Search in the book

Crédits photographiques

intercalaire 1 pour la démo

Table des matières

Cat. 1

cat1_h4_0Historique

Ce tableau fut commencé vers 1503 au moins, sans doute pour Francesco del Giocondo, gentilhomme florentin (1460-1539), mais fut conservé par Léonard de Vinci jusqu’à la fin de sa vie pour en pursuivre l’exécution picturale toujours inachevée à sa mort ; il fut très probablement acquis par François Ier en 1518[1].

cat1_h4_1Bibliographie

Brejon de Lavergnée et Thiébaut, 1981, p. 192, ill. ; Habert et Scailliérez, 2007, p. 61-122, p. 81, ill. n&b ; Delieuvin et Franck, 2019, p. 224-233.

1cat1_p_1Si l’on nous demande pourquoi figure, dans cet ouvrage consacré au Louvre, un tableau qui ne s’y trouve plus, nous répondrons que la disparition même de l’admirable Joconde nous la rend encore plus chère et nous fait désirer davantage de la pouvoir contempler, ne fût-ce qu’en effigie.

2cat1_p_2On n’a pas oublié l’émotion qui secoua l’univers civilisé lorsque se répandit l’incroyable nouvelle : « La Joconde a été volée. » Sur tous les points du globe, cette perte fut ressentie comme un désastre. Désastre, certes, et sans équivalent, car, avec la Joconde, a disparu l’une des plus grandioses productions du génie humain. Malgré son prodigieux assemblage de chefs-d’œuvre, le Salon Carré a perdu le meilleur de sa gloire ; dans l’écrin rempli de joyaux manque le plus beau diamant, celui qui jetait les feux les plus brillants et les plus purs. La Mona Lisa n’accueille plus le visiteur de son sourire énigmatique et qui sait en quels lieux l’étrange créature repose aujourd’hui son troublant et mystérieux regard ? Et, malgré tout, survit en nous l’indéfectible espérance de la revoir un jour à son ancienne place, triomphante et narquoise, et groupant une cour encore plus nombreuse d’adorateurs autour de son immortelle beauté.

3cat1_p_3Nulle peinture au monde n’a provoqué une aussi entière admiration. La Joconde a eu ses poètes, ses romanciers, ses amants. Certains hommes l’ont adorée comme un être vivant ; il en est même qui se sont tués pour elle et peut-être faut-il chercher dans une passion de cet ordre l’énigme de son étrange disparition.

4cat1_p_4Relisons la page enthousiaste où Théophile Gautier célèbre la Mona Lisa[2] :

