Key Takeaways

|

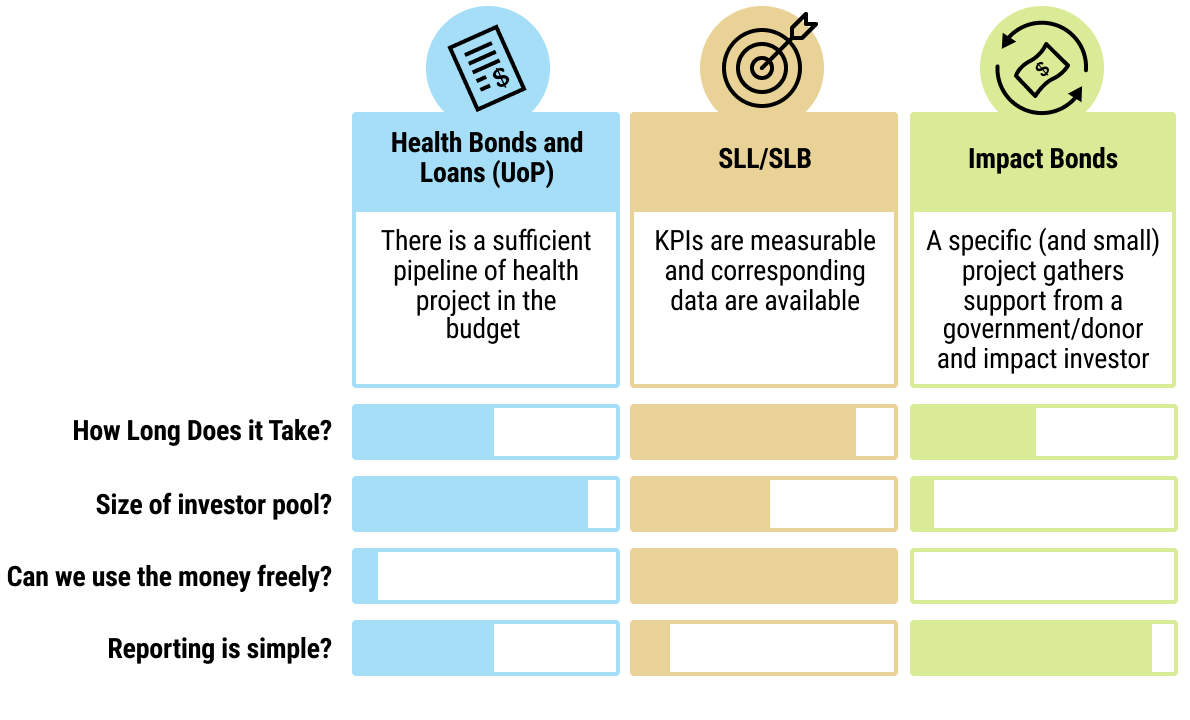

1chap5_p_1This chapter aims to guide officials from Ministries of Finance (MoFs) and Ministries of Health (MoHs), as well as practitioners, on the design and implementation of sustainable financing instruments - specifically UoP and sustainability-linked bonds (SLB) and sustainability-linked loans (SLL) - as mechanisms to mobilise public and private capital for health objectives. These instruments represent two complementary approaches to integrating sustainability into financing strategies: one through the earmarking of funds for eligible health-related projects (the UoP approach), and the other by linking financial terms to measurable health and sustainability performance (the sustainability-linked approach).

2chap5_p_2Three types of financing instruments are covered in this section:

- chap5_ul_1

- chap5_li_5Health bonds and loans. Models based on the UoP approach and would require the country to earmark the funds raised towards health projects and activities, such as infrastructure development or disease-specific programmes. This commitment will be contractually binding and must be reflected in the mandatory annual allocation reports. Therefore, robust project selection, transparent fund management and rigorous reporting are essential to ensure that resources achieve their intended outcomes and to maintain investor confidence.

- chap5_li_6SLBs and SLLs. Instruments in which the cost of financing is directly contingent upon the achievement of predefined sustainability targets. In the health sector, these targets could include expanding access to essential health services through improved health workforce availability or the expanded utilisation of quality services, such as for human immunodeficiency virus (HIV) patients with suppressed viral loads. When targets are met or exceeded, issuers benefit from more favourable financial terms; conversely, underperformance triggers penalties or adjustments, thereby incentivising continuous improvement.

- chap5_li_7Impact bonds. Performance-based approach bonds involving contractual arrangements between a government and/or donor and investors. In these arrangements, the government and/or donor commit to making payments contingent on the achievement of pre-agreed outcomes, specifically health-related objectives. These instruments typically operate on a more limited scale, but still offer a targeted mechanism for linking financing to measurable impact.

chap5_img_0

chap5_img_0

Financing Sustainable Health

3chap5_p_3Globally, the issuance of these instruments has grown rapidly in emerging markets, with UoP structures still dominating the market. Sustainability-linked financing, although less common, is gaining traction as performance-based mechanisms are seen to reflect progress toward national sustainable development goals better. In Africa, over 150 sustainable UoP bonds have been issued in both foreign and local currencies, totalling more than USD 15 billion. South Africa, Nigeria, Egypt and Côte d’Ivoire lead in terms of volume and diversity of instruments. A notable milestone occurred in August 2025, when Côte d’Ivoire issued Africa’s first foreign currency-denominated sustainability-linked loan, supported by the World Bank.

4chap5_p_4International financial institutions and development banks increasingly promote these instruments for their potential to channel private capital into sustainable development across the region. Together, they offer governments and health authorities practical tools to mobilise private resources while aligning debt management strategies with national development and sustainability objectives.

Health Bonds and Loans (UoP)

Case Study: Differences Between Bonds and Loans5chap5_p_5Throughout this chapter, reference to two distinct debt instruments will be made: (i) loans and (ii) bonds.

6chap5_p_6Summary of main differences

22chap5_p_22For further details of the range of creditor types, instruments and financing structures, see the African Legal Support Facility’s (ALSF) handbook Understanding Sovereign Debt: Options and Opportunities for Africa. |

Description and Rationale

23chap5_p_23Unlike traditional debt instruments that finance general budget needs, UoP bonds and loans allocate funds to projects with clear environmental or social benefits. There are three main types.

- chap5_ul_3

- chap5_li_10Green bonds/loans. Finance environmental initiatives (e.g. renewable energy, forestry, marine conservation).

- chap5_li_11Social bonds/loans. Support social programmes (e.g. healthcare, education, gender equality).

- chap5_li_12Sustainable bonds/loans. Combine both environmental and social objectives.

24chap5_p_24A health bond or loan would fall under the social category, funding health-related expenditures such as hospital construction, medical equipment purchases, vaccination programmes and improved access to care.

25chap5_p_25UoP instruments are not new - they have been widely used for years by governments, development banks and corporations, including in Africa. They operate under internationally recognised guidelines set by two key market bodies: the International Capital Market Association (ICMA) for bonds and the Loan Market Association (LMA) for loans. These guidelines are, in principle, voluntary, but in practice, it is highly recommended to follow them.

26chap5_p_26For sovereign borrowers, UoP instruments offer four significant benefits:

- chap5_ul_4

- chap5_li_13Alignment with global standards. Clear, comprehensive and regularly updated guidelines enhance transparency and credibility.

- chap5_li_14Reputation building. Health bonds and loans generate positive visibility, allowing governments to showcase their development strategies and highlight ongoing policies and projects.

- chap5_li_15Investor confidence. These instruments are familiar to investors, who value the assurance that funds are earmarked for specific, budget-identified projects aligned with social goals.

- chap5_li_16Unlocking new funding sources. UoP issuance attracts investors focused on social impact and taps into environmental, social and governance (ESG)-dedicated funding sources.

Enabling Conditions

27chap5_p_27The following enabling conditions establish the institutional and operational foundation necessary to support a credible and successful health bond issuance or loan contraction.

28chap5_p_28High-level political buy-in. Strong political leadership is indispensable to overcoming bureaucratic barriers and facilitating cooperation across ministries, agencies, and government departments. Issuing and managing health loans and bonds throughout their life cycle requires a high degree of inter-ministerial coordination, which can be challenging without a political champion, typically originating from either the MoH or the MoF (for example, the head of the debt management office (DMO)).

