Key Takeaways

|

1chap6_p_1This chapter aims to guide officials from Ministries of Finance (MoFs) and Health (MoHs), as well as practitioners, through the design and implementation of debt-for-health swaps, which provide a powerful tool to unlock fiscal savings for health objectives. The chapter emphasises that the decision to pursue a debt swap, as well as the choice of debt swap type (bilateral versus commercial, bond versus non-bond, international versus domestic), must be informed by country-specific debt profiles, fiscal objectives and health sector priorities. Each section provides a practical framework to support this decision-making process, outlining the key steps for structuring and executing successful transactions.

Fiscal Savings for Health Objectives

2chap6_p_2Debt swaps are emerging as a financial tool that can help progress towards achieving universal health coverage (UHC) in a context of narrowing fiscal space and increasing debt service pressures, through a dual impact of unlocking additional long-term health funding and reducing debt burdens. MoFs have traditionally employed debt swaps as a liability management instrument to create fiscal savings, which can be channelled to development objectives, while optimising public debt profiles, reducing refinancing risks and improving fiscal sustainability.

3chap6_p_3The traditional bilateral debt swap approach originated in the late 1980s in Latin America to support nature conservation. These transactions exchanged portions of sovereign debt for commitments to biodiversity conservation and climate resilience. Over time, other sectors have benefited from bilateral debt swaps, including health, education and food security. According to the United Nations Conference on Trade and Development, more than 230 bilateral swaps have been concluded in 58 countries since 1987, with a combined face value of nearly USD 8 billion. The Global Fund has been a major player in bilateral debt-for-health swaps, concluding 14 agreements since 2007 with an average deal size of USD 23.5 million to support national health programmes targeting human immunodeficiency virus (HIV), tuberculosis (TB) and malaria. While these operations have delivered a meaningful impact, their scale remains modest relative to the growing financing needs of health systems across Africa, primarily because they depend on the generosity of a creditor country to cancel their debt.

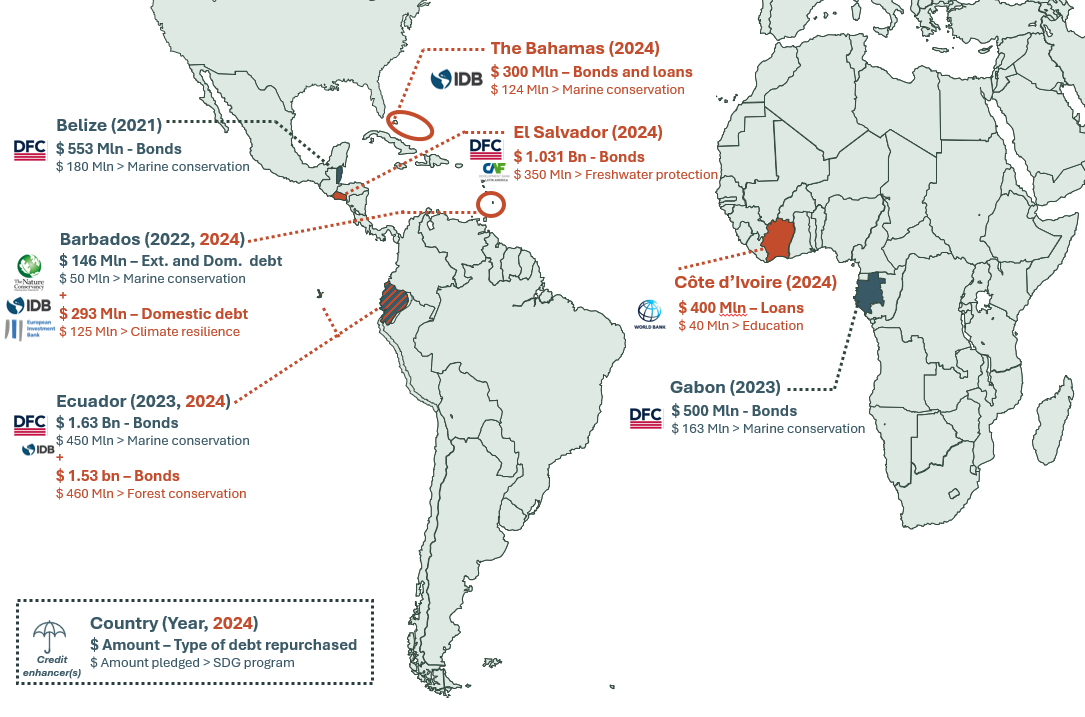

4chap6_p_4Since 2021, a new generation of commercial debt swaps (known as debt conversions) has emerged, significantly increasing the volume of potential transactions. It began with nature conservation in Latin America but is now being applied to a broader range of sectors, including education. This new generation of debt swaps has expanded beyond purely financial objectives to encompass structures that align debt management strategies with national development priorities. These innovative mechanisms, where a country exchanges part of its existing debt for new, guaranteed borrowing under more favourable terms, then reallocates (part of) the associated savings to specific projects, have gained traction across emerging markets as governments seek to leverage debt relief for broader socio-economic and environmental outcomes. In the environmental space, large-scale operations include transactions in Belize (2021), Barbados (2022; 2024) and Gabon (2023). Ecuador’s debt swaps in respect of the Galápagos Islands (2023) and the Amazon (2024), Bahamas (2024) and El Salvador (2024) unlocked over USD 2.1 billion for conservation, with over USD 4.6 billion of debt exchanged.

5chap6_p_5This model has also been extended to education, with Côte d’Ivoire’s (2024) transaction, which mobilised EUR 40 million for education over 5 years.

chap6_img_0

chap6_img_06chap6_p_6This context underscores the urgency of exploring debt conversions to support the health sector, through refinancing existing debt with both bond and non-bond instruments. By leveraging credit enhancement and market-based mechanisms, debt conversions could significantly amplify fiscal savings and channel resources toward health priorities at scale.

Debt Swap Structures: Bilateral versus Commercial

7chap6_p_7Bilateral debt swaps and debt conversions have distinct features. Country-specific objectives and fundamentals should guide the selection of the most suitable instrument. Table 6.1 below summarises the key characteristics of each structure.

|

8chap6_p_8Bilateral Debt Swaps |

9chap6_p_9Debt Conversions |

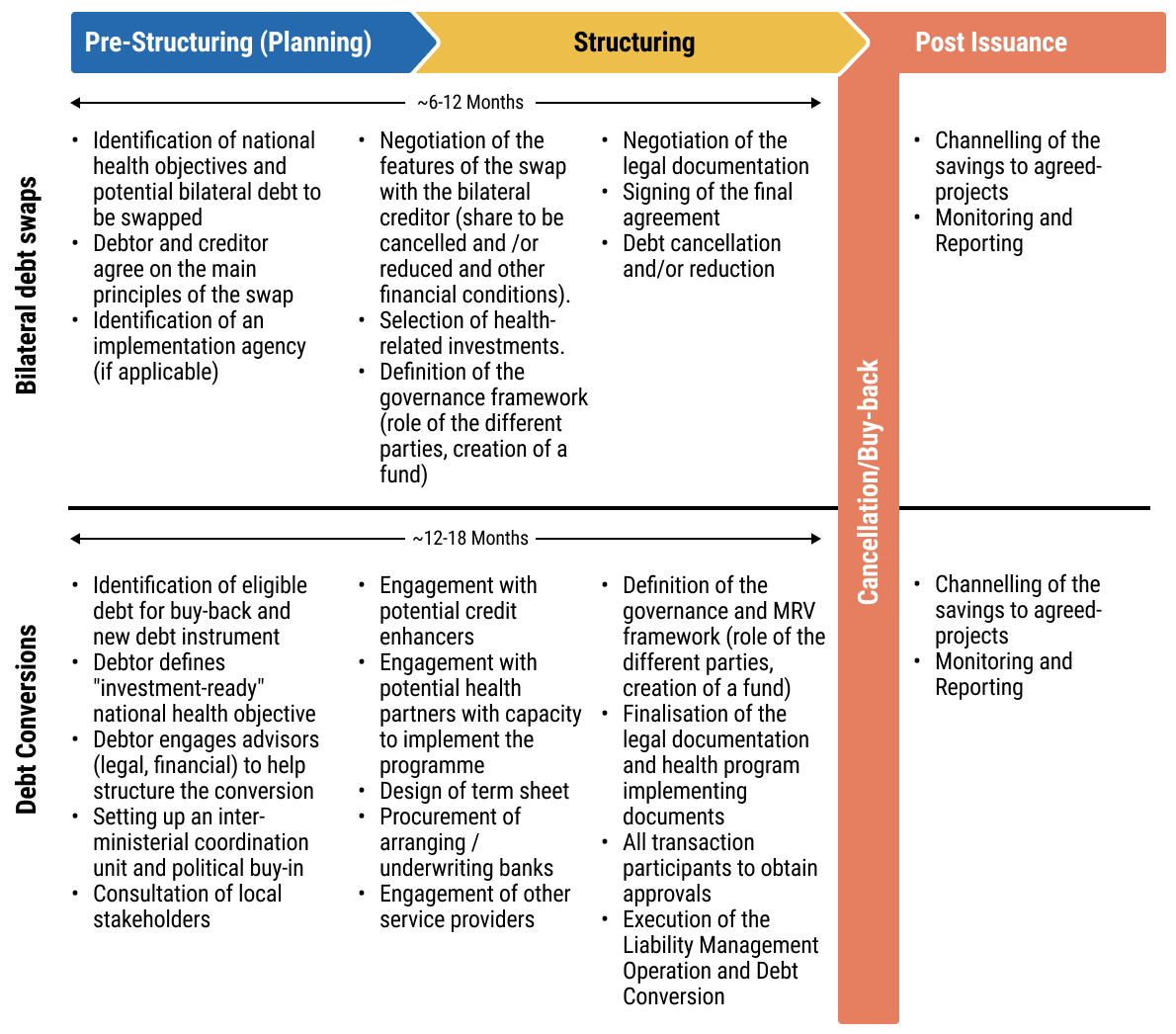

|

|

10chap6_p_10Debt swap mechanisms |

|

|

|

11chap6_p_11Target existing debt facilities |

|

|

|

12chap6_p_12Involved third-parties |

|

|

|

13chap6_p_13Range of debt swapped |

|

|

|

14chap6_p_14Range of programme funding |

|

|

|

15chap6_p_15Typical programme design timeline |

|

|

|

16chap6_p_16Typical financial execution timeline |

|

|

17chap6_p_17Note: The programme design phase includes agreeing on the health-linked application of freed-up fiscal savings, policy and spend commitments, as well as related monitoring and verification. The financial execution phase includes defining the structure, negotiating and executing. Depending on the situation, these two phases can be successive or run in parallel. Ranges are based on historical transactions that have been executed.

