks such as expropriation, currency inconvertibility, political violence, breach of contract by a government or state-owned entity, or sudden regulatory changes. For example, the U.S. DFC provides PRI that explicitly covers losses resulting from the borrowing country’s non-payment of a final and binding arbitral award and from denial of access to justice. In Africa, PRIs are provided by multilateral institutions such as the World Bank Group’s MIGA, DFIs such as African Trade and Investment Development Insurance, and private insurers.

14chap8_p_14Unlike PCGs, which are generally unconditional, PRI payouts are contingent on predefined political events that must be verified. Because the payout may be linked to the conclusion of a lengthy process, such as international arbitration, PRI may be combined with guarantees or collateralisation to ensure continuity of payments. In contrast, the arbitration is being pursued to maintain investor confidence. Providers of PRI may not require counter-guarantees but will seek to have subrogation rights (I.e. the right of the insurer to step into the shoes of the insured party and to recover from any third party responsible for the loss) - I.e. the credit enhancement provider steps into the investor’s shoes in respect of the right to recover amounts covered by the PRI.

Rationale

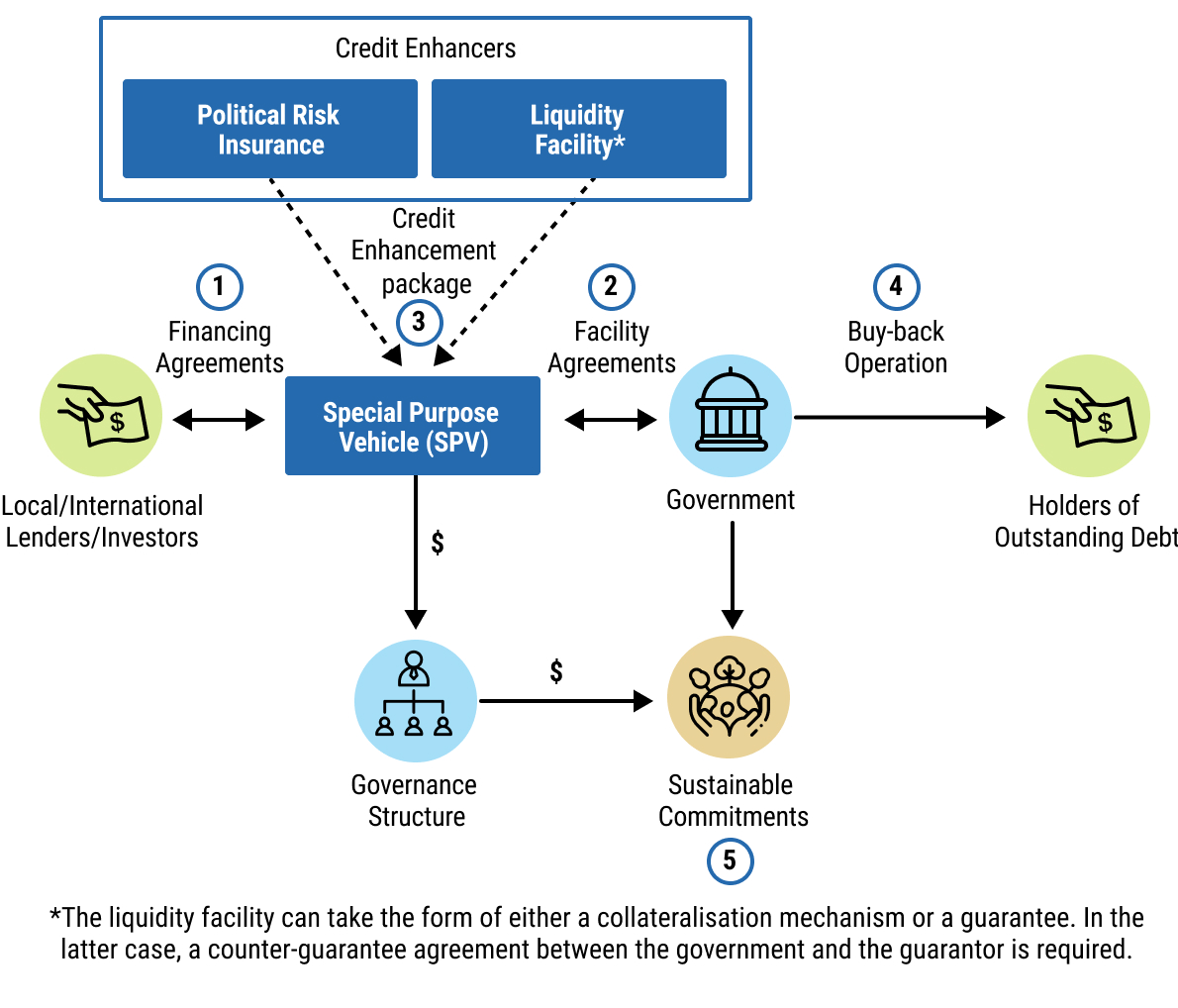

15chap8_p_15A common practice in debt conversions has been to establish an SPV to issue bonds to investors or enter into a loan agreement with lenders. The SPV will then on-lend the proceeds through a new loan agreement with the government. This new lending arrangement may be credit-enhanced by a PRI that covers the loan principal amount and will often be combined with a liquidity guarantee, ensuring that interest payments will still be made to investors prior to the policy paying out.

For example, when the policy covers failure to pay an arbitral award, the liquidity guarantee would cover any interest payments incurred during the arbitration proceedings. This liquidity guarantee could be established as a PCG or as a collateralisation mechanism, where specific assets or cash are set aside as security.

chap8_img_2

chap8_img_2

3. Collateralisation

Definition and Rationale

16chap8_p_16A collateralisation mechanism is a way to set aside certain of the borrower’s assets or revenue stream that can be used to repay lenders if the borrower is unable to meet its repayment obligations. Government assets that generate stable or predictable income (e.g. export proceeds, tax revenues, or project-related cash flows) or the income itself can serve as collateral. This provides additional comfort to lenders and typically improves borrowing terms.

17chap8_p_17These mechanisms can be employed to back a guarantee for a portion of transactions or ensure debt service payments in the event of a default. Collateralisation of a guarantee gives creditors rights over a guarantor’s or borrower’s asset(s) or revenue stream that, in the case of default, could allow the creditor to secure repayment of the debt.