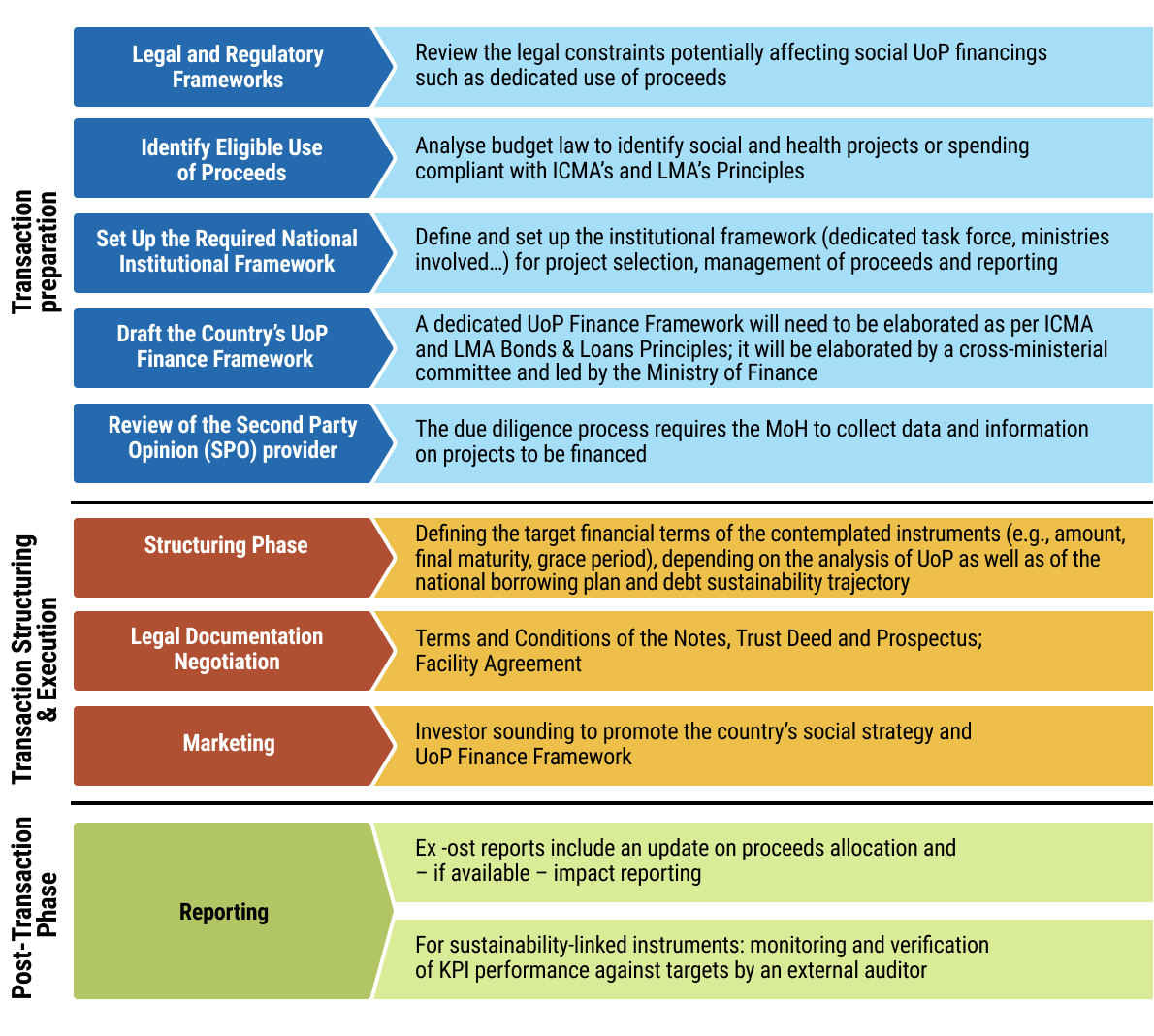

29chap5_p_29Conducive legal and regulatory frameworks. A country’s statutory, legal and regulatory framework defines how public borrowing is authorised and managed. It typically covers borrowing approvals, parliamentary oversight, debt contracting and recording procedures and limits on government borrowing or guarantees. For health bonds or loans, national frameworks must allow - or at least not prohibit - earmarked borrowing for specific purposes, such as health programmes. If the legal framework is silent or unclear, governments should consider amending laws to explicitly authorise debt for defined policy objectives (e.g. health). Such clarity reduces legal risk and strengthens investor confidence in the legitimacy and enforceability of the instrument.

30chap5_p_30Experience and market readiness. Countries with experience issuing foreign-currency bonds or contracting external loans are generally better positioned to adopt a UoP framework for health. While prior issuance of conventional debt is not a requirement, it helps build investor relationships - a sound foundation before moving to more specialised instruments like health-linked debt. Regardless of experience, early engagement with international investors is critical. This dialogue helps clarify their expectations, particularly around which health expenditures are most attractive to the market. These insights allow governments to design the structure of the operation in a way that maximises investor interest and confidence.

31chap5_p_31Sufficient project and expenditure pipeline. Before issuing a health bond or loan, the government needs to identify a sufficiently large amount of eligible health expenditures in its budget to match the target amount of the new debt. Typically, for a health bond in the international capital markets, a country would ideally identify health-related projects/programmes requiring funding from the national budget of at least USD 500 million, typically spent over 2-3 years. Smaller transactions could nevertheless be privately placed in the bond markets with a smaller group of investors or funded through loans. It is important to note that governments retain flexibility on the list of expenditures to be financed by the new debt instrument:

- chap5_ul_5

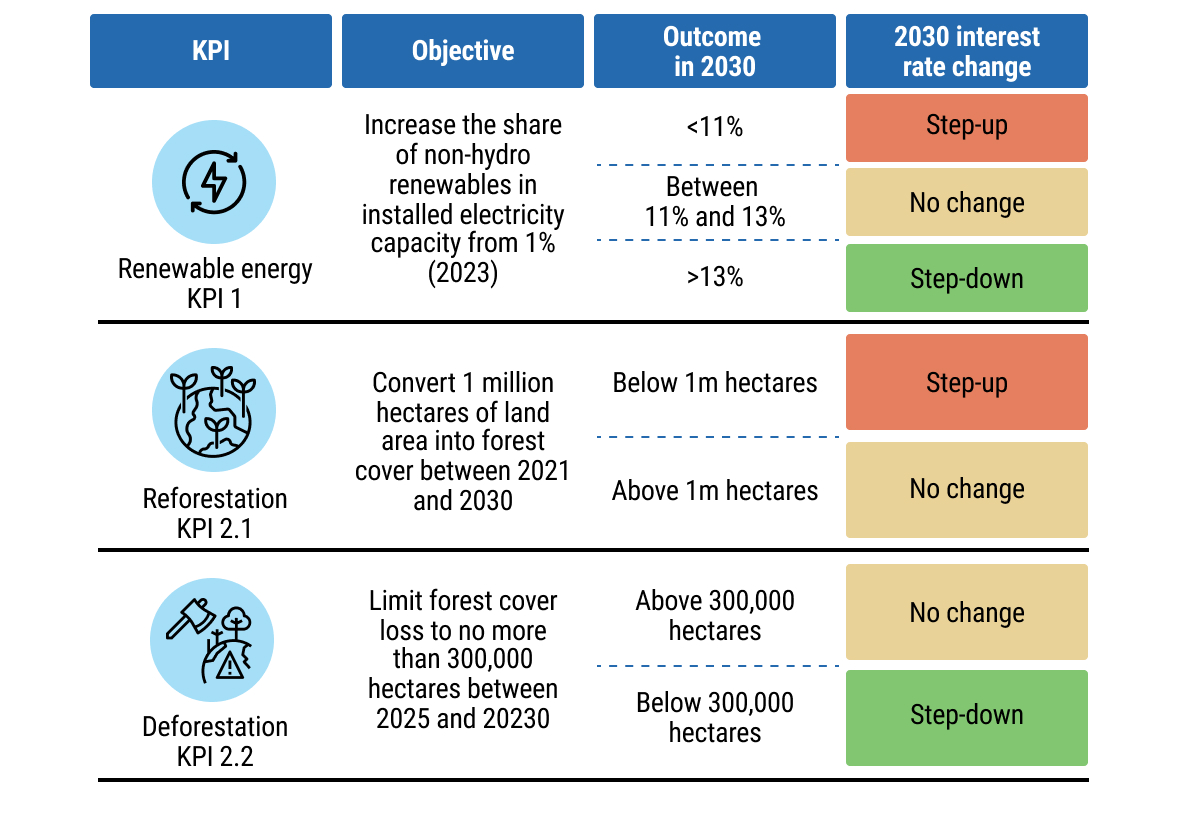

- chap5_li_17Multi-year allocation. Eligible expenditures can span several fiscal years. For example, a bond issued in 2026 can cover past (2025) and future (2026-2028) health spending.

- chap5_li_18Adjustable list. The exact list of expenditures does not need to be finalised at issuance. Governments can update it later during the subsequent reporting phase, based on actual budget execution.

- chap5_li_19Broader scope. Expenditures do not have to be limited to health: governments could opt for a broader social bond or loan, where health can be combined with other social sectors (e.g. education).

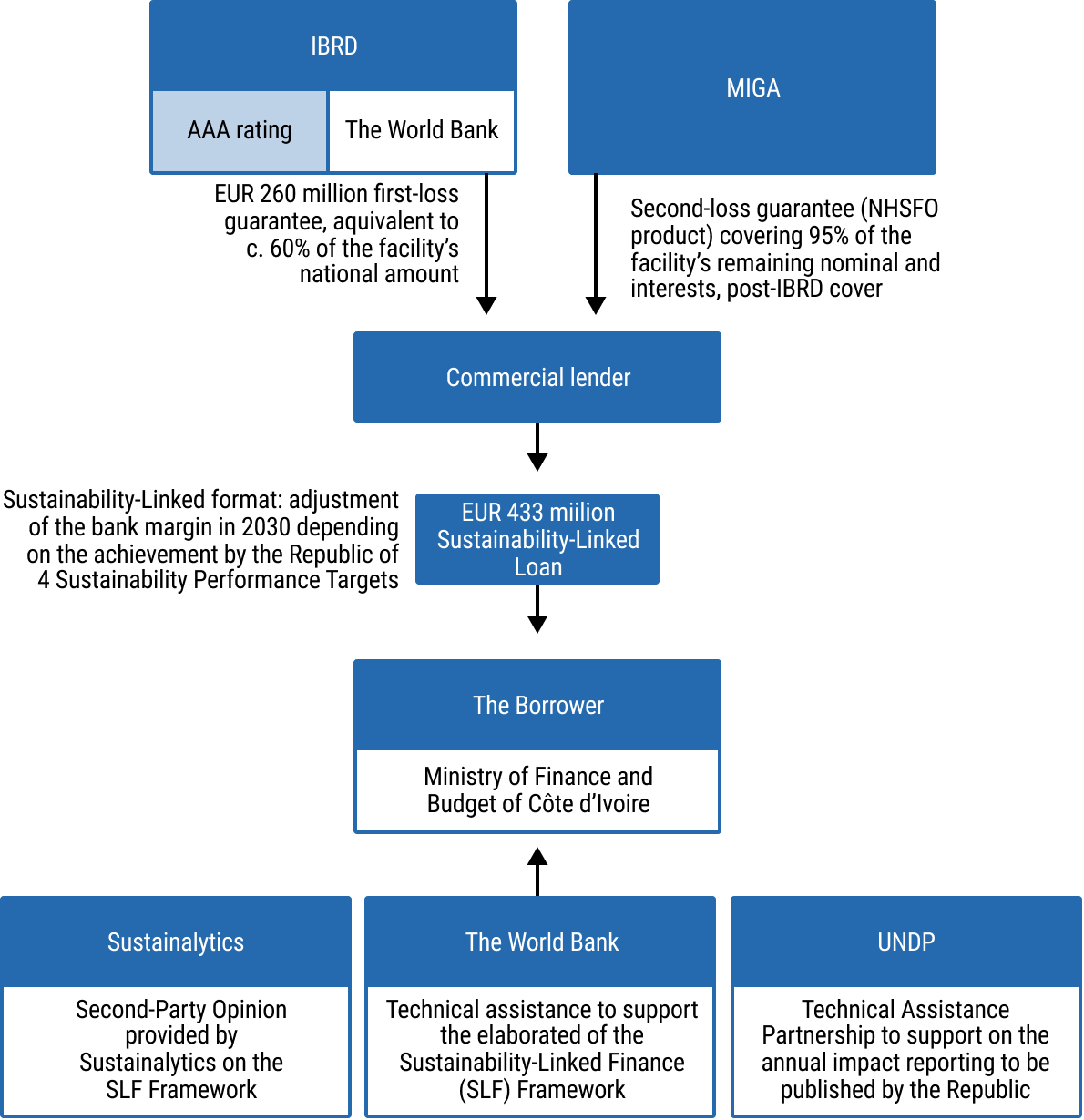

Opportunities and Challenges

Opportunities

- chap5_ul_6

- chap5_li_20Significant issuance potential. UoP instruments can mobilise substantial financing volumes, particularly when structured as a bond issued on international markets.