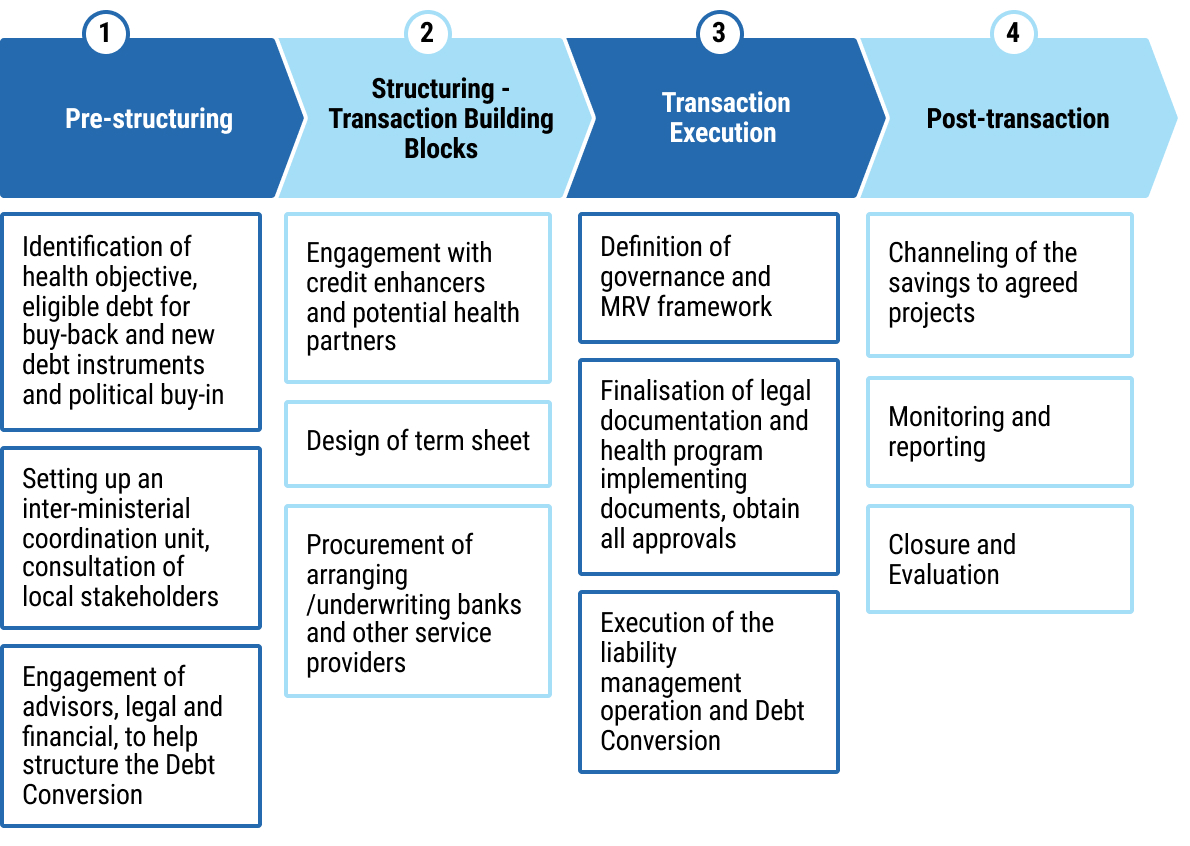

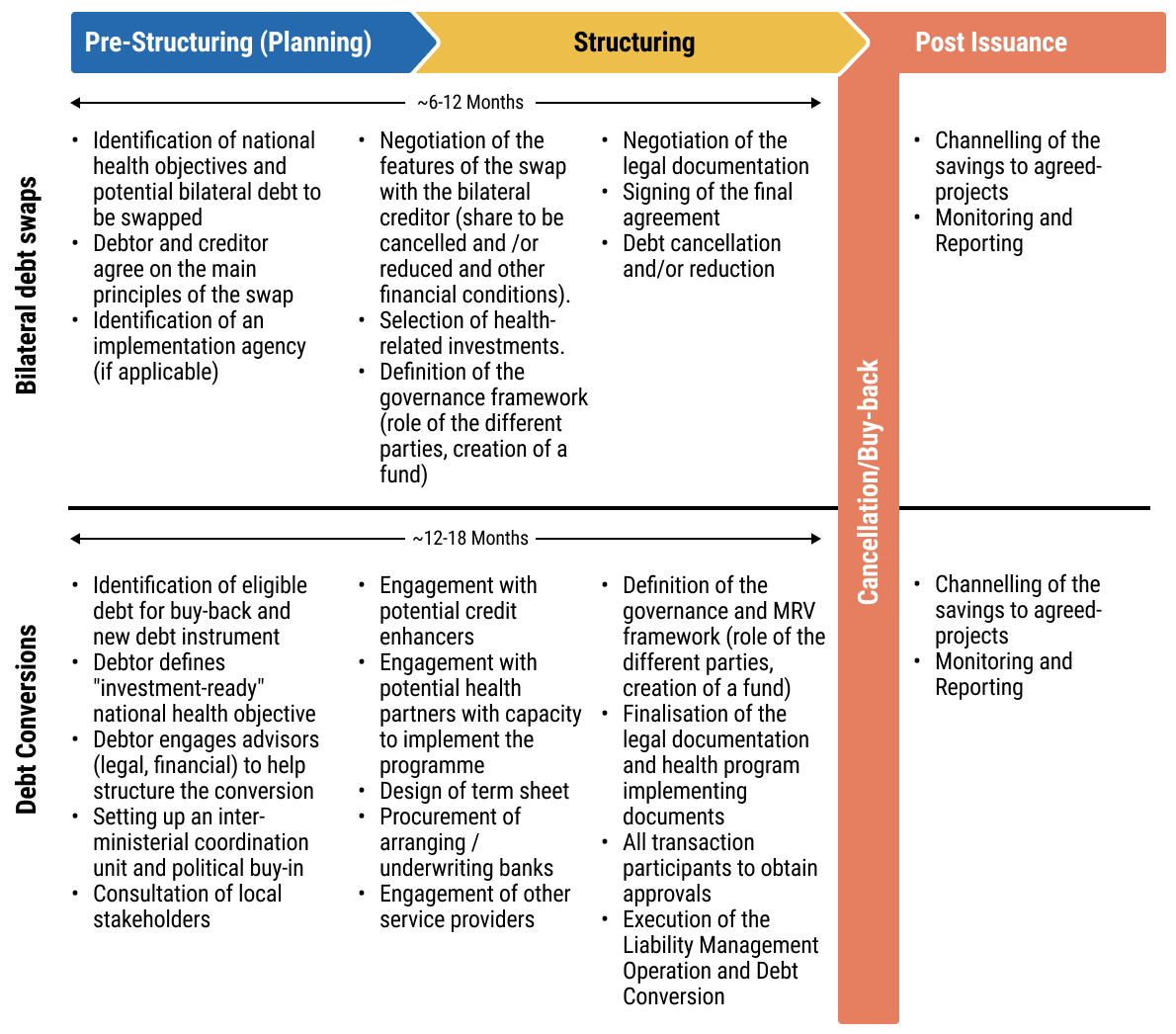

5cat1_p_5« La Joconde ! Sphinx de beauté qui souris si mystérieusement dans le cadre de Léonard de Vinci et sembles proposer à l’admiration des siècles une énigme qu’ils n’ont pas encore résolue, un attrait invincible ramène toujours vers toi ! Oh ! en effet, qui n’est resté accoudé de longues heures devant cette tête baignée de demi-teintes crépusculaires, enveloppée de crêpes transparents et dont les traits, mélodieusement noyés dans une vapeur violette, apparaissent comme une création du Rêve à travers la gaze noire du Sommeil ! De quelle planète est tombé, au milieu d’un paysage d’azur, cet être étrange avec son regard qui promet des voluptés inconnues et son expression divinement ironique ? Léonard de Vinci imprime à ses figures un tel cachet de supériorité qu’on se sent troublé en leur présence. Les pénombres de leurs yeux profonds cachent des secrets interdits aux profanes et les inflexions de leurs lèvres moqueuses conviennent à des dieux qui savent tout et méprisent doucement les vulgarités humaines.