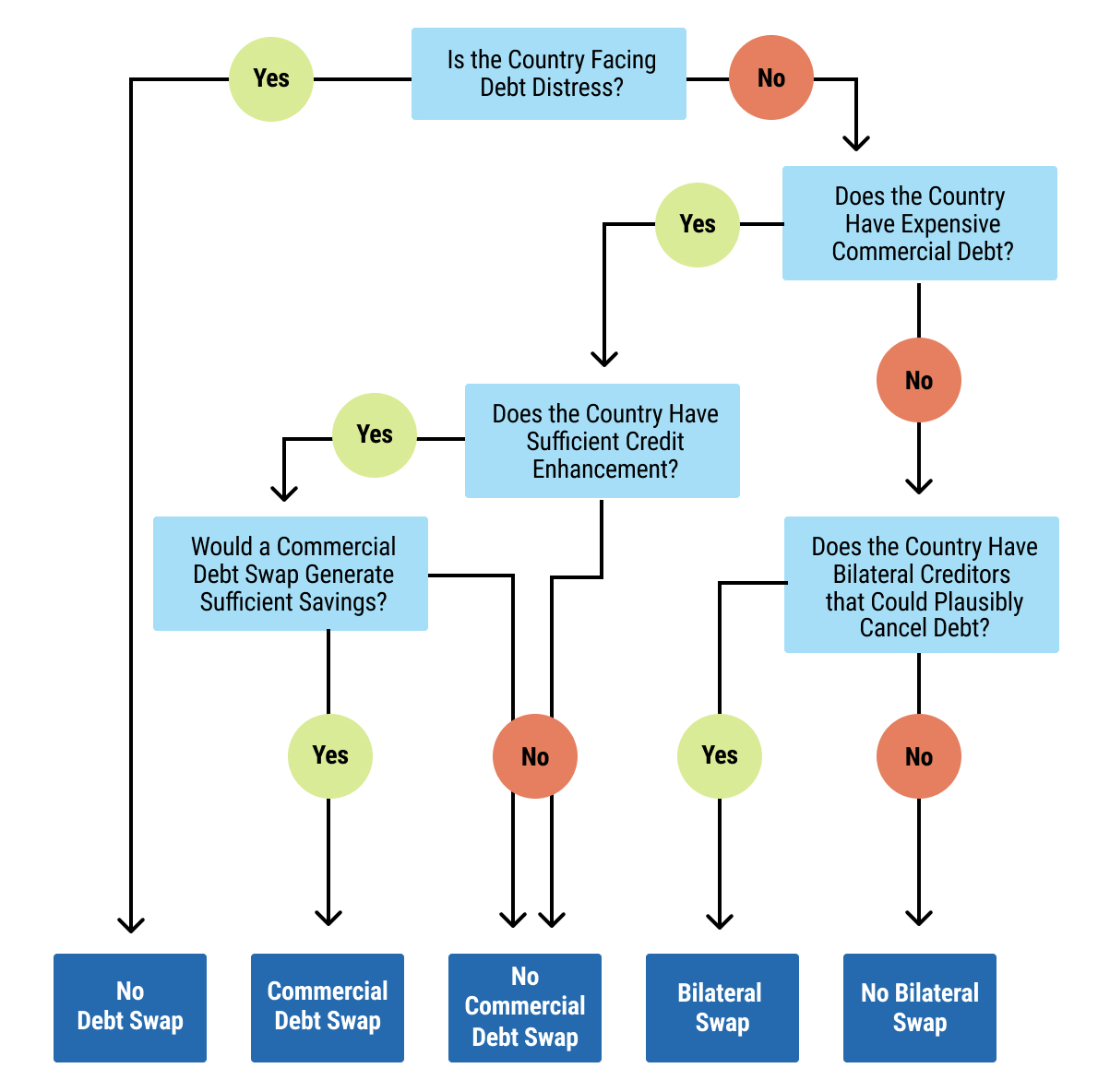

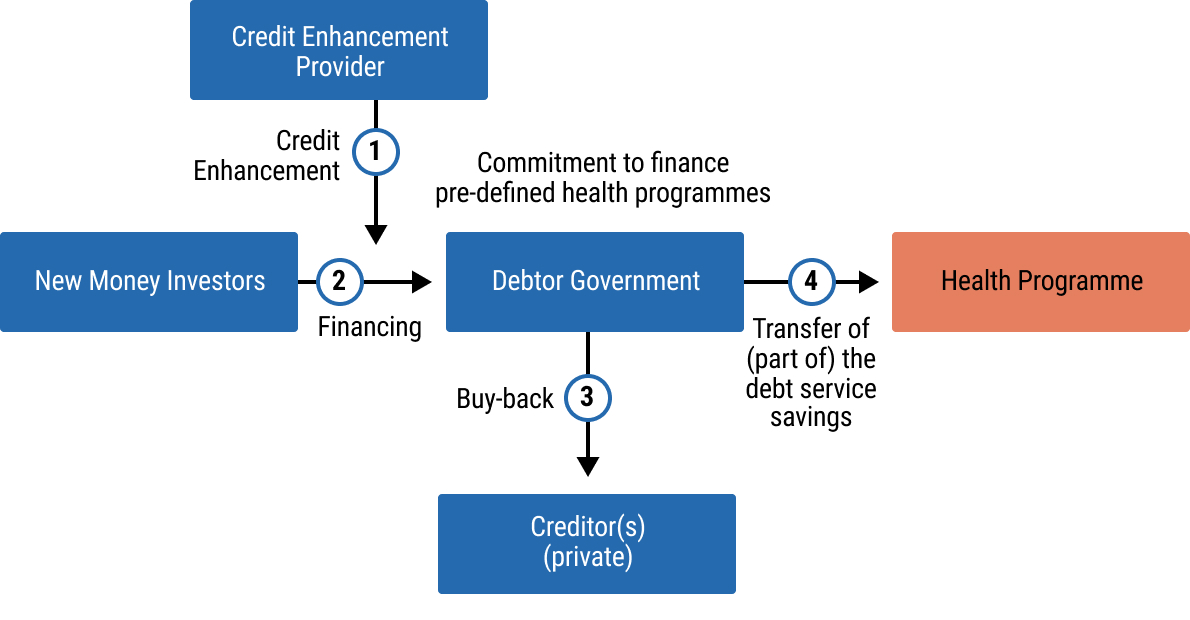

18chap6_p_18Several factors need to be evaluated to assess whether a debt swap provides the right tool in the country’s specific context. For countries facing unsustainable debt burdens, a comprehensive debt restructuring, generating substantial debt relief, is likely required. While debt swaps serve as a liability management tool, they do not address solvency issues and should be viewed as a means of providing liquidity support. The decision tree below helps to navigate the decision-making process.

chap6_img_1

chap6_img_1Debt Swaps to Support Health Programmes

Aligning Financial Flows with Health Programmes

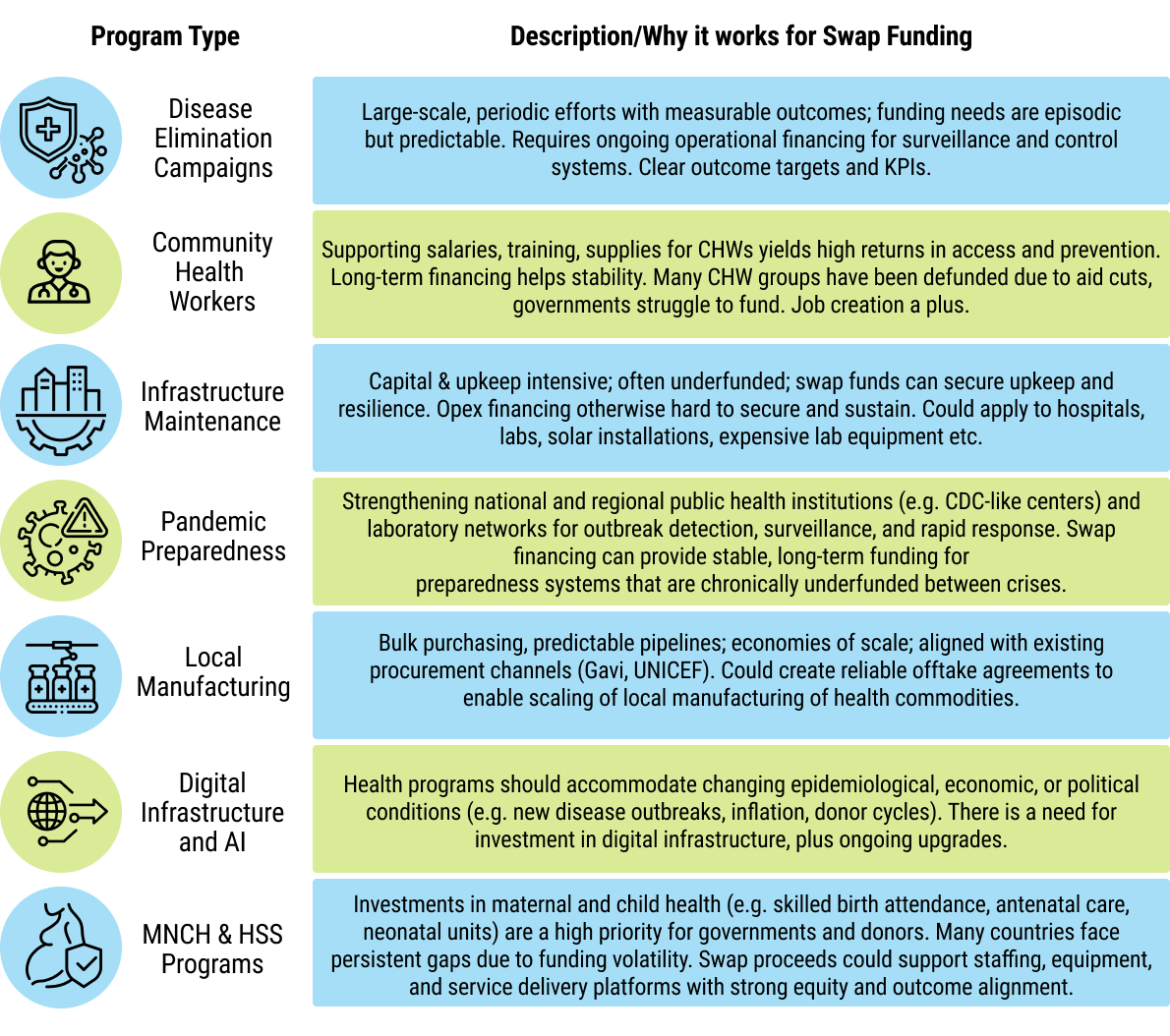

19chap6_p_19The financial flows generated through a debt swap are well-suited to health financing needs, as they tend to be long-term, regular and predictable. Debt swaps are not one-off grants or loans. Instead, they enable countries to redirect their savings towards long-term health objectives. When a country enters a swap arrangement, it agrees to make fixed, periodic payments into a development fund or to a specified third party, instead of paying those amounts to the original creditors. These payments are often set for the life of the swapped debt, which can be up to 20 years, as in the case of Belize, and typically above 10 years - although bilateral debt swaps can have a shorter tenure. Because they are linked to the sovereign’s debt-servicing obligations, the payment flows can become a legally binding, long-term commitment.

20chap6_p_20The unique structure of these financial flows warrants careful consideration to fully harness their potential in advancing health outcomes. Three guiding principles can help orient the nature of spending that a debt-for-health swap could support:

- chap6_ul_15

- chap6_li_26Long-term vision and government ownership. Define a clear long-term vision for what swap resources will achieve, align it with national plans, utilise consultations at both design and operational levels, and establish measurable results and outcome-based commitments to guide spending over many years.