Rationale

18chap8_p_18Where collateralisation is used, the borrower and its creditors will enter into agreements that define the rights and obligations related to the pledged assets, including enforcement rights, such as a collateral or security agreement.

19chap8_p_19From a legal standpoint, the borrower must avoid breaching any negative pledges to which they may be bound under the underlying contractual agreement (such as those imposed by the World Bank or other relevant entities providing credit enhancement). From a fiscal standpoint, collateralised loans represent contingent liabilities that need to be disclosed and accounted for, with a potential impact on debt sustainability. Revenue collateralisation may limit budget flexibility if the collateral is called upon.

4. Partial Risk Guarantees (PRGs)

Definition and Rationale

20chap8_p_20PRGs cover a private project in relation to relevant government or government-owned entity undertakings and/or politically-related risks vis-à-vis the project and not genuine commercial risks. Government undertakings towards a private project can be of a financial or non-financial nature, and these undertakings shall be clearly defined in contracts between the government and the private project or its sponsor. A PRG can attract investments (debt and/or equity financing) in project finance transactions where a project’s success depends as much on government undertakings as on private commercial acumen. In public-private partnerships, PRGs can assure private partners and commercial financiers that the government will fulfil its obligations to the partnership.

Rationale

21chap8_p_21Risk coverage under the PRG can be requested for protection against political risks such as non-payment, breach of contract, currency inconvertibility or confiscation/expropriation. These are mainly the same as those covered under PRIs. However, unlike PRIs, PRGs do not require an arbitration process. Following non-payment by the government or a government-owned entity, the guarantee can be called immediately upon expiration of any agreed-upon waiting period.

22chap8_p_22Similar to PCGs, PRGs generally require a sovereign counter-indemnity, where the country commits to repay any amount paid by the guarantor under the guarantee. However, some MDBs, such as the AfDB, can provide both PCGs and PRGs without sovereign counter-indemnity, provided the guarantee is commercially priced.

23chap8_p_23The PRG can support a project mainly through two types of structures: (i) PRG with a deemed loan provided to the beneficiary for protection against termination risk and (ii) PRG with a standby letter of credit for protection against temporary liquidity shortfalls from the government or a government-owned entity.

chap8_img_3Combining Credit Enhancement Sources

24chap8_p_24Credit enhancement instruments provided by MDBs and DFIs may also be combined with private sector credit enhancement, thereby strengthening the credit profile of the underlying transaction and further improving finance terms.