6cat1_p_6Quelle fixité inquiétante et quel sardonisme surhumain dans ces prunelles sombres, dans ces lèvres onduleuses comme l’arc de l’Amour après qu’il a décoché le trait ! Ne dirait-on pas que la Joconde est l’Isis d’une religion cryptique qui, se croyant seule, entr’ouvre les plis de son voile, dût l’imprudent qui la surprendrait devenir fou et mourir ? Jamais l’idéal féminin n’a revêtu de formes plus inéluctablement séduisantes. Croyez que si don Juan avait rencontré la Mona Lisa, il se serait épargné d’écrire sur sa liste trois mille noms de femmes ; il n’en aurait tracé qu’un, et les ailes de son désir eussent refusé de le porter plus loin. Elles se seraient fondues et déplumées au soleil noir de ces prunelles. Nous l’avons revue bien des fois, cette adorable Joconde, et notre déclaration d’amour ne nous paraît pas aujourd’hui trop brûlante. Elle est toujours là, souriant avec une moqueuse volupté à ses innombrables amants. Sur son front repose cette sérénité d’une femme sûre d’être éternellement belle et qui se sent supérieure à l’idéal de tous les poètes et de tous les artistes. »

7cat1_p_7Le divin Léonard mit quatre ans à faire ce portrait, qu’il ne pouvait se décider à quitter et qu’il ne considéra jamais comme fini ; pendant les séances, des musiciens jouaient pour égayer le beau modèle et empêcher ses traits charmants de prendre un air d’ennui et de fatigue.