- chap5_li_21Market familiarity. Based on well-established ICMA and LMA frameworks, UoP bonds and loans are easily understood by investors, enhancing demand.

- chap5_li_22Visibility and credibility. Linking borrowing to health-related expenditures strengthens the government’s social commitment and improves investor confidence. A case can even be made that increased health expenditures can support economic growth and, ultimately, debt sustainability.

- chap5_li_23Access to a broader pool of investors. Socially responsible and ESG investors are more likely to participate in addition to the existing investor base, increasing the chances of success for these instruments.

Challenges

32chap5_p_32Complex transaction preparation. Developing a dedicated national social or health bond or loan framework aligned with relevant standards like ICMA or LMA takes time and coordination across key ministries (e.g. MoH). It is resource-intensive and demands strong administrative commitment and technical capacity. In addition, identifying sufficient eligible expenditures in the budget to meet the minimum transaction size (especially for bonds) might be challenging for some countries.

33chap5_p_33Firm reporting commitments. Borrowers must report annually on how proceeds are used until all funds are allocated. Reports detail financed programmes and may showcase flagship projects with expected impacts. While not mandatory, investors often request third-party audits for added assurance. This process can be demanding and requires close collaboration between the DMO, the budget department and relevant ministries (I.e. the MoH). Meeting these standards on time is crucial to establishing credibility as an ESG issuer and enhancing future market access. Importantly, reporting requirements can be legally binding - failure to comply may trigger events of default with serious consequences for the country.

Implementation

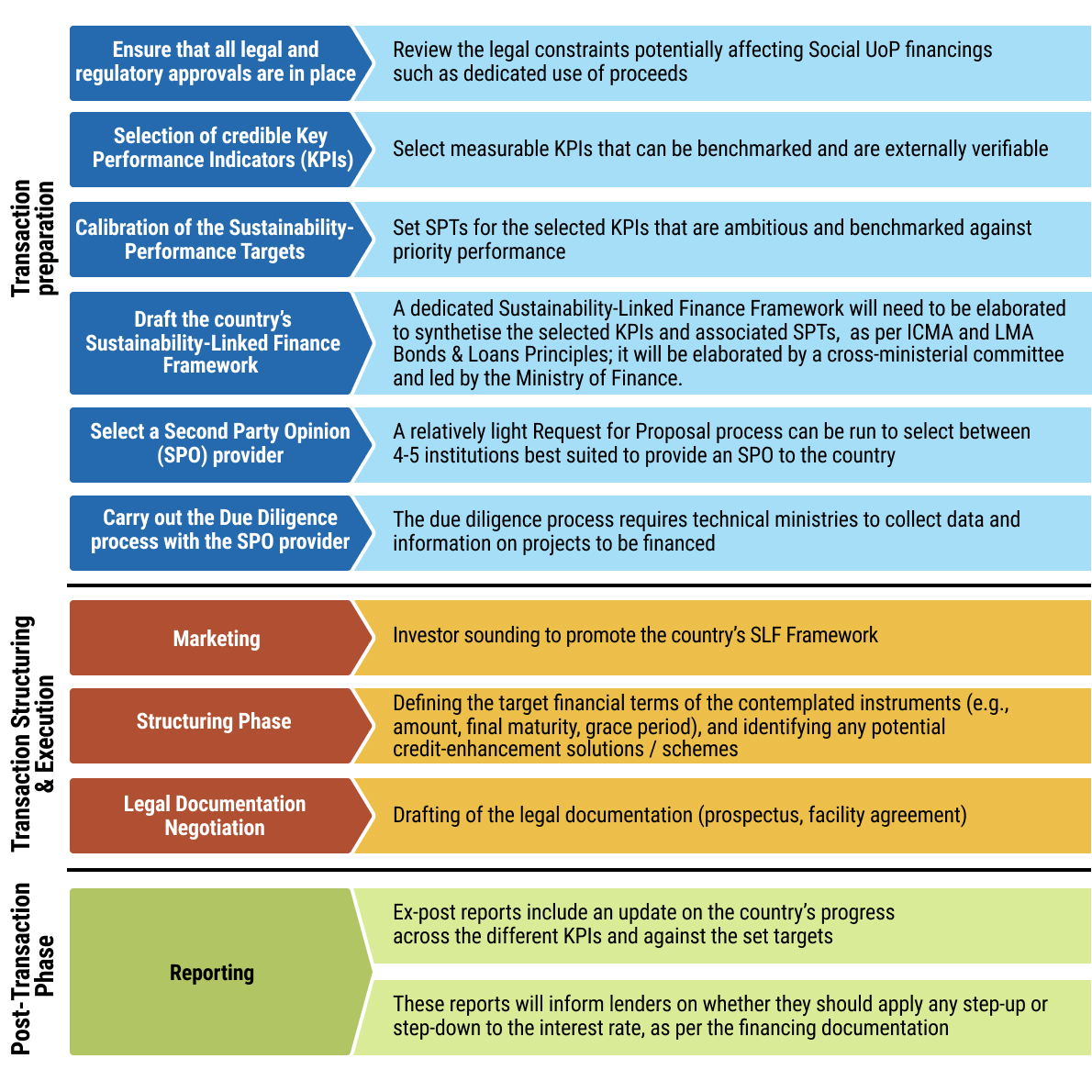

34chap5_p_34Issuing a UoP debt instrument will require thorough preparation and specific execution workstreams compared to more standard debt instruments. Figure 5.3 below summarises a checklist of all activities that need to be conducted through the process.

chap5_img_1

chap5_img_1

35chap5_p_35Across this process, three elements are core to UoP debt financing.

- chap5_ol_0

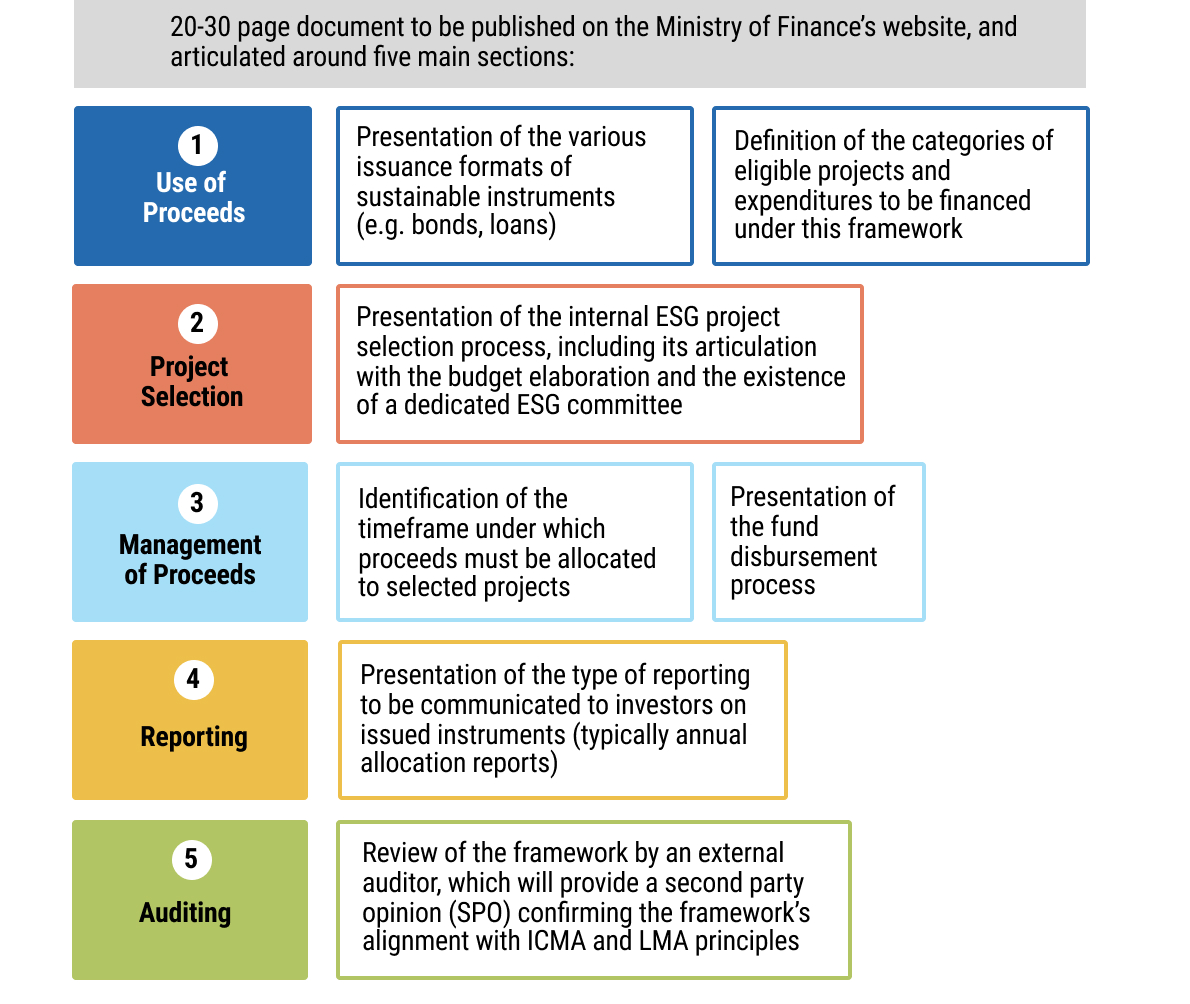

- chap5_li_24Preparation of a dedicated UoP Finance Framework for health. If the ICMA or LMA guidelines are being followed, the national framework will be mandatory for any borrower that wants to issue a UoP debt instrument on the international markets. The Framework serves as the reference for all future UoP issuances. It aims at (i) presenting the country’s national social and/or health priorities, (ii) defining clear eligibility criteria to select expenditures and projects financed by UoP instruments (e.g. health-related spending), and (iii) presenting the country’s governance structure in charge of selecting eligible expenditures and managing reporting. Such Frameworks need to be reviewed by an external third party, which will provide a second party opinion (SPO) confirming the document’s alignment with international standards. The Case Study below details the content and format of a UoP Finance Framework.