25chap8_p_25A notable example of blended credit enhancement is Côte d’Ivoire’s inaugural SLL issued in 2025, which combined two distinct MDB products: a policy-based guarantee from the World Bank Group’s International Bank for Reconstruction and Development (IBRD) and a non-honouring of sovereign financial obligations guarantee from MIGA. This innovative structure provided AAA-rated coverage for 95% of the loan, significantly reducing the all-in cost of borrowing and enhancing investor confidence.

26chap8_p_26The following outlines how private sector instruments can complement MDB and DFI credit enhancement support.

Private Sector Insurance

27chap8_p_27Private insurers increasingly participate in sovereign transactions by covering a portion of the payment risk related to sovereign or sub-sovereign obligations through credit insurance policies, reinsurance arrangements, or co-insurance structures, especially when MDBs or DFIs provide anchoring guarantees and first-loss protection. This is beneficial to all parties involved as it allows lenders and development institutions to reduce risk exposure and free balance sheet capacity, enables insurers to diversify into underrepresented markets, and signals investor confidence, which ultimately improves pricing.

Private Investors as Co-guarantors

28chap8_p_28High-net-worth investors are increasingly well-positioned to share sovereign risk alongside traditional guarantors. This approach was demonstrated in the 2024 Bahamas debt-for-nature swap, where Builders Vision provided a USD 70 million co-guarantee alongside the Inter-American Development Bank (IDB) and AXA XL, an insurance and reinsurance company. This is the first example of a private investor providing credit enhancement for a sovereign debt swap transaction. Recent initiatives include the Private Credit Enhancement Facility (PCEF) by Enosis Capital, a pooled credit enhancement facility for family offices and foundations, aiming to scale the successful example of impact investor participation in sustainability-linked financing (SLFs). The PCEF is designed as a USD 1 billion facility focused on emerging market and developing economies (EMDEs), offering guarantees to share risk alongside MDB-backed transactions. Funders, including family offices, foundations, and endowments, have the option to pledge a portion of their fixed-income portfolios as collateral, retaining ownership unless a default occurs. The structure enables funders to maintain the underlying asset yield and earn a deployment premium while amplifying the impact on nature and climate outcomes.

Credit Rating Implications

29chap8_p_29Credit ratings play a critical role in determining the effectiveness and market impact of credit enhancement mechanisms. Enhancements provided by highly rated entities, such as MDBs or DFIs, can materially improve the perceived credit quality of sovereign or sub-sovereign borrowers by blending their ratings with those of the credit enhancer. It is essential to acknowledge that particular challenges exist in this regard, including uncertainty regarding how credit rating agencies and regulatory frameworks evaluate credit-enhanced instruments, particularly with respect to partial coverage and the treatment of first-loss coverage from the perspective of the credit enhancement provider. Nonetheless, it remains that well-structured credit enhancement mechanisms can improve investor confidence and improve financing terms.

Credit Enhancement for Health PPPs

30chap8_p_30Credit enhancement plays a crucial role in mitigating risk in health PPP transactions. Similar to the above, credit enhancement mechanisms in the PPP context help improve creditworthiness, which in turn enhances financing terms, thereby allowing governments to attract private investment at lower costs. As will be discussed in more detail in this section, credit enhancement can either come from external sources, such as multilateral, regional or national institutions, or from the government itself, through contractual commitments or government support mechanisms. The appropriate form of credit enhancement will depend, among other factors, on the project’s risk profile and the degree of comfort required by lenders and investors.

External Credit Enhancement

31chap8_p_31External credit enhancement in PPPs involves instruments provided by third-party institutions, such as MDBs, ECAs, DFIs and insurers. These entities use their stronger credit rating to share or absorb project risks that the government or investors would otherwise bear.

32chap8_p_32Standard external credit enhancement mechanisms include PRGs and PRI as described above.

Government-provided Credit Enhancement

33chap8_p_33Government-provided credit enhancement involves contractual commitments or financial arrangements made directly by the government to assure the private partner under the PPP contract and lenders. These instruments vary in the level of fiscal exposure they create, ranging from unconditional guarantees (the highest commitment level) to letters of support (lower commitment level). This subsection will review the two most prominent government-provided credit enhancement mechanisms found in the health PPP context.