- chap6_li_27Spending that benefits from long-term financing. Direct resources to expenditures with predictable multi-year costs or high long-term returns, for example, maintenance programmes, infectious disease surveillance systems, vaccine financing and campaigns, workforce training, climate-resilient infrastructure and broader human capital.

- chap6_li_28Additionally, with government budgets. Implement governance and selection rules that ensure swap funds do not displace baseline government spending but are instead accretive to it. Practical measures include prioritising programmes that the budget would not reliably fund, and channelling quick-release funds for emerging needs and sustained finance for longer-term programmes.

21chap6_p_21Figure 6.3 below highlights examples of health spending that could be aligned with those principles - depending on the country context.

chap6_img_2

chap6_img_2

Delivering Health Programmes

22chap6_p_22Debt swap-funded programmes have traditionally been delivered by implementing entities that are accountable for the programme implementation. Often, the debt swap enabler (the bilateral creditor in a bilateral debt swap or the development finance institution providing credit enhancement in a debt conversion) requests that such intermediaries provide them with comfort regarding the programme delivery. There can be transaction costs for setting up those intermediaries, and different models have been used thus far, with costs typically going in decreasing order:

- chap6_ul_16

- chap6_li_29Setting up a dedicated trust fund. A legally independent, separate entity, with board members from the government, the implementing partner, and other independent technical experts and professionals, which ensures that the resources freed by the debt swap are applied as agreed and subject to strong governance. For example, Belize’s 2021 blue bond debt swap led to the creation of an independent conservation trust fund - the Belize Fund for a Sustainable Future (BFSF). The BFSF receives long-term payments from the Government of Belize and allocates these flows towards marine and coastal protection. It is essential to determine upfront whether a new trust fund will be used for future operations, not just the specific transaction, as this informs its design and governance, allowing transaction costs to be spread across different operations. For example, the Seychelles utilised the Seychelles Conservation and Climate Adaptation Trust, established for Seychelles’ 2015 debt swap, to receive proceeds from a blue bond transaction.

- chap6_li_30Using existing structures. Leveraging existing structures to facilitate the objectives of the debt swap, either at the national or global level.

- chap6_li_31National structures: Country-specific, national trust funds. For example, the Bahamas 2024 commercial debt swap was implemented through the Bahamas Protected Areas Fund (BPAF). The BPAF was previously established in 2014 by an Act of Parliament to provide “sustainable financing into perpetuity” for the management of the country’s protected‐areas system. The El Salvador debt swap involved a collaboration between the already existing Environmental Investment Fund of El Salvador and Catholic Relief Services.

- chap6_li_32Global structures: Instead of channelling the funds to a separate trust fund, the fiscal savings can be channelled to international organisations or development institutions already present in the country and with mandates that are aligned with the debt swap objectives. For example, the Global Fund, through its debt-for-health model, has been widely used as an implementing channel for bilateral debt-for-health swaps owing to its strong fiduciary systems, large in-country delivery footprint, and ready pipeline of technically vetted programmes that allow countries to rapidly and transparently translate debt swap proceeds into measurable health impact (see the box below: The History of Debt-for-Health Swaps).

- chap6_ul_17

- chap6_ul_18

- chap6_li_33Using country systems. For its 2024 commercial debt swap, Côte d’Ivoire is utilising its existing systems and institutions to deliver the programme. In this case, the savings are channelled into an already existing education-sector programme-for-results supported by the World Bank.

The History of Debt-for-Health Swaps23chap6_p_23Debt-for-health swaps had a brief history with the United Nations Children’s Fund (UNICEF) between 1991 and 1993, during which the institution served as the implementing organisation for seven debt-swap operations, totalling approximately USD 75 million. Older debt swaps that benefited the health sector included approximately 8% of the French add-on programme to Heavily Indebted Poor Country (HIPC) debt relief, known as the Contrat Désendettement Développement, and a debt buyback of Nigerian debt by the River Blindness Foundation to combat river blindness in 1993. 24chap6_p_24It was only after the Global Fund launched its debt-for-health programme in 2007 that debt swap resources started supporting the health sector at scale. Leveraging its role as the most prominent global health financier and its extensive operational footprint across more than 120 countries, the Global Fund introduced Debt2Health (D2H), a structured, high-integrity model that transformed debt swaps from ad hoc instruments into a reliable and scalable financing tool for health. Unlike earlier swaps, D2H embedded rigorous fiduciary oversight, transparent reporting and measurable programmatic commitments - giving creditors the assurance they needed and enabling countries to channel resources immediately into technically vetted, high-impact health interventions. 25chap6_p_25Three features of the Global Fund’s model proved catalytic. First, its existing grant architecture and trusted assurance systems (including independent audits, procurement controls and in-country grant management structures) dramatically reduced transaction costs and implementation risks. Second, its Register of Unfunded Quality Demand (UQD) (See: https://resources.theglobalfund.org/en/grant-life-cycle/grant-making/unfunded-quality-demand/) provided a ready pipeline of technically reviewed, country-owned programmes, allowing debt-swap proceeds to be rapidly absorbed without lengthy design phases. Third, the Global Fund’s established relationships with MoFs and MoHs created the political and operational alignment needed to turn cancelled debt into sustained domestic investments. 26chap6_p_26As a result, D2H became the first mechanism to deliver debt-for-health swaps at a meaningful scale, demonstrating that well-structured swaps could reliably produce additional, predictable funding for national HIV, TB, malaria and health-systems priorities - while maintaining full country ownership and alignment with national strategic plans. Between 2007 and 2025, the Global Fund closed 14 transactions involving three creditor countries (Australia, Germany and Spain), converting nearly USD 500 million of bilateral debt into USD 330 million in health funding for 11 debtor countries. Germany, in particular, contributed to more than 84% of the health investments generated by the D2H programme. |

Bilateral Debt-for-Health Swaps

Description and Rationale

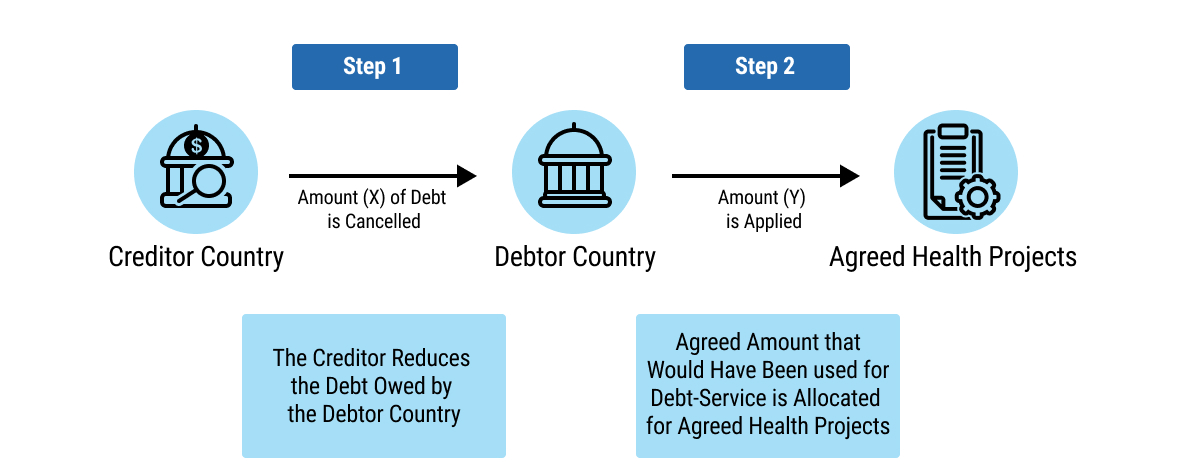

27chap6_p_27Bilateral debt-for-health swaps are voluntary operations whereby a bilateral creditor agrees to cancel or reduce existing debt in exchange for a predetermined health spending commitment by the debtor country. The debtor country will reallocate all or part of the debt service on the cancelled or reduced debt to support a pre-approved health programme over time. In other words, instead of repaying the debt to the creditor, the debtor country spends it on an in-country programme. The health programme may be implemented by a reputable international organisation and/or by the government or public institutions.

chap6_img_3

chap6_img_3

28chap6_p_28The incentives for the parties on a bilateral debt swap typically include the following:

- chap6_ul_19

- chap6_li_34For the debtor country, the transaction unlocks additional health financing while advancing national development goals.

- chap6_li_35For the creditor country, the swap provides a vehicle to reinforce its commitment to global health diplomacy, potentially increasing Official Development Assistance (ODA) under specific conditions.

- chap6_li_36For the health intermediary, it enables them to expand their operations and demonstrate a greater impact in the country.

Case Study: A Large-Scale Debt-for-Health Swap Accelerating Tuberculosis Elimination29chap6_p_29In 2022, as part of the 7th Replenishment, Germany announced a significant new commitment to the Global Fund, explicitly reaffirming that EUR 100 million of this commitment would be delivered through debt-for-health (D2H) mechanisms. Building on more than a decade of successful D2H cooperation, Germany and Indonesia initiated discussions to convert a portion of Indonesia’s bilateral debt into predictable financing for national health priorities - primarily tuberculosis (TB), a disease for which Indonesia carries the world’s second-highest burden. 30chap6_p_30The pathway from political commitment to implementation followed a structured, multi-step process:

31chap6_p_31This operation demonstrates how a clear political commitment by a creditor (Germany), strong country ownership (Indonesia) and a trusted delivery platform (the Global Fund) can turn public debt into measurable health impact at scale. It also illustrates the strengths that make the Global Fund a partner of choice for debt-for-health swaps. Through its long-standing relationships with MoFs and MoHs, the Global Fund has consistently helped align priorities between debtor and creditor countries, grounding each transaction in nationally endorsed strategies and measurable outcomes. Its established governance, fiduciary and assurance systems provide the accountability that creditors require, while dramatically reducing implementation risk and transaction costs. The Global Fund’s UQD pipeline provides a ready pool of vetted interventions, addressing capacity constraints, accelerating programme design and ensuring additionality. Moreover, by integrating swap proceeds into existing grants and national planning cycles, debt-for-health avoids parallel structures and reinforces existing systems for implementing, auditing, measuring and reporting impact. These strengths have enabled the Global Fund to deliver a series of timely, mutually beneficial debt swaps over nearly two decades, helping turn complex political and operational challenges into a durable health impact. |

Enabling Conditions

- chap6_ol_1

- chap6_li_41Identifying plausible debt for a bilateral swap

32chap6_p_32A first step is to identify the list of potential bilateral creditors. The exercise can involve compiling a list of bilateral creditor countries, including the respective size of their claims and the remaining duration, as well as whether the debt was provided based on concessional official development assistance (ODA) loans. In addition to the country’s internal debt management database, this information can also be found in public databases such as the World Bank International Debt Statistics. It would be essential to focus on the size and terms of the debt, prioritising creditors with outstanding amounts in line with the country’s health programme’s financing needs and potentially the more expensive bilateral debt.

33chap6_p_33The second step is to identify, among the existing creditor countries, those who would most likely support a debt swap. That identification exercise depends on a spectrum of indicators, including:

- chap6_ul_20

- chap6_li_42Creditor countries that have a strong bilateral relationship with the debtor country. In close collaboration with the Foreign Ministry, the debtor country can identify key creditors most likely to provide financial support, particularly for its health system.