Case Study: Format and Content of a UoP Finance Framework chap5_img_2 chap5_img_2 |

- chap5_ol_1

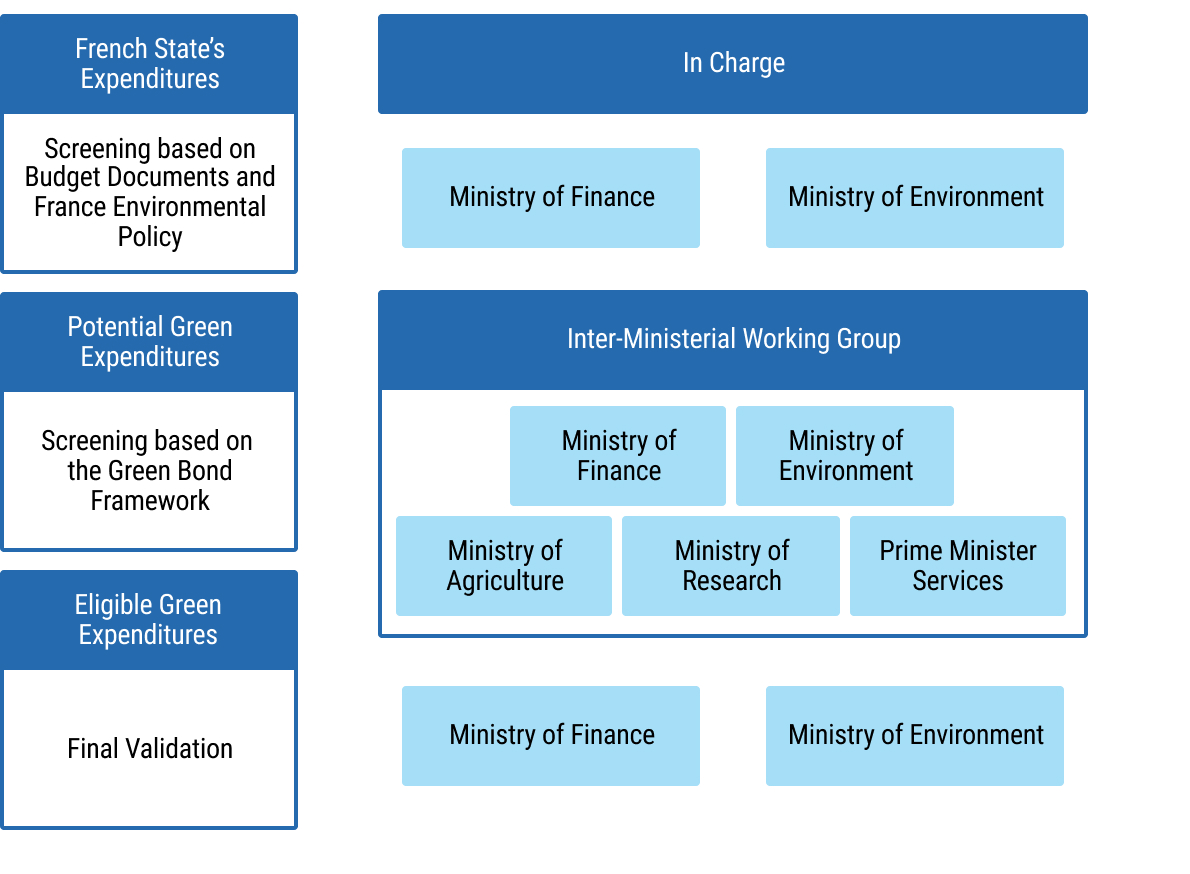

- chap5_li_25Extensive stakeholder engagement. Health bonds and loans require coordination among various key stakeholders throughout the process (see example of France in the Case Study below). The MoF and its DMO typically lead the process, ensuring alignment with government priorities and managing structuring and negotiations with investment banks and advisors. The MoH provides sector expertise, confirming that the proposed health-related eligibility criteria outlined in the UoP Finance Framework align with existing health plans. The Attorney General’s office or the Ministry of Justice ensures legal compliance by issuing necessary approvals and opinions. To streamline this complex process, it is recommended that a dedicated task force be created to oversee each step and maintain coordination among all parties.

Case Study: Example of the French UoP Bond - Selection of Eligible Expenditures and Interministerial Coordination chap5_img_3 chap5_img_3 |

- chap5_ol_2

- chap5_li_26Robust monitoring, reporting and verification (MRV). Post-issuance obligations for health bonds or loans involve three main areas, which should be documented in the UoP Finance Framework:

- chap5_li_27Monitoring eligible expenditures. The MoF (typically with the Budget Directorate) tracks eligible spending in the national budget, ensuring it matches the total debt issued and is disbursed within a reasonable timeframe (usually within two to three years). To facilitate this process, expenditures and budget execution must be easily traceable in the accounting system.

- chap5_li_28Reporting to investors and the public. Annual allocation reports, which synthesise how funds were distributed throughout eligible budget expenditures, are mandatory for UoP debt instruments as per ICMA and LMA Principles. Although not compulsory, borrowers can also provide impact reports, depending on the availability of data. Reports would usually be co-drafted by the Finance and Health ministries and published on the MoF’s website.

- chap5_li_29Independent verification. Although not compulsory, it is strongly recommended to have an external third-party audit the reports to provide a limited assurance audit report. This is often a requirement by investors and lenders.

- chap5_ul_7

Sustainability-Linked Bonds and Loans for Health

Description and Rationale

36chap5_p_36SLBs and SLLs are especially suited for sovereigns in need of flexible funding, while embedding health goals. Unlike UoP debt instruments, there is no restriction on specific line-item or project spending. Instead, the country will commit to achieving pre-agreed performance targets on environmental and/or social key performance indicators (KPIs) within a specified time horizon. The cost of financing SLBs and SLLs will be tied to the borrower’s performance across these KPIs:

- chap5_ul_8

- chap5_li_30If the pre-defined performance targets are successfully met, the borrower may benefit from an interest rate step-down. This means that for the remaining duration of the instrument, the lenders will reduce the interest amounts that the borrower will need to service.

- chap5_li_31If the targets are not met, the borrower may suffer an interest rate step-up. In this case, lenders will increase the interest amounts that the borrower will need to service until the end of the instrument’s life.

37chap5_p_37The selection of the KPIs and associated performance targets (commonly referred to as sustainability performance targets (SPTs)) should reflect the borrower’s national social and/or health commitments. It will be thoroughly monitored and verified throughout the life of the SLB/SLL. As such, KPIs should be relevant, material, quantifiable and externally verifiable metrics that can be reliably benchmarked against standard-setting norms (ICMA/LMA). The associated targets should be ambitious and represent a material improvement beyond a business as usual scenario (I.e. without funding).

38chap5_p_38SPTs and KPIs also play a crucial role in securing credit enhancement from international institutions that aim to support the health sector. See Chapter 8: Credit Enhancement for more details.

Case Study: Republic of Côte d’Ivoire - Sustainability-Linked Loan Structured with the Support of the World Bank (August 2025)39chap5_p_39In August 2025, the Republic of Côte d’Ivoire issued its first EUR 433 million SLL, building on its inaugural Sustainability-Linked Finance Framework published in June 2025, with the support of the World Bank Group. 40chap5_p_40This Framework is articulated around 3 KPIs in the forestry and energy sectors. For each KPI, an SPT has been defined, to be achieved by the Republic by 2030 and which would result in interest rate changes from 2031 until the final maturity of the loan (2040). The table below summarises these KPIs and SPTs.  chap5_img_4 chap5_img_4 |

|

41chap5_p_41The SLL issued based on this Framework has benefited from strong support from the World Bank Group: it was the first-ever combination of two different World Bank guarantee products: (i) a Policy-Based Guarantee by the International Bank for Reconstruction and Development (IBRD), and (ii) a Non-Honouring of Sovereign Financial Obligations by the Multilateral Investment Guarantee Agency (MIGA). The graph below highlights the highly innovative structure.  chap5_img_5 chap5_img_5 |

Enabling Conditions

42chap5_p_42Strong political buy-in. Strong political leadership is essential to ensure coordination across ministries and agencies - especially for SLBs/SLLs, which require more collaboration than UoP instruments. These instruments involve continuous monitoring of KPIs and SPTs throughout their life. The MoH must have adequate resources to meet its targets, while the MoF needs regular updates to report to investors. Identifying a political champion can help sustain this long-term effort. Leadership and ownership should ideally come from both the MoF (via the DMO or directly) and the MoH. To manage the process efficiently, establishing an interagency coordination body is recommended.

43chap5_p_43Conducive legal and regulatory frameworks. Similar to health bonds and loans described above, the borrowing country’s statutory, legal and regulatory framework must also allow for the issuance of a sustainability-linked debt instrument or be supplemented to do so. However, because SLL and SLBs do not specify the use of funds, countries should not be constrained by legal restrictions related to the earmarking of funds.

44chap5_p_44Robust data infrastructure. SLBs and SLLs require strong, reliable data that investors can trust. According to ICMA and LMA Principles, KPIs must be relevant and material to economic, social and governance policies, aligned with national sustainability priorities such as health strategies, measurable using consistent methodologies, externally verifiable and benchmarkable.

45chap5_p_45Health-related KPIs can be particularly challenging due to poor data quality, reliance on infrequent surveys, limited historical records and gaps in coverage. Some areas, like HIV/AIDS screening, are well supported by data, while others, such as non-communicable diseases, lack robust information because many cases go undetected. These gaps must be addressed to ensure transparency, verification and credible reporting. National authorities responsible for health data, such as the Statistics Office and the MoH, should regularly confirm their ability to collect and report reliable data. Ultimately, KPIs should be chosen based on the quality, availability and verifiability of the underlying data.