1. Sovereign guarantees

Description and rationale

34chap8_p_34Sovereign guarantees may take various forms and can be provided in favour of multiple participants in a health PPP project (for example, to the private partner under the PPP contract or to lenders).

35chap8_p_35Sovereign guarantees typically cover the risk of non-payment and/or the risk of non-performance of other obligations. Of course, when considering the role of a government as a guarantor, it is more likely that the guarantee covers non-payment risks, as it may not have the means to fulfil (or procure the fulfilment of) other types of obligations.

36chap8_p_36It should be noted that, in some jurisdictions, providing a sovereign guarantee is not permitted under law. In such cases, alternative methods for giving comfort to the private partner under the PPP contract or lenders should be considered.

Rationale

37chap8_p_37Non-payment guarantees may relate directly to loans (to protect against debt service defaults, and which will be provided in favour of lenders) or to other payment obligations (which are not loan-related, and which will be provided in favour of the relevant private partner under the PPP contract). An example of the latter would be a guarantee regarding an off-taker’s payment obligations, or a guarantee that the revenue for a project will at least meet a certain minimum level.

38chap8_p_38A government may offer a sovereign guarantee in respect of a PPP project to enhance the project’s financial viability and bankability for lenders. The presence of a sovereign guarantee can also help to attract private sector investment, in particular foreign investment, as the private partner under the PPP contract is assured that the project has the backing of the government, which helps to mitigate the perceived risks the private sector would otherwise potentially not take on.

39chap8_p_39However, given that sovereign guarantees create potential liabilities for governments, the necessity of granting a sovereign guarantee must be reviewed on a case-by-case basis to assess whether issuing a sovereign guarantee is necessary and appropriate. Sovereign guarantees should not be provided as a matter of routine for all projects, and governments should carefully analyse the level of risk they are taking on, on a project-specific basis.

40chap8_p_40The terms of any sovereign guarantee need to be carefully considered, and the government’s exposure to liability under the terms of the sovereign guarantee should be limited as far as possible. Additionally, when providing a sovereign guarantee, a government must consider the treatment of this guarantee for accounting purposes, as it may be recorded as a contingent liability on its balance sheet.

2. Letters of Comfort

Description

41chap8_p_41The host country provides a letter of comfort in which it promises to facilitate a project through, for example, facilitating certain approvals required for project implementation. Such a letter may be provided in place of a government guarantee where the guarantee would require parliamentary or constitutional approval or where granting a guarantee would negatively impact the sovereign’s debt sustainability levels.

Rationale

42chap8_p_42A letter of comfort does not establish a legally binding obligation; rather, it reflects the sovereign’s intent to support the project. As such, this type of credit enhancement provides a lower level of protection for the lender or investor.

43chap8_p_43Where applicable, the letter should address the lender’s areas of concern regarding the PPP project.

44chap8_p_44In some cases, a government letter may be enhanced to include firm undertakings, transforming the letter into a legally binding obligation.

3. Letters of Support

45chap8_p_45A letter of support is a government instrument issued to a private party, providing assurances that the government will cover certain political, legal, and regulatory risks. The scope of coverage typically varies from country to country. It is, however, not a sovereign guarantee.

4. Other Types of support

46chap8_p_46Governments can also offer other forms of support, such as providing grants or subsidies for a PPP project, tax breaks, or customs exemptions. Often, a combination of measures is taken.

47chap8_p_47In addition, contract terms (e.g. indemnities and compensation on termination) can also be used to provide relief in the event of specific risks, as opposed to covering those risks through a sovereign guarantee. Please note that contractual indemnities from governments attract the same contingent liability issues as sovereign guarantees. For detailed description of contingent liabilities, please see Understanding Sovereign Debt: Options and Opportunities for Africa

5. General Considerations

48chap8_p_48It is essential when considering credit enhancement to understand the expenses the credit enhancement provider expects the sovereign to cover, the premium payment to be paid, and the timing of such payments. Understanding the legal basis upon which such credit enhancement is to be provided will also be important, especially any recovery routes that the credit enhancement provider will require (e.g. counter-guarantees/indemnities, subrogation rights, transfers/assignments of commitments, etc.). Credit enhancement providers will also have specific participation conditions, and understanding these early on in the transaction structuring process will be helpful. They will also have their own internal approval processes for participation in any transaction, and these should be factored into the project timeline.