- chap6_li_43Creditor countries that have a track record of supporting debt swaps, especially in health. Historically, Germany and Spain are the two countries that have supported the most debt-for-health swaps.

- chap6_li_44Creditor countries that have recently announced debt swap programmes.

- chap6_li_45Spain announced at the Fourth International Conference on Financing for Development in July 2025 that it would step up its debt-for-development swap efforts.

- chap6_li_46In June 2025, Italy announced a EUR 235 million debt swap programme to support local development projects over 10 years.

- chap6_li_47In July 2025, China and Egypt signed a framework agreement for the first phase of a debt swap programme through China International Development Cooperation Agency loans, marking the first such initiative by China, which may pave the way for additional debt swaps.

- chap6_ul_21

- chap6_ol_2

- chap6_li_48Political and institutional arrangements in the debtor country

34chap6_p_34Countries considering a debt-for-health-swap can leverage lessons learned from previous cases to identify the leading enablers for global implementation:

- chap6_ul_22

- chap6_li_49Strong political leadership and buy-in signal that the instrument is accepted at the political level, and therefore, that the government will be willing to invest political capital in championing the full implementation of the swap and ensuring accountability.

- chap6_li_50A clear institutional structure that defines the lead ministry, supported by other relevant ministries, departments and agencies (MDAs). The lead ministry is typically the MoF, supported by the MoH, which leads the implementation of the agreement once finalised.

- chap6_li_51Alignment with national development goals is crucial to ensure that the swap proceeds complement the government’s plans and priorities and do not establish a separate and potentially fragmented set of priorities.

- chap6_li_52Building country ownership from the start is essential to ensure transparency, accountability and the use of country systems to deliver on the debt swap, aligning with the principles of aid effectiveness and the Lusaka agenda.

- chap6_li_53The formation of an oversight and coordinating mechanism ensures that all relevant stakeholders have an opportunity to weigh in and are part of the decision-making process.

- chap6_ol_3

- chap6_li_54Early political buy-in

35chap6_p_35A debt-for-health swap involves multiple actors with distinct roles, so securing early political buy-in from a small group of high-level stakeholders is essential. These individuals will vary by country, but their endorsement signals government commitment and alignment around the process. Early engagement should be interactive and tailored, framing the debt swap in terms of each stakeholder’s priorities, pain points and incentives. To do this effectively, their internal concerns must be well understood in advance, anticipated and directly addressed in the briefing materials prepared for these discussions.

36chap6_p_36For further details on the different stakeholders involved, please see the Implementation section which follows.

Opportunities and Challenges

Opportunities

37chap6_p_37Bilateral debt swaps can mobilise additional funding for health services that align with national health strategies. This should be the starting point for a debt-for-health swap, and the government should play a key role in identifying potential uses of the proceeds. The MoH can identify health programmes that are more likely to be additional and that will not come at the expense of budget allocations from the MoF.

38chap6_p_38A bilateral debt swap can also come with additional financial benefits.

- chap6_ul_23

- chap6_li_55A bilateral debt swap might free up additional fiscal space through debt relief, which was the case in 8 of the 14 swaps implemented by the Global Fund.

- chap6_li_56Additionally, debt swaps should lower demand on foreign reserves because they typically allow the debtor country to make the repurposed payments in local currency.

- chap6_li_57Lastly, rating agencies should view bilateral debt swaps as positive even if they have typically represented only a marginal portion of the debtor country’s total debt. Given the involvement of official bilateral partners and the smaller size of the debt swaps, credit rating considerations carry less weight for bilateral debt swaps compared to debt conversions.

39chap6_p_39Working through a global health institution, such as the Global Fund, has significant upsides. The institution ensures that funding flows to pre-defined funding gaps that the government vets for their quality. In addition, its platform sets standards for transparency, inclusion, country ownership, accountability and measurable outcomes based on indicators that are independent, transparent and accurate and that involve civil society. While debt swap negotiations timelines can be protracted, the institution should have the advantage of having a pipeline of health programmes awaiting funding, for example, through its Register of UQD in the case of the Global Fund. Lastly, funds generated by debt swaps can serve as the country’s co-financing payment. This helps explain why all the identified debt-for-health swaps since 2007 have been channelled through the Global Fund.

Challenges

40chap6_p_40The primary challenge of a bilateral debt swap is aligning the incentives between the creditor and debtor countries. This involves identifying the appropriate health activity supported by the swap, as well as the implementing agency that will provide comfort to both countries. Moreover, convincing the creditor country to cancel or reduce its debt claims demands substantial negotiation.

41chap6_p_41Identifying an organisation that will be the custodian of the fiscal savings released by the debt swap and help to implement the debt swap is a key parameter in the negotiation. This organisation needs to have credibility for the implementation, monitoring and evaluation of health programmes in the country. As mentioned above, a new entity could be established, or an existing organisation identified.

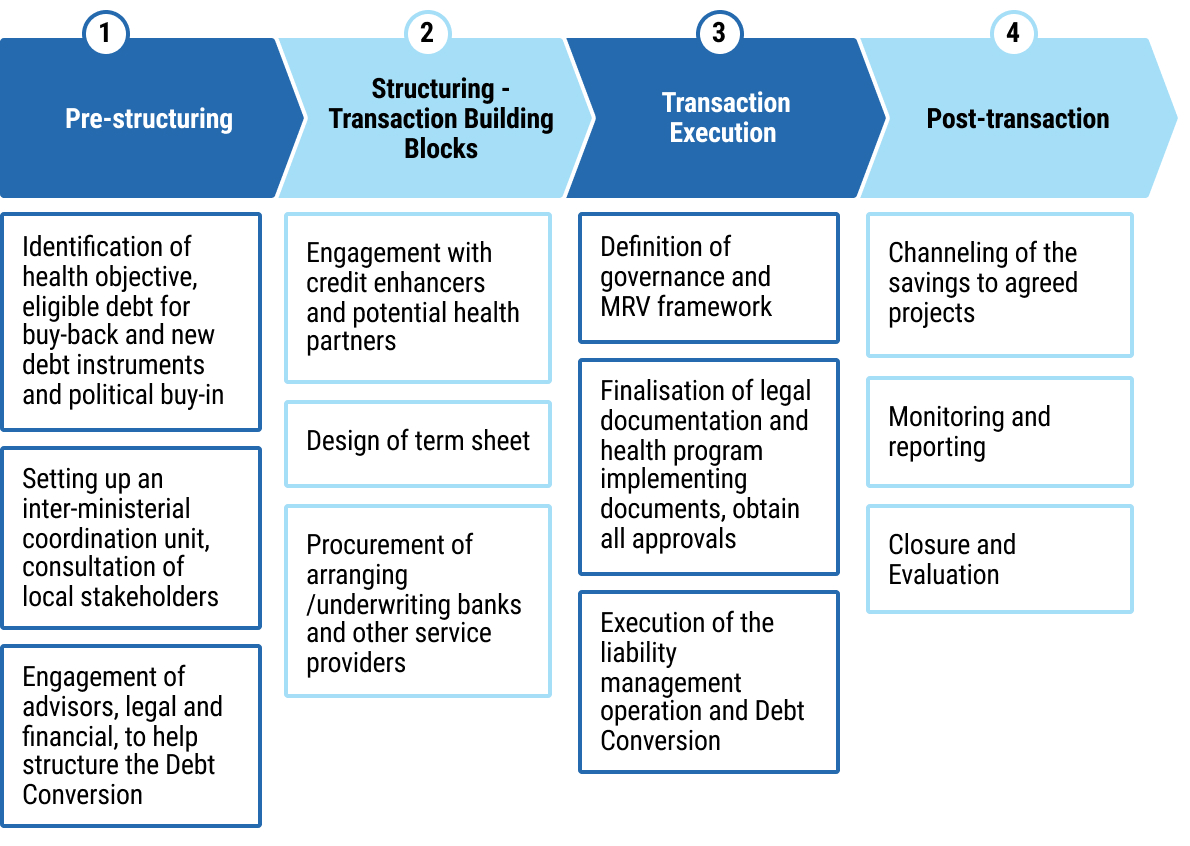

Implementation

Life Cycle of a Bilateral Debt Swap

chap6_img_4

chap6_img_4- chap6_ol_4

- chap6_li_58Identification and political agreement. Both creditor and debtor governments agree in principle on converting part, or all, of the outstanding debt into health-related funding. They assess feasibility, alignment with health and development objectives and mutual interest.

- chap6_li_59Negotiation and legal framework. A formal agreement defines the debt amount and associated treatment, including the share to be cancelled or reduced, the application of the savings generated towards an agreed domestic investment, the implementing agency and the governance structure.

- chap6_li_60Debt cancellation. The creditor cancels all, or a portion, of the agreed debt, while the debtor commits the pre-agreed payments to a national or dedicated fund, if needed, for the agreed-upon projects or programmes.

- chap6_li_61Project selection and implementation. Funds are allocated to vetted programmes aligned with national priorities and implemented through established systems or a dedicated fund.

- chap6_li_62Monitoring and reporting. Performance is tracked and reported transparently to all parties, ensuring accountability and measurable impact.

- chap6_li_63Closure and evaluation. Upon completion, results are evaluated, lessons are documented and the agreement is formally closed.

Stakeholder Engagement

42chap6_p_42Once the decision to swap debt for health has been made, the lead ministry identifies all critical stakeholders from relevant MDAs and incorporates them into the process. Involved stakeholders should be adapted to each country’s institutional and political context.

43chap6_p_43In many cases, the initiators of bilateral debt swaps are the MoF or the creditor nation. The role of the MoH in these situations is to be responsive to requests for information on priority interventions and their costs, and ensure follow-up with the MoF, leading the transaction.