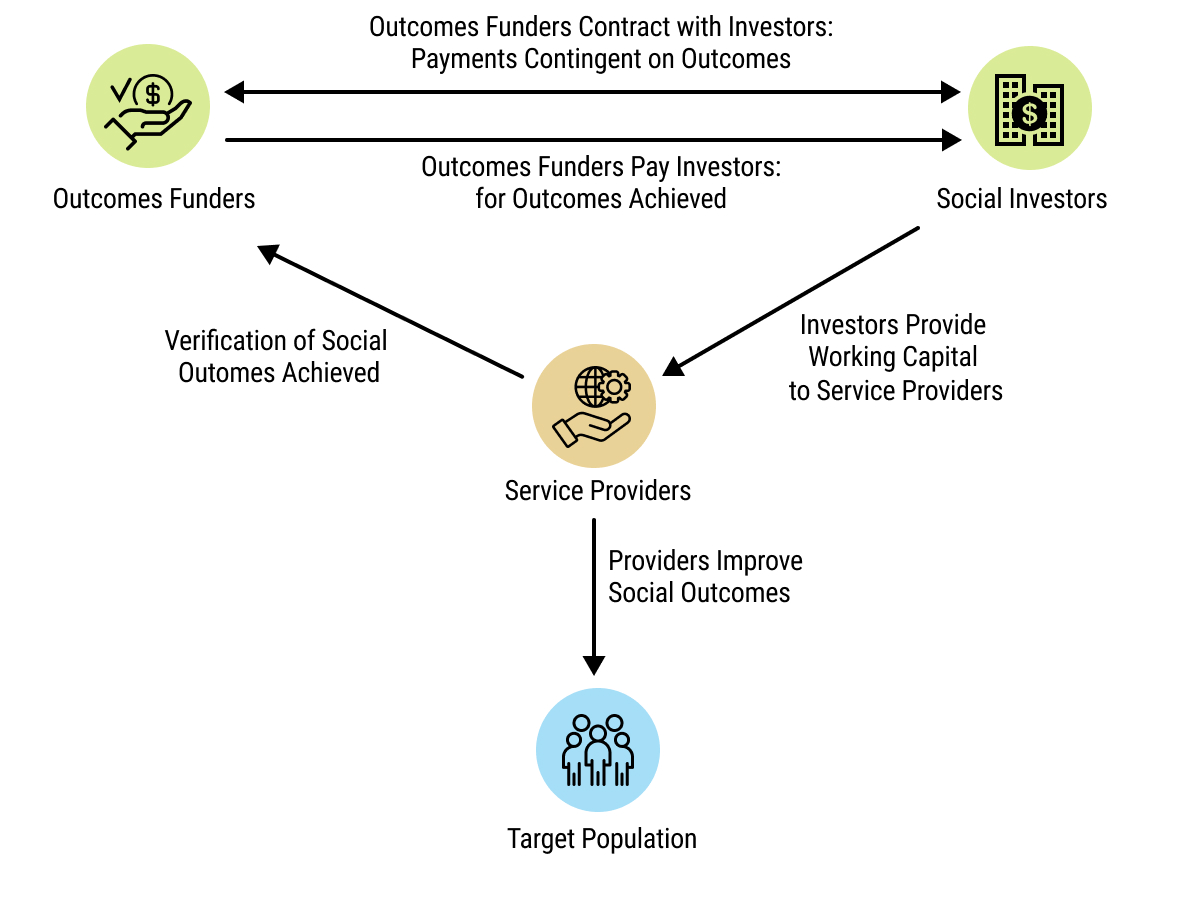

Opportunities and Challenges

Opportunities

46chap5_p_46Significant issuance potential: Similar to health bonds and loans, SLBs/SLLs can mobilise substantial financing volumes, particularly when structured as a bond issued on international markets.

47chap5_p_47Access to a broader pool of investors. Issuing SLBs or SLLs with health-related KPIs should expand the country’s investor base, appealing to social and ESG-focused funds and institutional investors that need to meet and report on sustainability targets. Most importantly, improvements in health not only deliver social benefits but should also support economic growth, creating an additional incentive for investors to engage with the country.

48chap5_p_48Gathering support from development finance institutions. In addition, these instruments could unlock interest from development finance institutions (DFIs), which could provide innovative credit-enhancement schemes. (See Chapter 8: Credit Enhancement). Global health institutions (GHIs) could also be engaged to provide technical assistance to MoHs in selecting their KPIs. Together, these could lower borrowing and transaction costs.

49chap5_p_49Flexible use of funds. Unlike health bonds and loans, SLBs/SLLs allow issuers to use funds for general budgetary needs while embedding agreed sustainability commitments, making them particularly attractive to sovereign borrowers balancing health goals with economic priorities. The money raised can also be used to repay pre-existing debt (e.g. but not exclusively, as part of a debt swap operation. For more information see Chapter 6: Debt-for-Health Swaps.)

50chap5_p_50Driving long-term health policy alignment. Sovereign SLLs and SLBs can be designed to drive policy change by linking borrowing costs to performance. Missing agreed targets can increase financing costs, therefore creating a strong incentive for governments to allocate sufficient resources to health. For example, a transaction could include a commitment to update a Universal Health Care law to provide free maternal health services.

Challenges

51chap5_p_51Credibility and KPI enforcement. Weak or vague health KPIs risk undermining the effectiveness of SLBs and SLLs. Ensuring that targets are material, ambitious, measurable, independently verified and aligned with ICMA or LMA Principles mitigates these concerns. Governments can seek technical assistance from GHIs or other implementation partners to strengthen their national MRV systems.

52chap5_p_52Investor awareness and market depth. The market for health-related SLBs and SLLs is still emerging, as most sustainability-linked issuances have focused on climate or nature KPIs. Building investor confidence will require transparent reporting and standardised KPI frameworks. Conducting investor soundings alongside the development of a Sustainability-Linked Finance Framework, as Côte d’Ivoire did in 2025, helps ensure that KPIs and SPTs align with market expectations. In parallel, multilateral development banks (MDBs) and other credit enhancement providers should advocate with private lenders to encourage the broader adoption of sustainability-linked instruments, including the acceptance of more meaningful interest step-downs than are currently offered.

53chap5_p_53Need for capability-building. Many sovereigns lack experience in integrating health KPIs into financial instruments and structuring adequate SLBs/SLLs. Policy and technical support, capacity building and regulatory guidance from multilateral institutions can strengthen implementation.

54chap5_p_54Complex transaction preparation. Developing an SLL/SLB framework aligned with relevant standards like ICMA or LMA takes time and coordination across key ministries (e.g. MoH, MoF). However, this framework can be reused in the future: if the government wants to issue another bond, the existing framework can be expanded to include other KPIs in the Framework (see Case Study on the example of Chile below).

Case Study: Evolution of the SLB Framework in Chile, Including Social KPIs55chap5_p_55In its initial SLB Framework, published in March 2022, Chile established two KPIs with their corresponding SPTs. 56chap5_p_56The KPIs are as follows: 57chap5_p_57KPI 1. Greenhouse gas (GHG) emissions per year, measured in metric tons of carbon dioxide equivalent. 58chap5_p_58KPI 2. Non-conventional renewable energy generation. 59chap5_p_59Later, in June 2023, considering the relevance of gender equality and social factors to the country, which were also reflected in the previous expansion of its Green Bond Framework to include social projects, a similar approach was followed in the SLB Framework, incorporating an additional KPI. 60chap5_p_60The new KPI is as follows: 61chap5_p_61KPI 3. Women’s representation on corporate boards is typically measured as a percentage of the total number of board members. |

Implementation

62chap5_p_62Issuing a sustainability-linked debt instrument will require thorough preparation and specific execution workstreams compared to conventional debt instruments. Table 5.1 below summarises a checklist of all activities that need to be conducted through the process.

chap5_img_6

chap5_img_6

- chap5_ol_3

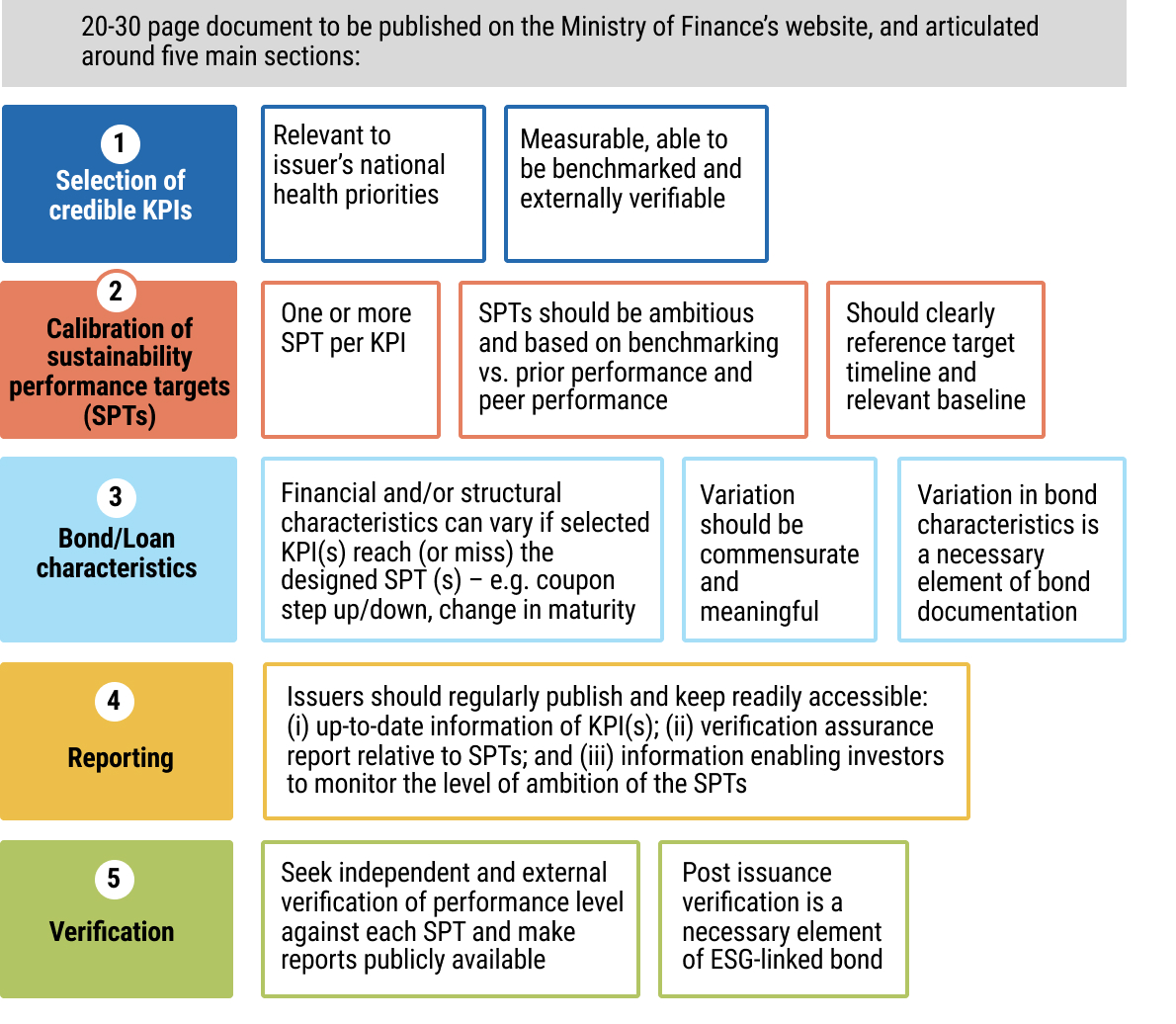

- chap5_li_32Preparation of a dedicated Sustainability-Linked Finance Framework. Similar to health bonds and loans, having this national framework is a mandatory requirement by ICMA and LMA for any borrower that wants to issue a sustainability-linked debt instrument on the international markets aligned with their Principles. The existence of a national strategy with clear health policy priorities will be crucial in developing the Framework, particularly in selecting KPIs and calibrating SPTs. Indicators and targets should be sufficiently ambitious to ensure the Framework’s credibility and attract investor interest, yet realistic given the country’s capacity for monitoring, reporting and verification. The MoH should play a leading role in developing any such Framework, in close collaboration with the MoF.