8cat1_p_8Doit-on regretter que le noir particulier qu’employait Léonard ait prévalu dans les teintes de la Mona Lisa et leur ait donné cette délicieuse harmonie violâtre, cette tonalité abstraite qui est comme le coloris de l’idéal ? Nous ne le pensons pas. Maintenant, le mystère s’ajoute au charme et le tableau, dans sa fraîcheur, était peut-être moins séduisant.

9cat1_p_9Le modèle de ce magnifique portrait s’appelait Lisa Maria di Noldo Gherardini ; elle épousa, en 1495, Francesco di Bartolomeo de Zenobi del Giocondo, d’où son nom de « Joconde », sous lequel elle est aujourd’hui célèbre (Fig. 1-1).

10cat1_p_10La Joconde fut peinte vers 1500. François Ier l’acquit pour quatre mille écus d’or et la fit placer dans le cabinet doré de Fontainebleau. Elle passa ensuite dans la chambre de Louis XIV, à Versailles. Après la Révolution, le célèbre portrait fut transporté au Louvre et placé dans le Salon Carré, d’où il disparut en août 1911.

11cat1_p_11Hauteur : 0.77. – Largeur : 0.53. – Figure en buste grandeur nature.

Voir sur le site des collections du musée du Louvre https://collections.louvre.fr/ark:/53355/cl010062370 : « Données historiques ».

Gautier, 1882, chapitre « Salon Carré », p. 26. Consulter l’ouvrage sur la bibliothèque numérique de l’Institut national d’histoire de l’art : https://bibliotheque-numerique.inha.fr/collection/item/8352-guide-de-lamateur-au-muse-du-louvre.

Cat. 2

cat2_h4_0Historique

Commandé par Charles Ier d’Angleterre (?) pour remplacer un portrait de la reine Anne, par Paul Van Somer (1617), au château d’Oatlands (?)[1] ; la dispersion des collections royales britanniques, puis leur histoire au long du xviie siècle, font perdre la trace du tableau[2] ; […] ; 13 juillet 1797 : le tableau est inventorié par les commissaires révolutionnaires, à Versailles, dans la chambre de la reine ; 15 juillet 1797 : envoyé au Muséum central des arts (dans un lot expédié en échange du « cloître des Chartreux et [d]es ports de Vernet[3] ») ; 5 août 1797 : récépissé de l’arrivée des œuvres donné à Fragonard « chargé par le Ministre de l’intérieur de surveiller les transports[4]14 » ; 1816 : les experts du musée l’estiment 100 000 francs[5] ; 17 juillet 1945 : retour du château de Montal après évacuation pendant la Seconde Guerre mondiale[6].