44chap6_p_44That said, the MoH could be the originator of the idea of the debt-for-health swaps. In this instance, the MoH carries greater responsibility for early-stage preparation, including ensuring that the proposal is technically sound, supported by credible data, and clearly articulates the rationale for why such a mechanism is needed and how funds would be effectively utilised. If the MoF has previously raised concerns, for example, about absorptive capacity or financial management, these should be proactively addressed in an initial briefing note or concept note shared with the MoF and other high-level stakeholders. Clear, evidence-based communication at this stage builds confidence. It facilitates cross-ministerial alignment once the MoF aligns with the plan and becomes the lead for the debt swap. The MoH’s role then shifts to follow up and continued engagement in proposal writing, creditor engagements and implementation plans.

|

45chap6_p_45Stakeholder / Institution |

46chap6_p_46Core Role in Debt Swap Process |

47chap6_p_47Interest / Incentive |

48chap6_p_48Potential Concern / Risk |

49chap6_p_49Engagement Strategy / Framing |

50chap6_p_50Phase of Involvement |

|

51chap6_p_51Minister of Health 52chap6_p_52 53chap6_p_53Deputy Ministers of Health/Ministers of State for Health |

54chap6_p_54Sector policy leader; defines investment priorities and measurable outcomes for the fiscal savings generated by the debt swap; Could be the originator of the swap idea |

55chap6_p_55Stable, predictable funding for planned healthcare interventions and programmes; alignment with Sustainable Development Goal (SDG) and Universal Health Coverage (UHC) goals |

56chap6_p_56Concern that resources may not materialise or that MoF may redirect the fiscal savings generated by the debt swap elsewhere |

57chap6_p_57Frame as debt and fiscal innovation and point to alignment with national documents (national development strategy/plan, debt management strategy) |

58chap6_p_58From the early concept to the end |

|

59chap6_p_59Minister of Finance 60chap6_p_60 61chap6_p_61Debt Management Official (DMO); the Financial Secretary (Permanent Secretary for the MoF) |

62chap6_p_62Custodian of debt; face of external transactions; engages with the creditor |

63chap6_p_63Fiscal space creation; Debt sustainability; demonstration of fiscal innovation and credibility with partners |

64chap6_p_64Concern about losing control of the debt policy; concern about transaction complexity; scepticism about sector-driven proposals; concerns about absorptive capacity |

65chap6_p_65Frame as co-created fiscal innovation for health; point to alignment with health financing strategy; identify unfunded health programmes |

66chap6_p_66From the early concept to the end |

|

67chap6_p_67Creditor Country / Institution |

68chap6_p_68Counterparty to the swap |

69chap6_p_69Diplomatic and ESG visibility |

70chap6_p_70Fiduciary or reputational risk |

71chap6_p_71Emphasise transparency, accountability and co-benefits |

72chap6_p_72From the initial engagement until the end |

|

73chap6_p_73Health Development Partners |

74chap6_p_74Technical and policy support |

75chap6_p_75Programme success, portfolio impact |

76chap6_p_76Fragmentation or overlap |

77chap6_p_77Promote joint planning and unified messaging |

78chap6_p_78Feasibility → Agreement |

|

79chap6_p_79Other relevant stakeholders |

|||||

|

80chap6_p_80Presidency 81chap6_p_81Actors here could include the Chief Minister, Minister of State, etc. |

82chap6_p_82Provides political leadership, cross-ministerial alignment and strategic direction |

83chap6_p_83Mobilising funding for strategic priorities; country being seen as a leader in reforms/innovations and credibility in the comity of nations; political legacy; national ownership |

84chap6_p_84Concern about timing of reform; competing political interests |

85chap6_p_85Frame the high visibility reform potential; links to the national development agenda and regional goals |

86chap6_p_86From the beginning and at inflexion points in the process |

|

87chap6_p_87Parliament 88chap6_p_88Actors here could include the chairs for the parliamentary committee on health, finance, etc. |

89chap6_p_89Approves debt operations and ensures accountability for public expenditure |

90chap6_p_90Transparency; fiscal prudence; public accountability; positive political capital from supporting innovative solutions |

91chap6_p_91Concern about their oversight function being overruled |

92chap6_p_92Engage early with non-technical and practical briefings; demonstrate discipline and tangible citizen benefit; identify cross-party champions |

93chap6_p_93From the beginning and at inflexion points in the process |

94chap6_p_94

96chap6_p_96

97chap6_p_97

129chap6_p_129

|

95chap6_p_95Other relevant stakeholders |

|||||

|

98chap6_p_98Attorney General / Ministry of Justice |

99chap6_p_99Legal review, compliance, approvals and provision of legal opinions |

100chap6_p_100Safeguarding sovereign integrity, ensuring due process |

101chap6_p_101Concern over liability or precedent |

102chap6_p_102Engage early; emphasise role as guardian of national interest |

103chap6_p_103From the negotiation until the agreement is signed |

|

104chap6_p_104Ministry of Foreign Affairs |

105chap6_p_105Manage the diplomatic relationship with the creditor nation; ensure alignment with foreign policy objectives; facilitate communication through official diplomatic channels |

106chap6_p_106Maintain and strengthen the integrity of the diplomatic relationship and international credibility; advance the country’s image as a reform-oriented and responsible partner |

107chap6_p_107Concern about frayed relationships if swaps don’t work out; risk of being bypassed in technical discussions |

108chap6_p_108Engage early; emphasise their role as custodians of the diplomatic relationship |

109chap6_p_109From early on in the process until the implementation |

|

110chap6_p_110Central Bank |

111chap6_p_111Foreign exchange and payment management |

112chap6_p_112Accuracy, compliance, reporting integrity |

113chap6_p_113Transaction complexity |

114chap6_p_114Involved as a technical assurance partner |

115chap6_p_115Negotiation until the implementation |

|

116chap6_p_116Health regulatory agencies |

117chap6_p_117Provide technical oversight, quality assurance and regulatory approvals for interventions funded through the swap, such as procurement of medicines, construction of health facilities or deployment of digital health tools |

118chap6_p_118Ensuring that swap-funded programmes meet national quality, safety and ethical standards; an opportunity to strengthen institutional visibility and capacity through well-managed projects 119chap6_p_119 |

120chap6_p_120Insufficient consultation leading to delays in approvals or non-compliance with national standards; risk of being perceived as bypassed in implementation oversight |

121chap6_p_121Co-opt regulators early based on the nature of funded interventions; frame participation as safeguarding quality and ensuring accountability of public investments; use them as technical verifiers or members of project review committees |

122chap6_p_122Feasibility → Implementation → Monitoring |

|

123chap6_p_123Civil Society / Academia / Media |

124chap6_p_124Oversight, communication, public trust |

125chap6_p_125Accountability, participation |

126chap6_p_126Limited access to information |

127chap6_p_127Share regular updates and accessible data |

128chap6_p_128Implementation → Monitoring |

Reporting

130chap6_p_130Transparency regarding monitoring, reporting and accountability is an essential element in the implementation of a debt-for-health swap, both for debtor and creditor countries. The reporting costs can vary significantly depending on the level of information required and when it is needed. Organisations that already have existing systems set up are likely to provide more credible reporting at a lower cost.

Debt Conversions

Description and Rationale

131chap6_p_131Commercial debt swaps are referred to as debt conversions. They are a type of liability management operation that allows a sovereign nation to replace its existing private-sector debt (such as bonds or loans) with new instruments under more favourable terms. The central purpose of this refinancing is to generate fiscal savings, which are then contractually allocated to fund specific national priorities, specifically healthcare.

132chap6_p_132Unlike bilateral swaps, which restructure government-to-government loans, debt conversions are implemented through the capital markets or banking sector, where the sovereign refinances debt held by private sector investors or lenders using proceeds from new debt (“New Debt”) to finance the buyback of the old debt. These transactions are structured around three key features:

- chap6_ol_5

- chap6_li_64Credit enhancement. The New Debt is typically credit-enhanced through guarantees or insurance from MDBs, development finance institutions (DFIs) or private sector parties (e.g. insurers or guarantors). This enhancement reduces the risk for new investors, enabling the government to secure lower all-inclusive borrowing costs (e.g. reduced interest rates) and more favourable repayment terms (e.g. longer repayment periods), resulting in financial savings (see Chapter 8: Credit Enhancement.)

- chap6_li_65Performance-linked objectives. To ensure alignment of the new financing to desirable health objectives, the New Debt is tied to legally binding policy commitments or key performance indicators (KPIs).

- chap6_li_66Governance system. A robust and accountable mechanism is utilised to manage and deploy the savings generated by the operation into the designated development objective. These can be channelled through a dedicated trust fund, through existing multilateral organisations’ programmes or through domestic government systems with equivalent oversight.

133chap6_p_133Ultimately, debt conversions can be a powerful tool for governments to create significant funding for national priorities without increasing their overall debt burdens - and often by reducing them (if the debt being repurchased, for example, trades at a considerable discount). They work by reducing fiscal expenditure on debt servicing and reallocating a portion of those savings toward financing gaps that require consistent, predictable and long-term investment. This approach can also provide a stable, long-term financing source for sovereigns that typically face costly or limited access to capital markets, offering them access to a new investor base due to their creditworthiness and pro-development features.

chap6_img_5

chap6_img_5

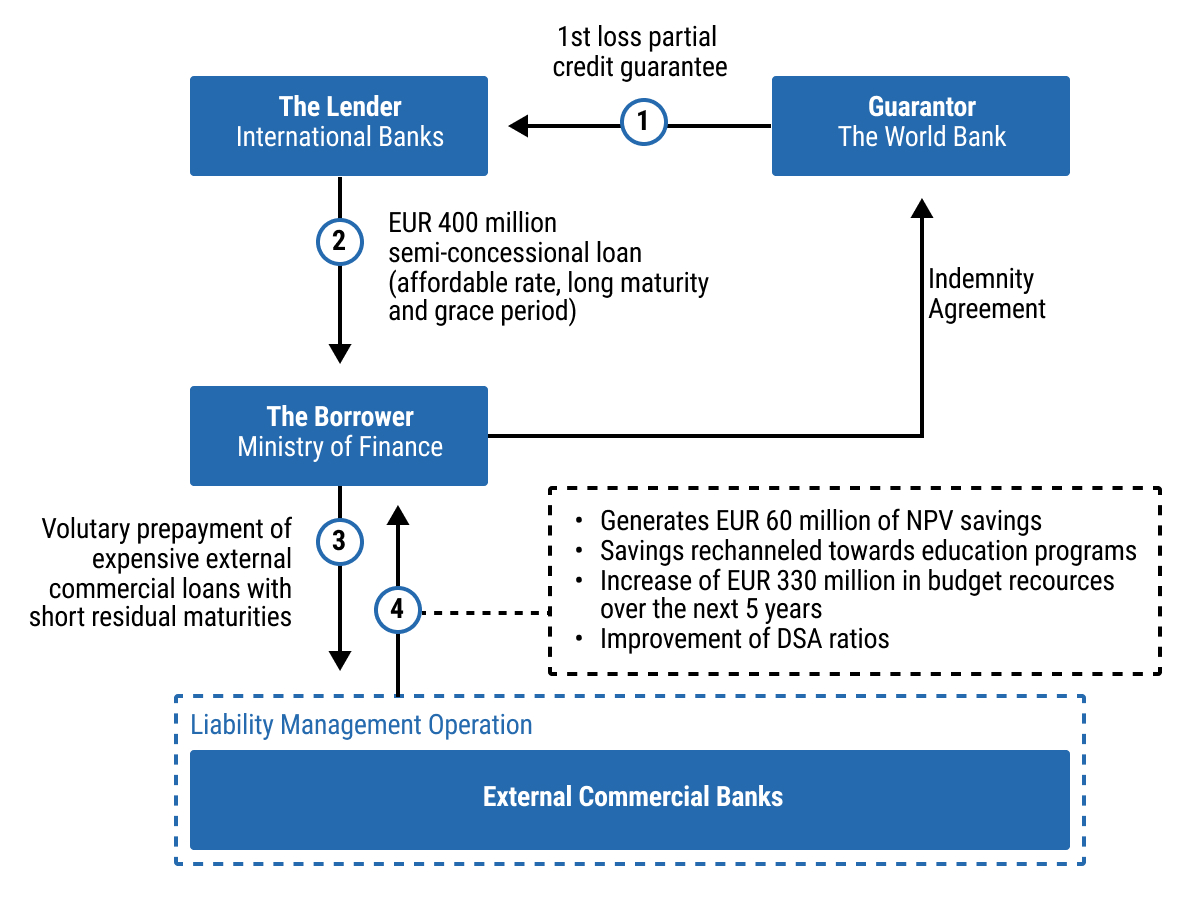

Case Study: Republic of Côte d’Ivoire, Debt-for-Development swap supported by the World Bank (2024)134chap6_p_134The transaction is the first “Debt for Development” swap supported by the World Bank following the publication of its reference framework in July 2024. It aimed to improve Côte d’Ivoire’s public debt profile and generate fiscal space for the education sector. 135chap6_p_135By refinancing expensive external commercial loans via a loan partially guaranteed by the World Bank, the transaction freed up around EUR 330 million in budget resources over the next five years, generating lifetime savings of at least EUR 60 million in net present value terms. Part of the savings will be repurposed towards an ongoing education programme supported by a World Bank Programme for Results financing instrument, which monitors the newly agreed-upon results and outcomes in the education sector, leveraging country systems already in place. The development objective of the Programme de Renforcement du Système Éducatif de Base is to improve: (i) equitable access to education and school health services at pre-school and primary level; (ii) improve learning outcomes; and (iii) strengthen performance-based management along the education service delivery chain.  chap6_img_6 chap6_img_6 |

Enabling Conditions

136chap6_p_136Before embarking on a debt conversion, it is essential to evaluate the following criteria to assess the applicability of this financing mechanism.