Case Study: Format and Content of a Sustainability-Linked Finance Framework (In Line with ICMA and LMA Principles) chap5_img_7 chap5_img_7 |

- chap5_ol_4

- chap5_li_33Strong stakeholder engagement. Like health bonds and loans, SLBs and SLLs require close coordination among key stakeholders. The MoF and its DMO typically lead the process, ensuring alignment with government priorities and managing structuring and negotiations with investment banks and advisors. The MoH plays a critical role in defining and selecting appropriate KPIs and targets, bringing sector expertise to the design phase and ensuring alignment with existing national health plans.

- chap5_li_34Robust financial structuring. The structure of the instrument, including the total amount, final maturity and any credit-enhancement mechanism, must be carefully aligned with the country’s debt-carrying capacity to avoid creating undue fiscal pressure. Equally important is the calibration of interest step-down and step-up mechanisms associated with the SPTs. These adjustments should be meaningful enough to incentivise governments to meet their targets and not incur additional interest payments, while remaining realistic and proportionate to the country’s fiscal capacity. Striking this balance ensures that the financial structure reinforces policy objectives without compromising debt sustainability.

- chap5_li_35Monitoring, reporting and verification. Regarding a health bond or loan, sustainability-linked instruments will require thorough annual reporting to be executed following the completion of the operation. Therefore, an effective MRV system must deliver reliable, publicly accessible and regularly updated data. It should define clear processes and transparent commitments for issuers, using trusted public databases such as those provided by the World Health Organisation (WHO) or the World Bank. This ensures investors and other stakeholders have accurate, verifiable information on the financial and structural characteristics of health SLBs and SLLs. In addition, since funding from an SLB/SLL is not explicitly earmarked for KPI achievement, it will be essential to ensure that these commitments are considered during the annual budget formulation process, allowing the MoH to implement essential activities on time and avoid potential penalties.

|

63chap5_p_63KPI policy area |

64chap5_p_64SDGs |

65chap5_p_65KPI |

66chap5_p_66Frequency: |

67chap5_p_67Data source: |

|

68chap5_p_68Communicable diseases |

69chap5_p_69SDGS 3.3: |

70chap5_p_70HIV Viral Suppression- People on HIV treatment who have suppressed viral loads 71chap5_p_71Ratio of: |

72chap5_p_72Annual |

73chap5_p_73https://indicatorregistry.unaids.org/ indicator/people-living-hiv-who-have-suppressed-viral-loads |

|

74chap5_p_74Health systems - vaccination |

75chap5_p_75SDG3:3.b Support the research and development of vaccines and medicines for the communicable and non‑communicable diseases that primarily affect developing countries, provide access to affordable essential medicines and vaccines, in accordance with the Doha Declaration on the Trade-Related Aspects Of Intellectual Property Rights Agreement and Public Health, which affirms the right of developing countries to use to the full the provisions in the Agreement on Trade-Related Aspects of Intellectual Property Rights regarding flexibilities to protect public health, and, in particular, provide access to medicines for all |

76chap5_p_76Proportion of the target population covered by all vaccines included in their national programme |

77chap5_p_77Annual |

78chap5_p_78https://unstats.un.org/sdgs/ metadata/files/Metadata-03-0b-01.pdf |

|

79chap5_p_79Maternal and child health and nutrition |

80chap5_p_80SDG 3.2 By 2030, end preventable deaths of newborns and children under 5 years of age, with all countries aiming to reduce neonatal mortality to at least as low as 12 per 1,000 live births and under‑5 mortality to at least as low as 25 per 1,000 live births |

81chap5_p_81Neonatal mortality rate |

82chap5_p_82Annual |

83chap5_p_83https://data.who.int/indicators/ i/E3CAF2B/A4C49D3 |

Impact Bonds

Description and Rationale

84chap5_p_84An impact bond is a contractual arrangement that funds a project between a government and/or donor, an investor and a service provider. The grant funder pays out only if, and only if, pre-agreed outcomes are achieved - the term “bond” is thus somewhat of a misnomer. The contracts commit the government/donor to make payments upon achievement of pre-agreed health outcomes, which the investor finances for the service providers to deliver. The donor may be a development partner or a private philanthropic organisation. Examples of impact bonds include improvements in weight gain for low-birth-weight or premature newborns, as well as a defined increase in the number of cataract surgeries and in visual acuity post-surgery.

85chap5_p_85An impact bond brings multiple parties together, each focusing on their specialisation:

- chap5_ul_9

- chap5_li_36Government and/or donor(s) who seek to maximise the benefits for target populations using scarce grant resources. They are defined as outcome funders because they pay based on the achievement of outcomes.

- chap5_li_37Socially-oriented investor(s) who seek both to have a positive social impact and a return on capital to reinvest in the future.

- chap5_li_38Service provider(s) such as a non-profit or social enterprise, which are incentivised to constantly adapt and innovate in their programmes to achieve the pre-agreed outcomes and for the maximum benefit of the populations they work with.

chap5_img_8

chap5_img_8

86chap5_p_86As impact bonds are typically less than USD 10 million, they are often best suited to piloting new ways of delivering health services and adding value when:

- chap5_ul_10

- chap5_li_39There is a demonstrated need for an outcome-focused approach in the specific target sector/geography.

- chap5_li_40There are promising interventions with some but incomplete evidence behind them, which could be refined through innovation and adaptation.

- chap5_li_41The chosen service providers lack access to adequate working capital or are unable to bear the risk of implementation.

87chap5_p_87Impact bonds in the health sector (follow to this link here for details) have been successfully used in Africa in:

- chap5_ul_11

- chap5_li_42Cameroon (neo-natal health; cataract surgery; hepatitis treatment)

- chap5_li_43Ethiopia (menstrual health and hygiene)

- chap5_li_44Kenya (adolescent sexual and reproductive health)

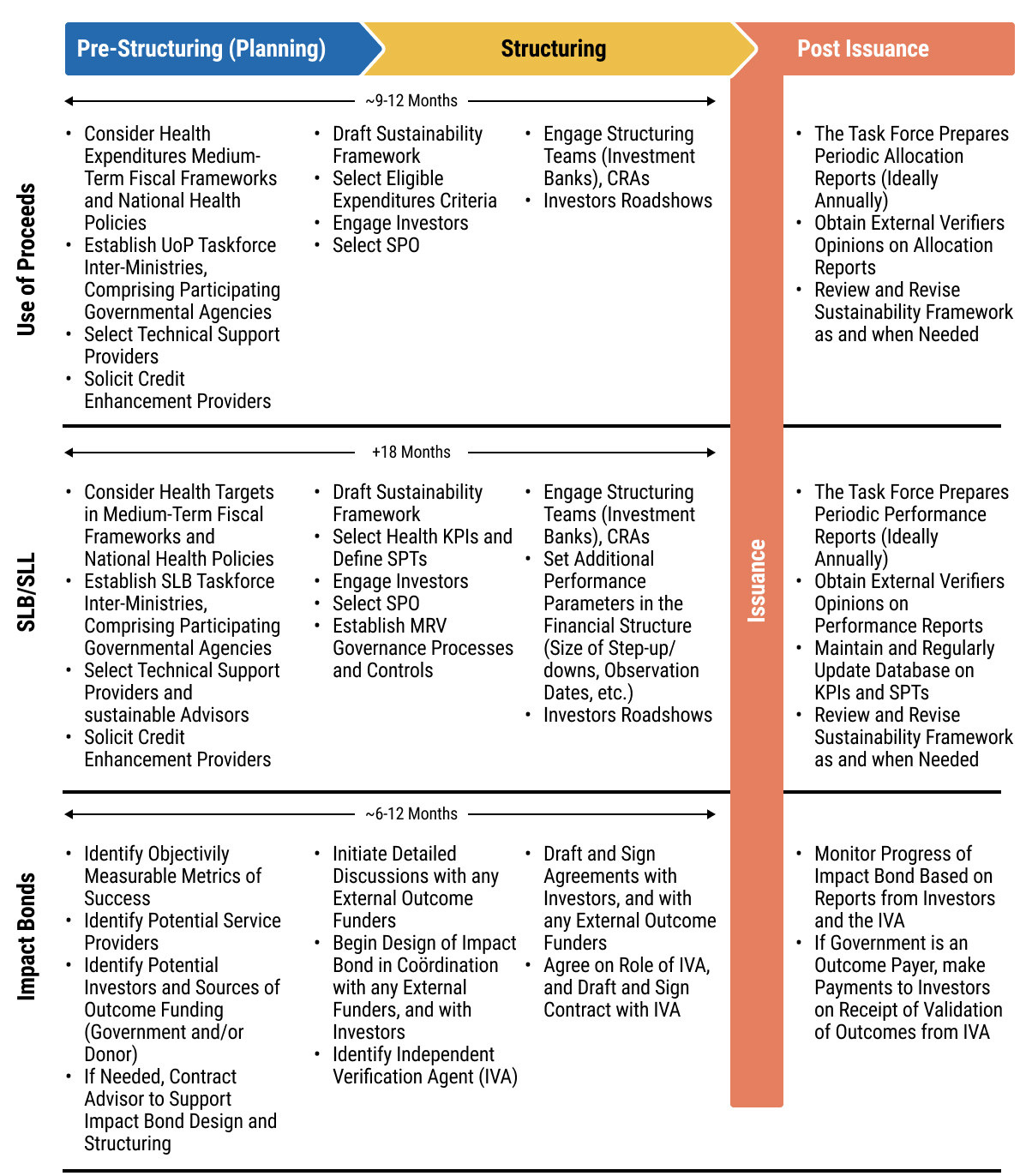

- chap5_li_45South Africa (vulnerable adolescent girls and young women)

- chap5_li_46Democratic Republic of Congo, Mali, Nigeria (physical rehabilitation)

Enabling conditions

88chap5_p_88Legal/regulatory. Impact bonds require that investors and the outcome funder establish a legal agreement (including, as needed, the establishment of a special-purpose vehicle (SPV), a temporary and ring-fenced legal entity set up for this specific purpose). Unlike the instruments described above, the government is not incurring any debt; instead, it is committing to make payments to investors upon achieving outcomes. Therefore, considerations regarding government debt issuance do not apply in this case.

89chap5_p_89Political buy-in. Ideally, outcome funding will either come from, or be channelled through, the government. This requires government buy-in notwithstanding that the government is not incurring any debt. Instead, an impact bond is beneficial to the government since it only makes outcome payments if the agreed, independently verified outcomes are achieved.

90chap5_p_90Data. Robust data at the project level are needed for the baseline against which outcomes are measured, to set ambitious yet reasonable targets, and for the outcomes themselves. This data needs to be verifiable by a third party, similar to an SLB/SLL.