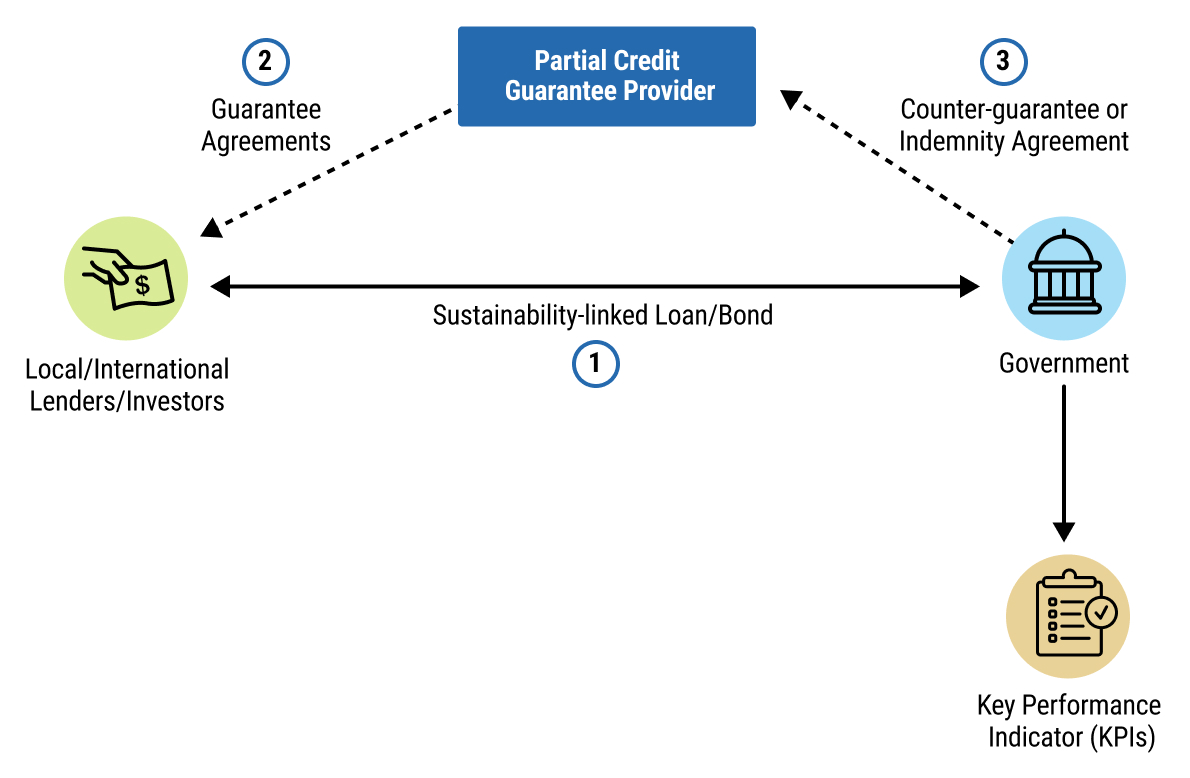

cat2_h4_1Bibliographie

Dezallier d’Argenville, 1752, p. 415 ; Rumberg et Shawe-Taylor, 2018, no 76, p. 7, 22, 131, 244, et note 41, p. 257 ; Ayres, 2020, paragraphe 16 et fig. 11 ; White, 2021, p. 222-224 et fig. 203 ; Eaker, 2022, p. 109 et fig. 52 p. 111 ; Ducos, 2023, no 18 (https://livres.louvre.fr/vandyck/cats/18/).

1cat2_p_1LE portrait de Charles Ier d’Angleterre, que possède le Louvre, est un chef-d’œuvre légendaire.

2cat2_p_2Le poing sur la hanche, du côté de l’épée, la main droite appuyée sur une haute canne, le roi tourne légèrement sa tête fine et blonde, encadrée d’un grand chapeau. Il regarde avec calme, avec assurance, et toute son attitude est celle d’un homme habitué à commander. Sa veste de soie grise est traversée du baudrier qui soutient l’épée. Au-dessous de la culotte rouge et laissant voir les bas de soie, des bottes souples en cuir fauve, garnies d’éperons, emprisonnent une jambe nerveuse et élégante. Un peu en arrière, le cheval favori du roi piaffe, impatient, maintenu par un écuyer vêtu de rouge qui représente le chevalier d’Hamilton ; un autre serviteur, plus loin, porte le manteau du souverain. Le tertre où sont placés les personnages est ombragé par la ramure épaisse d’un arbre et, sur les plans éloignés, s’étend une plaine au-dessus de laquelle des nuages gris floconnent dans le ciel bleu.

3cat2_p_3Ce tableau, d’une admirable composition, rend à merveille l’élégante silhouette de Charles Ier, le plus beau des Stuarts (Fig. 2-1). L’œuvre se présente avec une noblesse contenue, une richesse sourde et éclatante tout à la fois, une somptuosité discrète qui impressionnent, où l’on retrouve quelque chose de la manière de Rubens, mais tempérée, assagie, comme disciplinée.

4cat2_p_4Van Dyck avait d’ailleurs longtemps travaillé avec Rubens, qui l’appelait « le meilleur de ses élèves ». Son amitié lui fut aussi profitable que ses leçons. C’est lui qui le recommanda à la cour des Stuarts. Charles Ier, influencé par les éloges de Rubens pour son élève et ravi du portrait de Nicolas Lanière, son maître de chapelle, peint par Van Dyck, invita celui-ci à se rendre auprès de lui.