- chap6_ol_6

- chap6_li_67Debt eligibility and availability. Debt conversions provide the most significant savings when the cost of existing debt is high. Hence, countries should prioritise existing debt facilities that carry high interest rates and/or shorter-term maturities. Significant savings and debt-to-GDP reductions can also be achieved if the country purchases bonds trading at substantial discounts.

- chap6_ol_7

- chap6_li_68Availability of credit enhancement. A highly-rated third party, typically an MDB or DFI, must be willing to provide a guarantee or political risk insurance (PRI) for the New Debt. Such credit support is also provided by private sector entities (e.g. insurers, impact guarantors, family offices). Such schemes will lower the interest rate on the new loan, making the debt conversion viable.

- chap6_ol_8

- chap6_li_69A clear and credible purpose. The country must have a well-defined, measurable and investment-ready national priority that is typically part of its national development strategy (e.g. funding a public health programme). This priority should feature clear SDG-related benefits for the country, which would form the basis for the commitments and targets embedded in the operation.

- chap6_ol_9

- chap6_li_70A robust governance system, characterised by transparency and accountability, is essential to manage funds effectively, meeting the requirements of investors and stakeholders. In the case of a trust fund, governance typically includes a board comprising representatives from government, private sector and civil society, supported by clear reporting requirements on fund allocation and impact.

- chap6_ol_10

- chap6_li_71Stakeholder alignment. There must be broad buy-in from local communities, civil society and relevant non-governmental organisations (NGOs). These groups are often responsible for implementing the on-the-ground projects and add crucial credibility and accountability.

- chap6_ol_11

- chap6_li_72Government’s institutional and technical capacity. To execute a debt conversion efficiently and ensure its long-term success, governments need strong political backing and adequate technical capacity. After closing, they must provide regular data and progress reports to meet performance-linked obligations.

Opportunities and Challenges

Opportunities

137chap6_p_137Managing public debt. Commercial debt-for-health swaps enable countries to utilise financial market solutions to reduce their debt stock and/or servicing costs, thereby freeing resources for health sector investment. These debt conversions are most suitable for countries with commercial debt valued below its original value and/or with expensive repayment terms, as well as those with strong financial and health partners willing to support the transaction. While not appropriate for situations of imminent default or unsustainable debt, these swaps can play a significant role in easing fiscal pressures and addressing budget constraints.

138chap6_p_138Advancing health priorities. Debt conversions can secure substantial, long-term funding for health programmes through legally binding frameworks that include monitoring and reporting requirements. This dedicated financing supports measurable health outcomes, strengthens government policy implementation and enables longer-term planning - particularly critical amid declining external funding for health. These transactions also foster improvements in data systems and reporting practices, while promoting inter-ministerial collaboration - a valuable institutional outcome in itself.

139chap6_p_139International market signalling. Such transactions signal a high level of sophistication in a country’s debt management strategy, enhancing investor confidence and broadening the investor base. They often attract attention in financial markets and media, generating positive visibility and reinforcing the country’s reputation for innovative financing.

Challenges

140chap6_p_140Process management. Executing a debt conversion requires inter-ministerial cooperation and clear ownership of the execution process by a designated ministry. A dedicated team of officials should manage the transaction, as these operations are resource-intensive and involve technical aspects that span multiple areas of responsibility. Technical assistance may be considered where capacity gaps exist. To ensure alignment, an initial workshop with all involved officials, supported by case studies and best practices, can be highly effective.

141chap6_p_141Additionally, peer-to-peer exchanges with countries that have completed similar transactions are recommended. Given the complexity and the number of parties involved, robust project management is essential. A lead entity - either within government or an external financial advisor or arranging bank - should be appointed to oversee execution, supported by detailed timelines, document checklists and step plans. Early priorities should include modelling transaction economics, including all-in costs and expenses, assessing liability management strategies for any buyback operations and projecting debt service implications to ensure all stakeholders are aligned on the financial impact.

142chap6_p_142Transaction economics. Securing credit support is a critical early step in structuring a debt swap. Indeed, credit enhancement tools - such as partial credit guarantees, insurance, collateralised schemes - will further improve the financial terms of the new instrument to be issued under the debt conversion (for further details see Chapter 8: Credit Enhancement). Early engagement increases the range of available credit enhancement solutions and helps manage complexity - particularly when multiple providers are involved, as seen in recent debt-for-nature swaps that combined political risk insurance with additional liquidity support. In such cases, intercreditor arrangements and the approach of the different credit enhancement providers to the health-related commitments should be clarified upfront, ideally through an early-stage term sheet.

143chap6_p_143Capital market volatility. For debt conversions involving the buyback of bonds listed on public markets, the bond yields or prices of those existing bonds can fluctuate significantly due to country-specific factors and global geopolitical events, potentially altering the deal economics. To mitigate this risk, confidentiality must be maintained, and external developments - such as International Monetary Fund (IMF) programme announcements, budget presentations, election cycles or ratings actions - should be factored into the timeline. Continuous monitoring of market conditions and readiness to launch when an opportune window arises are essential. This requires being fully documentation-ready and leveraging regular market updates from financial advisors, as well as arranging with banks.

144chap6_p_144Legal implications. Unlike health bonds, loans and sustainability-linked loans/sustainability-linked bonds (SLLs/SLBs), breach of health-related commitments or KPIs could lead to events of default. It is therefore essential for governments to understand the implications of such defaults, including acceleration rights (I.e. lender’s ability to declare the entire loan outstanding amount immediately due and payable following an event of default) and any consent or veto provisions required by credit enhancement providers, given the potential for cross-default provisions across other external debt obligations.

145chap6_p_145It will also be important for governments to understand the implications of any security granted as collateral and the conditions that can trigger enforcement of such security, especially if these could lead to security being enforced over funds generated by the debt swap-related savings (e.g. in relation to any endowments required to be established by credit enhancement providers such as the Development Finance Corporation (DFC)).

146chap6_p_146Data availability and monitoring system. Debt-for-health swaps require strong data systems to enable regular and transparent monitoring of progress. Depending on the design of the debt swap, this could include regular monitoring of health budget execution, tracking of programmatic indicators (such as the number of workers trained and drugs procured) or reporting of outcomes and impact (such as HIV treatment coverage or HIV incidence). The availability of reliable and consistent data is critical to building credibility in service delivery - especially as the achievement of debt-swap conditions is legally binding. Debt conversions could provide an opportunity for the MoH to invest in robust data systems and establish credibility in their data, both internally with the MoF and externally with their creditors and credit enhancement providers.

Implementation

chap6_img_7

chap6_img_7Structuring of the Operation

147chap6_p_147The structuring of a health debt conversion must address two fundamental objectives:

- chap6_ul_24

- chap6_li_73Maximising the financial resources allocated to the health sector, and

- chap6_li_74Ensuring alignment with the country’s public debt sustainability framework.

148chap6_p_148To achieve these goals, three critical structuring questions must be addressed at the outset: (i) identification of eligible debt instruments to be bought back, (ii) selection of the target health programme and delivery mechanism, and (iii) design of an adequate credit enhancement mechanism. While these considerations are inherently complex and context-specific, external support from specialised third-party institutions can be mobilised to provide technical expertise, analytical input and strategic guidance throughout the process. The sections below outline these questions and potential partners.

Identification of Eligible Debt Instruments for BuyBack

149chap6_p_149A debt swap must be coherent with the country’s overall debt profile and fiscal strategy. Accordingly, a preliminary economic assessment should be conducted across the public debt facilities to identify suitable debt obligations for buyback. Priority should be given to commercial debt instruments characterised by high interest costs and short-term maturities, as well as bonds trading at significant discounts.

- chap6_ul_25

- chap6_li_75Historical precedents have focused on either bond debt (e.g. Barbados, 2022; Ecuador, 2023 and 2024; El Salvador, 2024), loans (e.g. Côte d’Ivoire, 2024) or a mix of both (e.g. Bahamas, 2024).

- chap6_li_76While the focus has typically been on external debt, certain operations (e.g. Barbados, 2024) have also targeted debt instruments denominated in local currency.

150chap6_p_150While there is no one size fits all solution, the selection of targeted debt instruments must be tailored to the specific needs and debt profile of each country, with the overarching objective of maximising available fiscal space.

151chap6_p_151It is also necessary to undertake a thorough legal review of the underlying debt contracts to assess the operational feasibility of repurchasing such debt. In the case of loan instruments, particular attention should be paid to voluntary prepayment clauses (I.e. loan-specific clauses allowing the borrower to repay the loan, in whole or in part, before its scheduled maturity date) and any associated breakage costs (I.e. the financial penalty incurred when a loan or other financial arrangement is terminated earlier than agreed), which may materially affect the economic viability of the transaction.

152chap6_p_152Legal and financial advisors can assist government authorities in performing these analyses.

Selection of the Target Health programme

153chap6_p_153The health programme to be financed through the savings generated by the debt conversion must reflect a national priority and demonstrate the potential for measurable, transformative impact over the medium to long term.

154chap6_p_154Selecting an appropriate programme is essential not only for maximising developmental outcomes but also for strengthening the narrative of the transaction. A well-chosen programme can enhance stakeholder engagement and foster broad-based support for the initiative.

155chap6_p_155Global health and development institutions can support the government in selecting existing in-country programmes. In such cases, savings can constitute a top-up to the already approved programme and funding.

156chap6_p_156

157chap6_p_157Design of the credit enhancement mechanism

158chap6_p_158Incorporating credit enhancement mechanisms into the transaction structure can enable the borrower to secure more favourable financing terms - such as lower interest rates and extended maturities - thereby amplifying fiscal savings and improving the overall risk profile of the country’s public debt portfolio.

159chap6_p_159Various credit enhancement solutions are available, including partial credit guarantees, PRI or collateral arrangements. These instruments may be combined within a layered guarantee structure to optimise risk mitigation and investor confidence.

160chap6_p_160Please see Chapter 8: Credit Enhancement for more details of the different instruments.

161chap6_p_161Credit enhancement mechanisms - particularly when structured as multi-layered schemes - may entail additional costs for the borrowing country. In this context, philanthropic organisations and grant providers can play a catalytic role by contributing grant funding to cover, either partially or fully, the premiums associated with guarantees or insurance instruments. The key element is to map out all transaction and financing-related costs early on.