Opportunities and Challenges

Opportunities

91chap5_p_91Impact bonds foster:

- chap5_ul_12

- chap5_li_47Accountability for results. Payments will not be made unless outcomes are achieved. This creates accountability for results throughout the programme.

- chap5_li_48Innovation. Service providers are only accountable for delivering outcomes, not a work plan, and can therefore adapt, innovate, and respond to evolving circumstances to achieve that. Up-front capital from the investor gives the financial space for this innovation.

- chap5_li_49Incentives to outperform. A well-designed impact bond typically features a graduated bonus for outperformance, capped at a certain level.

- chap5_li_50Cost-effectiveness. If the structuring is efficiently managed, impact bonds can improve cost-effectiveness by incentivising the maximisation of outcomes delivered per dollar.

Challenges

92chap5_p_92Impact bonds require:

- chap5_ul_13

- chap5_li_51Risk. An investor willing to take on the delivery risk (although in practice, this has often not been an obstacle given the volume of social capital available globally).

- chap5_li_52Metrics. Clear outcome metrics agreed by all parties.

- chap5_li_53Data. Availability of outcome data that can be independently verified at a reasonable cost and in a reasonable time.

- chap5_li_54Legal Structuring. A sometimes complex legal structure that may take time and legal fees to define and agree, especially for those participating in their first impact bond.

Implementation

93chap5_p_93The implementation of an impact bond is the responsibility of the investors, subject to the observance of the government’s and the outcome funder’s (if different) fiduciary, social and environmental standards. Government contractual involvement centres on a standard funding agreement with a donor (if any).

94chap5_p_94An impact bond may require an Independent Verification Agent (IVA), depending on the chosen verification approach. If outcomes can be verified using data that is already being collected, a third-party verification is not necessarily required. In particular, the following questions need to be addressed:

Questions That May Need to Be Answered During Structuring

|

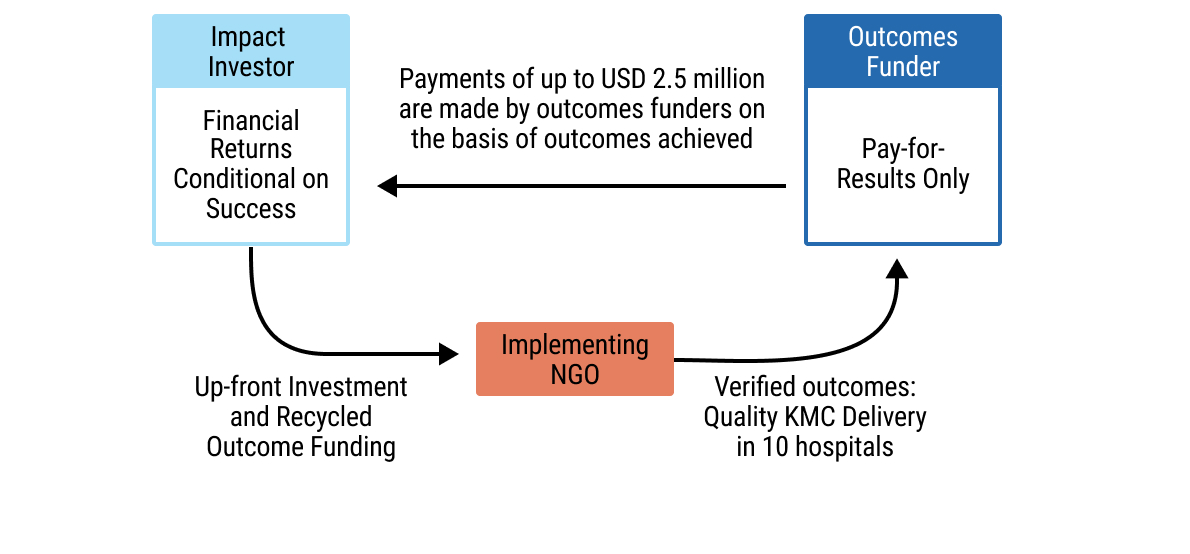

Case Study: Impact bond for Kangaroo Mother Care (KMC), Cameroon95chap5_p_95Description: Tackling neonatal mortality for premature and low-birth-weight infants

96chap5_p_96The approach has been demonstrated to reduce infant mortality and morbidity significantly in low-resource contexts. 97chap5_p_97Structure:  chap5_img_9 chap5_img_998chap5_p_98Objectives, Metrics and Results: The impact bond aimed to reduce mortality among premature and low-birth weight infants by scaling and improving KMC practice across Cameroon.

|

Key Legal Considerations

99chap5_p_99Understanding the legal documentation (as well as its relevant jargon) that underpins sustainable finance transactions is essential for effective transaction implementation and ensuring that terms are both fit for purpose and adequately reflect the local context.

100chap5_p_100A standard loan or bond refers to a debt instrument with conventional terms and conditions governing principal, interest, repayment and default, without any thematic or performance-linked provisions. The legal documentation for health and sustainability-linked instruments largely mirrors that of standard instruments, with modifications that align the financing with predefined performance objectives.

101chap5_p_101For health and sustainability-linked instruments, the transaction’s objectives (I.e. specifying health financing or performance-related objectives) are typically achieved through additional or revised provisions within otherwise standard documentation. As a result, these instruments are less complex to structure than debt swaps, which require multiple interlinked contracts and counterparties. Please refer to Chapter 5: Sustainable Finance Instruments> for the key legal considerations associated with debt swap transactions.

102chap5_p_102This section outlines the key clauses that are found in documentation for sustainable finance instruments. It also explains how debt documents can be enhanced to increase resiliency to potential health crises in countries through the use of debt pause clauses.

103chap5_p_103For details on the key provisions and negotiation points typically found in a standard sovereign loan agreement or bond offering document, please see the ALSF’s Loan Agreement and Bond Offering Document Commentaries.

Health Loans and Bonds: What is Unique About these Instruments?

104chap5_p_104Whether structured as a loan or a bond, a health-related financing instrument is distinguished from a standard instrument by the UoP being dedicated explicitly to health-related purposes. In the case of a health loan, the terms and conditions outlined in the loan (or “credit” or “facility”) agreement between the borrower and the lender(s) will expressly prescribe the health-related purpose of the borrowing, in line with the LMA’s Social Loan Principles (SLP) that the health investment be appropriately detailed in the documentation. Similarly, for a health bond issuance, the offering document (or prospectus) and the fiscal agency or trust deed will together outline the terms and conditions of the bonds, with a dedicated UoP specified, defining the relevant health project or programme and category of eligible expenditures set out in the agreed underlying Framework, in line with ICMA’s Social Bond Principles (SBPs). Notably, while the dedicated UoP is a defining characteristic of these instruments, failure to apply the funds in accordance with the stated health purpose does not typically constitute an event of default under the debt documentation. Instead, this is generally addressed through monitoring and reporting mechanisms.

Sustainability-Linked Instruments: What is Unique About These Instruments?

105chap5_p_105SLLs and SLBs share a common feature that distinguishes them from UoP instruments such as health loans or health bonds: the proceeds are not earmarked for specific projects or categories of expenditure. Instead, both instruments link their financial terms to the achievement of predefined SPTs measured against KPIs as described above.

106chap5_p_106In the case of an SLL, the loan agreement entered into between the sovereign and the lender(s) will include provisions that tie the interest margin to performance against the agreed SPTs, incorporating a step-up or step-down mechanism whereby the interest amounts owed increase if the SPTs are not met and decrease if they are met or exceeded. The loan documentation will also typically include a requirement for independent verification of performance, as a reporting obligation outlined in the transaction documentation, to confirm whether the relevant SPTs have been achieved for the applicable period.

107chap5_p_107The box below reflects the LMA’s draft provisions for SLLs.

Sample Step-Up/Step-Down Clause108chap5_p_108Sustainability Margin Adjustment 109chap5_p_109Subject to Clause · (Declassification Event) and the other paragraphs of this Clause, · following the receipt by the Agent of the Sustainability Compliance Certificate in respect of a SLL Reference Period in accordance with Clause · (Sustainability Compliance Certificate, Sustainability Report and Verification Report), the Margin applicable to each Loan shall be adjusted (a Sustainability Margin Adjustment) (or not adjusted, as the case may be) to the applicable rate determined using the table set out below and the number of SPTs that the Sustainability Compliance Certificate for that SLL Reference Period certifies have been met:

|

122chap5_p_122SLBs also link the bond’s financial characteristics (e.g. coupon rate or redemption premium) to the issuer’s achievement of specified SPTs, consistent with ICMA’s Sustainability-Linked Bond Principles. This will also be outlined in the bond’s documentation, like that of the SLLs.

Impact Bonds: What is Unique About These Instruments?

123chap5_p_123Impact bonds represent a distinct contractual structure from those described above. Rather than adapting a standard debt instrument, they comprise a series of contracts among governments, donors, investors and service providers, under which repayment is contingent upon the achievement of predefined social or health outcomes.

124chap5_p_124An impact bond requires the following contracts:

- chap5_ul_17

- chap5_li_67Outcomes contract, between government/other outcomes funders and investors to define the amounts to be paid against achievement of each unit of outcome (or the whole outcome if it is not divisible). A clause may be necessary to permit some payment to investors in the event of force majeure events that prevent the desired outcomes from being achieved. In some cases, the service provider may also be involved in the contracting structure, but this is unusual.

- chap5_li_68Investors and Service Providers to define programme implementation, disbursement triggers and possible bonus to service providers on achievement or over-achievement of outcomes. Experience suggests that investors will want to maintain a significant degree of flexibility in the contract to allow for learning and adaptation (feedback loops).

- chap5_li_69Government/other Outcome Funders and the IVA to define the role of, and payments, to the IVA (in some cases, an IVA may not be needed if all parties agree it is not necessary).

Pandemic or Epidemic Pause Clauses

125chap5_p_125Loan and bond documentation can also be drafted to include clauses that allow the borrower or issuer to pause repayments in the case of an exogenous health event, such as a pandemic or epidemic. These are typically structured as contingent debt service deferral clauses, which provide for a temporary standstill on principal and/or interest payments upon the occurrence of a predefined trigger event such as a declaration of a public health emergency by a recognised international body (e.g. the WHO) or a national authority. The clause typically specifies the duration of the deferral period, the conditions for resuming payments and the treatment of accrued interest during the deferral. Because they provide certainty and predictability for all parties to the debt contract, these should be beneficial for both the sovereign and its creditors.

126chap5_p_126ICMA has published a sample pandemic-related pause clause, which would tie the repayment pause to a WHO declaration of a Public Health Emergency of International Concern. This formulation provides an objective trigger linked to an authoritative international body, reducing ambiguity around when the deferral trigger can be invoked.

127chap5_p_127The following is the sample pandemic event pause clause published by ICMA. The language below can be adapted as appropriate for epidemics or other health crises that may impact a country.

Sample Pandemic Event-Related Debt Clause128chap5_p_128"Deferral Event" means the occurrence of any of the following: 129chap5_p_129(a) Pandemic Event, 130chap5_p_130(b) Other. 131chap5_p_131"Pandemic Event" means the occurrence of the following sequence of events after the Issue Date: 132chap5_p_132(a) The WHO declares a Public Health Emergency of International Concern (as defined in the International Health Regulations of the WHO) with respect to any disease that grants such disease phase 6 status, or any other categorisation as the WHO may use to describe an active ongoing pandemic from time to time (PHIO) (excluding the continuation of the COVID-19 pandemic in the form of the current variants of COVID-19 existing as of the Issue Date); 133chap5_p_133(b) The [Sovereign] or any other competent political or regulatory subdivision thereof declares a state of public health emergency with respect to any PHIO declared under (a) above; 134chap5_p_134(c) And either: 135chap5_p_135(i) The occurrence of a Real Gross Domestic Product (GDP) contraction over [two consecutive quarters], which in aggregate results in a contraction of at least [•]% of Real GDP relative to [the same two quarters in the previous fiscal year (based on estimated realised GDP at constant prices for the current year and provisional realised GDP at constant prices for the prior year], as published by [•] and reported to at least [two] of: the International Monetary Fund (IMF), the World Bank and [insert any appropriate regional MDB]); and/or 136chap5_p_136(ii) The events described in paragraphs (a) and (b) above result in the [Sovereign] approving and enacting an increase in governmental spending (that is not rescindable) (the Pandemic Increased Spending) directly relating to the relevant PHIO (and the measures taken by the [Sovereign] in response thereto) that is at least equal to USD [•]. 137chap5_p_137For the purposes of paragraph (c)(ii) above, any reduction in budgeted government spending as a result of payments due under these [terms and conditions/Conditions] being deferred as a result of a Pandemic Event occurring shall be disregarded when determining whether Pandemic Increased Spending has been approved and enacted. 138chap5_p_138"Real GDP" means the gross domestic product of [Sovereign] at constant prices as adjusted for inflation. 139chap5_p_139For the full text, please see CRDC's November (2022) notice. |

140chap5_p_140At the time of writing this User Guide, the first country known to integrate a pandemic clause into its sovereign debt documentation is Barbados, which included a trigger tied to a pandemic emergency in its debt swap in 2022 and subsequently, including in its June 2025 sovereign bonds.

Case Study: Government of Barbados - Pandemic Clause (2022)141chap5_p_141In September 2022, the Government of Barbados completed a debt conversion (refer to Chapter 5: Sustainable Finance Instruments for an overview) for marine conservation that featured the world’s first pandemic clause. This provision, added alongside a natural disaster clause, allows the Government of Barbados to defer up to two years of principal payments (approximately USD 18 million) in the event of a qualified pandemic or natural disaster. This feature was designed to make the country’s debt terms more resilient to external shocks. 142chap5_p_142This transaction was financed by Credit Suisse and the Canadian Imperial Bank of Commerce, with The Nature Conservancy as co-guarantor and conservation advisor and the Inter-American Development Bank (IDB) as co-guarantor. It helped Barbados refinance USD 150 million of its existing debt, generating an estimated USD 50 million in savings over 15 years. These funds are dedicated to marine conservation and support Barbados’s commitment to protect up to 30% of its ocean territory. 143chap5_p_143Barbados also included these clauses in its USD 500 million eurobond, marking its return to international capital markets in July 2025. 144chap5_p_144References: 145chap5_p_145https://www.insurancejournal.com/news/international/2022/09/22/686174.htm 146chap5_p_146https://www.nature.org/content/dam/tnc/nature/en/documents/TNC-Barbados-Debt-Conversion-Case-Study.pdf 147chap5_p_147https://nationnews-brb.newsmemory.com/?publink=29e7314b6_134fa25 |

148chap5_p_148Nonetheless, pandemic deferral clauses and wider debt pause clauses are gaining traction. Indeed, bilateral official lenders, MDBs, governments and investors are increasingly recognising the value of such pause or deferral mechanisms in the face of exogenous shocks that can impact countries’ liquidity and debt sustainability. These clauses should be considered as another tool in the toolbox.

The Importance of Legal and Financial Advisors

149chap5_p_149For government officials designing and negotiating health or sustainability-linked debt instruments, it is critical not to go it alone. The technical and legal complexity of these structures necessitates specialised advice. Integrating experienced legal and financial advisors into the transaction team ensures that the documentation is aligned with best practices, international standards and domestic law, and that pricing and risk allocation are appropriately calibrated. Governments should also involve their Attorney-General’s Office (or equivalent) from the outset of the transaction to ensure that any transaction is consistent with national laws and regulations, and required approvals and legal opinions can be provided. (See also above on legal and regulatory frameworks).

150chap5_p_150The ALSF is an international organisation dedicated to providing legal advice and technical assistance to African countries in the structuring and negotiation of complex commercial transactions, including those outlined in this User Guide.

151chap5_p_151For more information on how the ALSF can support you, please visit https://www.alsf.int/

Summary of Instrument Implementation Processes and Stakeholders

152chap5_p_152The three instruments outlined in this chapter each have their own specific requirements for designing, structuring and implementation, with particular input needed from each key stakeholder. There is also a difference in the expected timeframe before issuance, ranging from 6 to 12 months for an impact bond to over 18 months for an SLB/SLL.

153chap5_p_153Figure 5.5 below summarises these key activities by instrument.

154chap5_p_154Table 5.3 following outlines the specific key role of each stakeholder.

chap5_img_10

chap5_img_10

|

155chap5_p_155Stakeholder / Institution |

156chap5_p_156Core Role in UoP Bond/Loan or SLL/SLB |

157chap5_p_157Interest / Incentive |

158chap5_p_158Potential Concern / Risk |

159chap5_p_159Engagement Strategy / Framing |

160chap5_p_160Phase of Involvement |

|

161chap5_p_161Minister of Health 162chap5_p_162 163chap5_p_163Included here could be the Deputy Ministers of Health/Ministers of State for Health |

164chap5_p_164* Health bond/loan: Defines eligible health projects and investment areas. 165chap5_p_165* SLB/SLL: Identifies relevant KPIs, helps set ambitious SPTs, and develops/manages the MRV framework. 166chap5_p_166*SLB/SLL: responsible for advocating for funding needed to achieve SPT during the annual budgeting process, and ensuring strong, evidence-based implementation of the relevant activities for the selected KPI 167chap5_p_167* Both: Provides technical health input for the issuance framework. |

168chap5_p_168* Health bond/loan: Secures ring-fenced funding for specific, planned health programmes. 169chap5_p_169* SLB/SLL: Drives and demonstrates national health improvements; incentivised to meet SPTs to avoid financial penalties and gain reputational benefits. |

170chap5_p_170* Health bond/loan: Risk of funds being diverted or misallocated from intended projects. 171chap5_p_171* SLB/SLL: Risk of failing to meet SPTs, triggering financial penalties (e.g. coupon step-up) and reputational damage. |

172chap5_p_172Frame as a fiscal innovation to achieve core health mandates. 173chap5_p_173Align with the national health strategy, development plan, and debt management strategy. |

174chap5_p_174Early concept through final reporting (entire lifecycle). |

|

175chap5_p_175Minister of Finance 176chap5_p_176 177chap5_p_177Also captured here could be the Chief Economic Advisor, the Financial Secretary (Permanent Secretary for the MoF) |

178chap5_p_178Both: Custodian of sovereign debt and lead coordinator of the sustainability framework across government. 179chap5_p_179*SLB/SLL: The Budget department must ensure the KPI-related activities are budgeted and monitored during the budget cycle. |

180chap5_p_180* Health bond/loan: Secures funding for specific national priorities. 181chap5_p_181* SLB/SLL: Raises general-purpose funds while demonstrating commitment to national goals. 182chap5_p_182* Both: Diversifies the investor base; signals market leadership. |

183chap5_p_183* Dependency: Heavy reliance on other ministries (e.g. Health) for data and performance to meet reporting obligations or SPTs. 184chap5_p_184* Financial: Risk of financial penalties (step-ups) if SPTs are missed. 185chap5_p_185* Admin: High administrative burden for UoP tracking or SLB/SLL verification. |

186chap5_p_186Frame as a co-created fiscal innovation, aligning with the national debt management strategy and development plan. 187chap5_p_187Emphasise market access and investor diversification. |

188chap5_p_188Early concept through final maturity (entire lifecycle). |

|

189chap5_p_189Stakeholder / Institution |

190chap5_p_190Core Role in UoP Bond/Loan or SLL/SLB |

191chap5_p_191Interest / Incentive |

192chap5_p_192Potential Concern / Risk |

193chap5_p_193Engagement Strategy / Framing |

194chap5_p_194Phase of Involvement |

|

195chap5_p_195Presidency 196chap5_p_196 197chap5_p_197Actors here could include the Chief Minister, Minister of State, etc. |

198chap5_p_198Provides high-level political leadership, ensures cross-ministerial alignment, and sets strategic direction. |

199chap5_p_199Enhances national prestige as an innovator. 200chap5_p_200Builds credibility with international partners. 201chap5_p_201Secures a political legacy and drives national ownership of reforms. |

202chap5_p_202Competing political priorities or timelines. 203chap5_p_203Risk of reform fatigue or political opposition. 204chap5_p_204Concern over the complexity of the commitments. |

205chap5_p_205Frame as a high-visibility, legacy-defining reform. 206chap5_p_206Link to the national development agenda and international commitments (e.g. SDGs). |

207chap5_p_207Beginning (to provide mandate) and at key inflection points (to resolve bottlenecks). |

|

208chap5_p_208Parliament 209chap5_p_209Actors here could include the chairs for the parliamentary committee on health, finance, etc. |

210chap5_p_210Approves national debt operations. 211chap5_p_211Ensures accountability for public expenditure and performance commitments. |

212chap5_p_212Ensures transparency, fiscal prudence and public accountability 213chap5_p_213Gains political capital by championing innovative and effective solutions for citizens. |

214chap5_p_214Concern that the instrument is too complex or bypasses traditional oversight functions. 215chap5_p_215Political opposition or lack of cross-party support. |

216chap5_p_216Engage early with clear, non-technical briefings. 217chap5_p_217Demonstrate fiscal discipline and tangible benefits for citizens. 218chap5_p_218Identify and empower cross-party champions. |

219chap5_p_219Early consultation (pre-approval) and at key reporting/inflection points. |