162chap6_p_162MDBs, DFIs and philanthropics can support governments in providing a specific guarantee instrument. Financial advisors can further support governments in brokering different credit enhancement providers and structuring multi-layered guarantee schemes.

163chap6_p_163The structuring elements outlined above are instrumental in determining the key financial parameters of the proposed transaction, most notably the total size of the facility. This amount should reflect an optimal balance between (i) the aggregate value of the debt instruments identified for the buyback, and (ii) the financial capacity of the selected credit enhancement providers.

164chap6_p_164Given that these structuring considerations fall within the respective mandates of both the MoF and the MoH, it is essential to ensure close inter-ministerial coordination throughout the design and implementation phases. Establishing a joint taskforce or working group can facilitate this collaboration, promote coherence in decision-making and enhance the overall effectiveness of the debt swap operation.

Stakeholder Engagement

165chap6_p_165Effective stakeholder engagement is also essential for ensuring its successful implementation. This engagement must be structured across two key dimensions:

166chap6_p_166Internal coordination within the government

167chap6_p_167Sustained collaboration between the MoF and the MoH is critical throughout the entire process to ensure coherence between fiscal strategies and national health priorities. In particular, the involvement of health authorities should extend across all levels of the health system - central, regional and local - and include any related national regulators where relevant, depending on the structure of the debt conversion and the nature of the targeted health programmes.

168chap6_p_168Engagement with external stakeholders

169chap6_p_169A range of external actors may be mobilised to support the transaction at various stages:

- chap6_ul_26

- chap6_li_77Global health and development institutions. Technical assistance in identifying appropriate health programmes and expenditures, support implementation, post-implementation monitoring and reporting.

- chap6_li_78Credit enhancement providers. Including (i) Multilateral and Regional Development Banks (e.g. World Bank, African Development Bank (AfDB), Asian Infrastructure Investment Bank (AIIB), European Investment Bank (EIB)) offering partial credit guarantees, (ii) insurance providers (e.g. African Trade & Investment Development Insurance, Islamic Corporation for the Insurance of Investment and Export Credit) and (iii) private insurers (e.g. AXA, Lloyds market) offering PRI instruments. Additionally, philanthropic actors (e.g. Builders’ Vision) may also contribute by financing collateral arrangements, covering guarantee premiums or subsidising interest rate reductions linked to any sustainability-linked instruments, which may also be used in the debt conversion transaction.

- chap6_li_79Credit rating agencies (CRAs). Play an important role rating (i) any new bonds that may be issued in a debt conversion transaction as the rating informs investors and lenders on the intrinsic risk of the operation and in this regard CRAs may raise issues which impact the structuring of elements of the debt conversion, and (ii) any potential implications on the sovereign credit rating. In particular, regarding the latter, CRAs will assess whether the operation qualifies as an opportunistic exchange aligned with the country’s debt management strategy or as a distressed exchange intended to mitigate imminent liquidity pressures. Where possible, early discussions should take place with the CRAs.

170chap6_p_170The participation of well-established and internationally recognised institutions can significantly enhance the legitimacy and credibility of the operation.

Reporting

171chap6_p_171Robust reporting undertakings are a cornerstone of sustainable finance, particularly in the context of debt swap transactions. Transparent and credible monitoring of both the allocation of proceeds and the resulting impact is essential to meet the expectations of global health and development institutions, as well as international investors and lenders. These requirements are reinforced by established market standards, such as the principles of the International Capital Market Association (ICMA) and the Loan Market Association (LMA) on sustainable finance.

172chap6_p_172In the case of debt conversions, three distinct types of reporting should be implemented at various stages of the transaction lifecycle:

chap6_h4_0Verification of the generated savings

173chap6_p_173This involves monitoring the execution of the debt buyback operation to confirm the actual savings generated. The timing of this verification may vary depending on the nature of the underlying debt instrument:

- chap6_ul_27

- chap6_li_80For bond-based swaps, verification can be conducted concurrently with the issuance of the new instrument.

- chap6_li_81For loan-based swaps, verification typically occurs after the transaction, once the buyback has been completed.

chap6_h4_1Verification of savings allocation

174chap6_p_174Ensuring that the fiscal savings are effectively channelled to the designated health programmes is critical. The verification process will depend on the structure of the health programme that is targeted in the debt swap operation:

- chap6_ul_28

- chap6_li_82If the programme is managed by a recognised global health or development institution, internal mechanisms may suffice, and external verification may not be required.

- chap6_li_83However, if the savings are administered through a dedicated trust fund or a bespoke financing vehicle, an independent external verification report from a verification agent will likely be necessary to ensure transparency and accountability.

chap6_h4_2Monitoring of health outcomes and impact

175chap6_p_175The relevant party (which could be the MoH and MoF, and any administering third party) must commit to reporting on the health outcomes and broader developmental impact of the financed programme. This includes tracking agreed KPIs, evaluating progress against predefined targets and assessing long-term benefits to the population, depending on the beneficiaries targeted by the programme. Some credit enhancement providers may require additional independent verification.

176chap6_p_176The capacity to deliver on these reporting requirements will vary across countries. In contexts where institutional capabilities are sufficiently developed, reporting may be conducted internally through coordinated efforts between the MoF and MoH. In other cases, technical assistance from international or regional partners may be required to support data collection, analysis and reporting.

177chap6_p_177Establishing a clear and credible monitoring framework not only enhances transparency but also strengthens investor confidence, reinforces the legitimacy of the transaction, and contributes to the broader objectives of sustainable development.

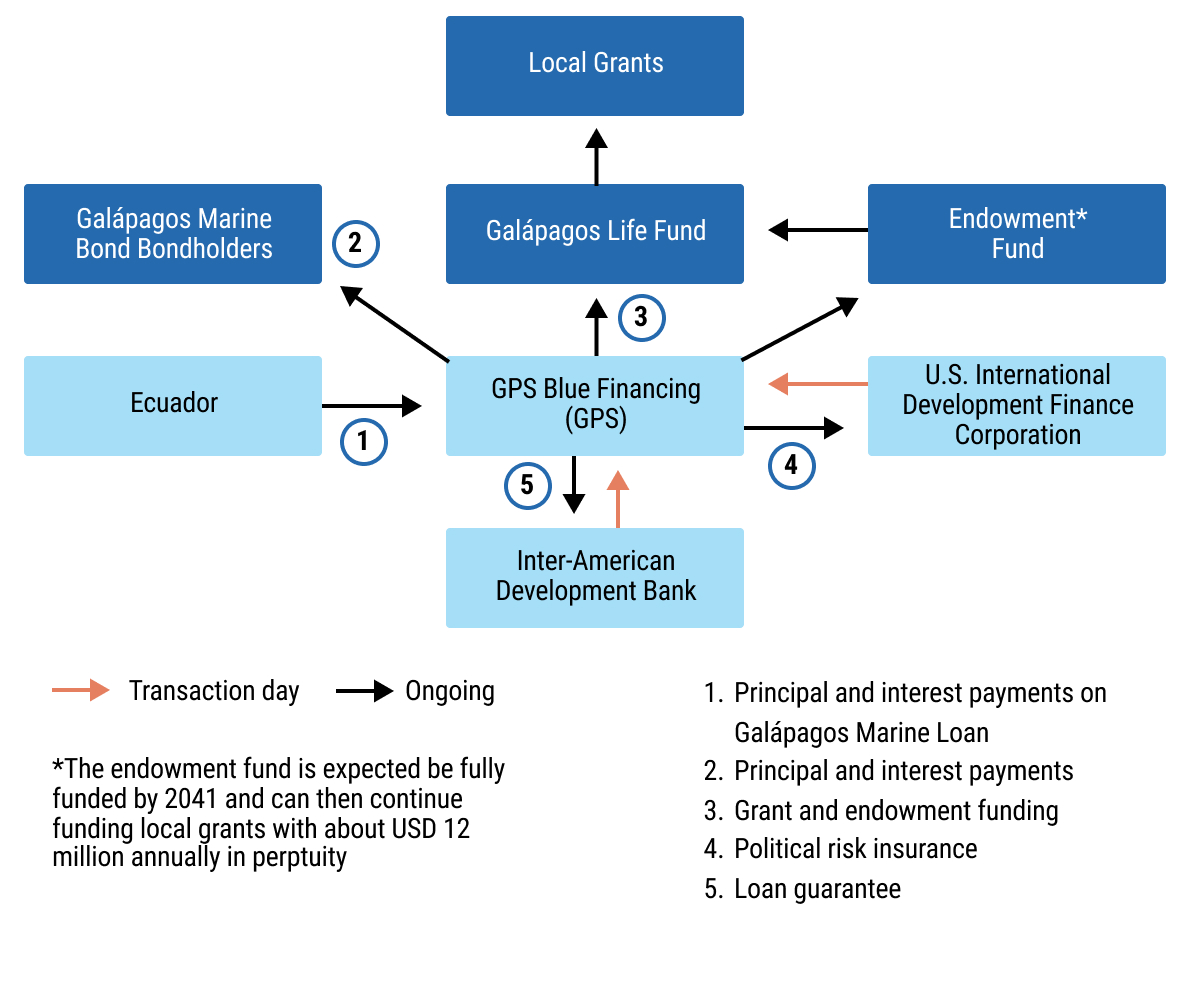

Case Study: Republic of Ecuador, Debt-for-Nature Swap (2023)178chap6_p_178In May 2023, Ecuador’s government executed a debt conversion to protect the Galápagos Islands. This innovative transaction enabled the country to exchange USD 1.63 billion of its existing high-interest commercial bonds for a new, significantly smaller USD 656 million loan, reducing the nation’s debt by nearly USD 1 billion. It is projected to save Ecuador over USD 1.1 billion in debt service payments over the term of the transaction. 179chap6_p_179The new loan was credit-enhanced with political risk insurance from the U.S. International DFC and a USD 85 million guarantee from the Inter-American Development Bank (IDB). This combination significantly lowered the borrowing cost for Ecuador, making the entire conservation funding scheme financially viable. 180chap6_p_180The transaction is projected to generate USD 450 million for marine conservation, which will be managed and disbursed over the next 18.5 years by a newly created nonprofit entity, the Galápagos Life Fund (GLF). The fund’s governance system is a public-private partnership, ensuring accountability through an 11-member board of directors. This board comprises five members from the Ecuadorian government and six non-governmental members, representing various stakeholders. This structure governs how the funds are spent on key priorities, which are tied to new conservation commitments made by Ecuador. These commitments broadly aim to strengthen the management, monitoring and enforcement of its marine protected areas and improve the overall sustainability of its fisheries. The GLF will also support scientific research and build an endowment to provide funding in perpetuity.  chap6_img_8 chap6_img_8 |

Key Legal Considerations

181chap6_p_181This section will provide an overview of the principal legal and documentation issues that typically arise in the negotiation and implementation of debt conversion transactions. It is intended to guide government officials and other potential stakeholders and transaction participants through the key instruments, contractual provisions and procedural steps involved in structuring a bilateral debt swap or debt conversion.

182chap6_p_182It begins by outlining the contractual framework for bilateral debt swaps, describing some of the main documents and key provisions that should be considered when negotiating these transactions. The second part discusses legal considerations related to debt conversions, including relevant legal documentation, credit enhancement considerations, the contractual treatment of health-related commitments and KPIs, the establishment of trust or project implementation funds, the inclusion of back-to-back funding arrangements and security structures. The discussion also outlines additional legal processes and operational considerations that are critical to execution.

Bilateral Debt Swaps

183chap6_p_183From a documentation perspective, bilateral debt swap agreements are simpler than debt conversions (described below). A bilateral debt swap is usually implemented through formal international contracts, usually comprising three tiers:

- chap6_ul_29

- chap6_li_84Intergovernmental framework agreement. This treaty-level instrument establishes the principle of the swap and is typically signed between the creditor and the debtor country. The agreement defines the total amount of debt to be cancelled or reduced and the broad purpose (e.g. for health system strengthening).

- chap6_li_85The debt swap agreement. This agreement outlines the financial and legal details of the arrangement, including the nominal amount, exchange rate, payment schedule, eligible sectors, project approval process and default provisions. The payment schedule may deviate from the initial debt repayment schedule to reflect the absorptive capacity of the programme or, if the debtor has negotiated a grace period, to ensure funds are transferred to the relevant fund, third-party entity or health project or programme. The agreement also defines how the debtor country will make counterpart payments to the fund, the implementing entity or the health project.

- chap6_li_86The implementation agreement. This agreement is usually signed between the debtor country and the implementing entity (e.g. the Global Fund). The agreement governs disbursement, fiduciary controls and monitoring.

184chap6_p_184It is important to note, however, that in a bilateral debt swap transaction, there is no standardised approach to legal documentation. In some cases, key provisions will be included in a single comprehensive debt swap agreement, while in others, various conditions and terms may be contained in separate agreements (e.g. a separate implementation agreement or trust agreement).

185chap6_p_185Two additional legal frameworks might be necessary on the creditor side:

- chap6_ul_30

- chap6_li_87Some creditors may have a nationally approved framework to support debt swaps, or they may require one that needs to be approved by their Parliament. For example, Germany’s Federal Budget Code empowers ministries to defer, reduce or write off federal claims - the core legal tool enabling debt cancellations/conversions. The Budget Act sets binding amounts annually for debt swaps.

- chap6_li_88Since the late 1980s, the Paris Club has included a debt swap clause in its agreements under specific conditions. That clause allows Paris Club creditors to convert part of their eligible claims (typically concessional loans) into a debt swap under agreed parameters. The quantitative limit is a 10-20% cap of the total restructured amount, and creditors are requested to inform other Paris Club members of any planned debt swap.

186chap6_p_186Provisions to be mindful of:

- chap6_ul_31

- chap6_li_89Debt reduction or cancellation clause. This clause specifies the scope and structure of the fiscal relief being provided in exchange for the debtor’s commitment to fund specific programmes or projects. Debtors should confirm whether relief takes the form of partial or full debt cancellation, debt reprofiling or rescheduling. In addition, to the extent that any partial write-off or cancellation has been negotiated, the debtor should suggest that this occur upfront rather than being conditional upon programme completion, so that the country obtains immediate fiscal relief. Finally, it is crucial to clarify in the documentation how and when debt obligations are extinguished - whether progressively as funds are transferred, or once the full amount is committed - and that once debt is deemed extinguished, it cannot be reinstated or clawed back by the creditor.

- chap6_li_90Transfer mechanics and schedule. This language in the debt swap agreement defines how, when and in what currency the debtor transfers freed-up resources to any designated fund, escrow account or programme administrator. When negotiating this clause, the debtor should carefully consider the duration and frequency of the transfer obligation, taking into consideration factors such as budget cycles, transaction costs, administrative simplicity and project absorption considerations. In some instances, depending on the debtor’s fiscal position, the debtor may also seek to negotiate a grace period before transfers begin to avoid budgetary strain.

- chap6_li_91Currency of transfer. Debtors typically prefer local currency transfers to align with local expenditures. However, if currency conversion is required, it is vital to ensure a fair and transparent exchange rate reference (e.g. central bank rate).

- chap6_li_92Monitoring and evaluation clause. This clause, to the extent it is included in the debt swap agreement, establishes oversight, reporting and audit mechanisms to ensure that resources are appropriately used for the agreed-upon purposes. Of note, this may also be included in a separate legal document, such as an implementation agreement. When reviewing this clause, debtors should clarify the format, frequency and responsible party for any reporting. It is also essential to avoid overly burdensome monitoring requirements that create excessive administrative costs or delays.

- chap6_li_93Transfer default and remedies clause. This clause defines the consequences of the debtor’s failure to fulfil its transfer obligations under the agreement and the remedies available to the creditor. Creditor remedies may include (i) reinstatement of the original debt (I.e. reverting to the original loan terms) and (ii) acceleration of payments under the original debt (I.e. requiring all remaining payment obligations to become immediately due). Debtors should negotiate a reasonable cure period (e.g. 2-6 months) during which the government can cure any default before the creditor can exercise its remedy rights.

Debt Conversions

187chap6_p_187Documenting a debt conversion requires a broader set of agreements than a standard bond issuance or loan transaction. The Attorney General’s Office (or equivalent) and the heads of relevant ministries’ legal departments should be aware early on of the transaction, as additional legal approvals may be required. The legal review process can also take longer due to the more structured and bespoke elements involved, which are not typical of other transactions that MoFs are accustomed to.

188chap6_p_188Negotiations often involve multiple ministries and agencies; therefore, forming a cross-government working group or task force can be beneficial. Clearly defining each ministry’s role, e.g. the MoF for liability management and funding aspects, and the MoH for health-related commitments, will help coordinate documentation, execution and ongoing monitoring. Holding regular check-ins will also facilitate this coordination.

189chap6_p_189Required documentation generally falls into the following categories:

- chap6_ul_32

- chap6_li_94Documents supporting the participation of initial stakeholders (e.g. mandate letters for lenders and arrangers, engagement letters for legal and financial advisors, appointment letters for third-party technical assistance, application for credit enhancement mechanisms)

- chap6_li_95Liability management documents (e.g. tender offer memorandum)

- chap6_li_96Debt conversion documents

- chap6_li_97Credit enhancement agreements (e.g. guarantee agreements, insurance policies)

- chap6_li_98Health-related policy and funding commitments for using the fiscal savings generated by the debt conversion

- chap6_li_99Documents establishing any trust fund or project implementation fund

- chap6_li_100Agreements for back-to-back funding, if applicable

- chap6_li_101Security and intercreditor documentation, in some cases

190chap6_p_190These are each described in more detail below.

Documentation Supporting the Participation of the Initial Participants in the Proposed Transaction

191chap6_p_191Once the sovereign has determined that it wishes to undertake a debt conversion, several third parties will need to be brought on board, and each of them will need to be mandated through a separate bilateral engagement letter with the government (usually through the MoF). This will include, inter alia:

- chap6_ul_33

- chap6_li_102Legal advisors and potentially financial advisors, who will advise on the contemplated transaction.

- chap6_li_103International and/or domestic banks, which could act as arrangers and/or underwriters of the new bond/loan at the heart of the debt conversion, as well as dealer managers in respect of any tender of the sovereign’s existing bonds (in case the debt conversion targets outstanding bonds).

- chap6_li_104Credit enhancement providers (e.g. MDBs, DFIs) typically support operations and usually require formal application requests from governments, as well as thorough due diligence processes. As such, a common understanding of these requirements, as well as any associated fees and expenses (including guarantee/insurance premia), should be sought early on. It is to be noted that these credit enhancement providers will require separate legal advice (often both international and national).

- chap6_li_105Global health institutions or NGOs can provide technical assistance on the health aspects of the operation and the health-related applications of the fiscal savings generated by the debt conversion, as well as monitoring and reporting components.

- chap6_li_106Rating agencies are typically involved at two levels: (i) rating the new debt instrument; and (ii) assessing any potential implications of the debt buyback on the sovereign rating.

- chap6_li_107Other third parties (e.g. trustee, facility agent, tender agent to manage and administer the tender offer and other parties’ legal advisors), whose roles will depend on the target operation’s structure and can be mapped out by the banks mandated to arrange the operation. Typically, banks will obtain quotes from two or three providers of such services to ensure competitive pricing and optimisation of transaction costs for the government.

192chap6_p_192Procurement/Request For Proposals (RfPs)

193chap6_p_193Thought will need to be given to any country-specific procurement processes to mandate the required parties or other ways of doing so, which will comply with national requirements - such requirements may lead to the need for an RfP to be drafted to invite financial advisors, legal advisers and banks to submit proposals to the MoF. These can be very useful, as would interviewing parties submitting proposals. The scope of each such mandate, as well as timing and fee coverage, will need to be clearly established (typically in a mandate or engagement letter).

194chap6_p_194At this initial step, and given the number of participants, it will be critical to ensure alignment across all parties on (i) the technical and commercial parameters of the deal, and (ii) the overall execution timeline - especially as the disbursement date should be in line with the overall MoF’s funding plan for the year.

195chap6_p_195Other documents

196chap6_p_196As such, beyond the bilateral mandate and engagement letters, four other documents can be elaborated and circulated to all relevant parties:

- chap6_ul_34

- chap6_li_108A financial model is used to map out the overall costs of the transaction and debt servicing costs. There should be a regular review of the model as the transaction moves from concept to execution. This model can be elaborated and maintained by the MoF team and its financial advisor.

- chap6_li_109A Term Sheet with the main commercial and legal parameters of the proposed transaction. This can ensure that, before moving to the full documentation stage, all the parties agree on the main parameters of the debt conversion.

- chap6_li_110A detailed execution timeline mapping out the different workstreams (e.g. alignment on commercial terms, negotiation of all legal documents, selection of all third parties, approval of the project by the credit-support providers’ boards, government approvals, ratings).

- chap6_li_111A document list with allocated responsibilities, indicating who has primary responsibility for drafting each document, the parties involved, who will review the document, and its position in any timeline.

197chap6_p_197Partners

198chap6_p_198In large debt conversion transactions involving multiple parties and legal advisors, having a strong coordinating partner can make a significant difference to the success of transaction execution, and it should be clear from the outset who will assume this role. In past transactions, this has ranged from a presidential advisor to a minister, the external financial advisor to the MoF or even an arranging bank. If a party outside of government, there should be clear lines of access to senior government officials and staff.

Confidentiality

199chap6_p_199Whilst the country is working on a debt conversion, it is often preferable that this should remain confidential. Where the subject of the debt conversion is publicly traded bonds in the capital markets, this is especially important, as the bond price may rally upon such information being known, and the fiscal savings the country seeks to obtain may diminish. The need to maintain confidentiality also applies to any credit enhancement providers who may inadvertently disclose a proposed transaction through the process of obtaining board approval. For example, early discussions should address these guidelines and any related measures put in place with all parties to the transaction and their respective employees/officials.

Liability Management Documentation

200chap6_p_200At the heart of many transactions is the buying back of sovereign bonds. The greater the discount at which such bonds are trading, the greater the fiscal savings that could be generated from the debt conversion. The buyback component of the transaction is similar to any simple liability management transaction that a country would undertake as part of its day-to-day debt management strategy, based on a cash tender offer.