5cat2_p_5Van Dyck arriva à Londres et se présenta au roi qu’il conquit dès la première entrevue. Il avait une beauté fine, assez semblable à celle de Charles Ier, des manières aisées, une certaine grâce cavalière et l’air vif et dégagé d’un homme du monde accompli. Sa conversation n’était pas moins agréable que sa personne ; il avait la parole abondante et brillante, alimentée par un savoir profond et disciplinée par un tact infini. Le roi se plaisait beaucoup en sa compagnie ; il se rendait fréquemment à son atelier et, dépouillant avec lui toute contrainte d’étiquette, ils s’entretenaient ensemble de mille sujets pendant que Van Dyck travaillait à son portrait. De cette époque datent les nombreuses effigies du roi et de la reine.

6cat2_p_6En récompense de son talent, Van Dyck reçut le titre de principal peintre ordinaire de Leurs Majestés, fut créé chevalier et eut son logement à Blackfriars.

7cat2_p_7Dans son portrait de Charles Ier, Van Dyck s’était révélé portraitiste de génie et il n’est pas étonnant que, voulant suivre l’exemple du souverain, toute la noblesse enviât l’honneur de poser devant le grand artiste flamand. Bientôt, il ne put suffire aux commandes, il dut prendre des collaborateurs chargés de peindre les accessoires, se réservant seulement les têtes et les mains. Le succès venu, il eut toute liberté d’augmenter ses prix et gagna des sommes considérables qu’il dépensait largement. Sa maison était montée sur un pied magnifique, il possédait un équipage nombreux et élégant et offrait si bonne chère que peu de princes étaient aussi visités et aussi bien servis que lui.

8cat2_p_8En 1639, il épousa Mary Ruthven, demoiselle d’honneur de la reine, petite-fille de lord Ruthven, dont il eut une fille. Sa femme ne lui apportait pas de dot, mais elle était considérée comme une des plus merveilleuses beautés de son temps. Cette union fut de courte durée. Sa vie de travail et de plaisirs avait miné la santé de Van Dyck et malgré que Charles Ier eût promis trois cents livres au médecin s’il le sauvait, le grand peintre mourut à Blackfriars, le 9 décembre 1641, âgé seulement de quarante-deux ans.

9cat2_p_9« Non moins coloriste que Rubens, écrit Théophile Gautier, mais plus fin, plus élégant que son maître, Van Dyck semble créé pour peindre les rois, les princes, les duchesses, tout ce monde de la haute vie, fin de race, aristocratique d’allure, d’une magnificence héréditaire et marchant au-dessus de la multitude comme les dieux marchent sur les nuages. Il a peint d’une touche aisée et noble, avec une couleur brillante mais vigoureuse et une pénétration rapide du caractère, des têtes qu’on ne reverra plus, des masques dont le moule est brisé, des expressions d’existences à jamais évanouies.[7] »

10cat2_p_10Le portrait de Charles Ier entra dans le domaine national d’assez curieuse façon. À la vente du comte de Thiers, qui en était possesseur, la comtesse Du Barry l’acheta pour une somme de 24.000 livres. Et comme on lui demandait pourquoi elle avait choisi ce tableau de préférence aux autres de la collection qui semblaient devoir mieux lui convenir, elle répondit que c’était un portrait de famille, car elle prétendait tenir de la maison des Stuarts. Plus tard, elle le céda au même prix à M. d’Angivillers, pour le compte du Roi.

11cat2_p_11Ce tableau occupe aujourd’hui au Louvre la salle Van Dyck qui précède la nouvelle salle des Rubens.

12cat2_p_12Hauteur : 2.72. – Largeur : 2.12. – Figures en pied grandeur naturelle.

Rumberg et Shawe-Taylor, 2018, p. 22 : il s’agit là d’une hypothèse formulée par Per Rumberg et Desmond Shawe-Taylor, mais sur laquelle revient celui-ci (ibid., p. 131) et celui-là (ibid., no 76, p. 244). Voir aussi Millar, 1982, p. 21, pour le précédent, thématique, d’Henriette Marie partant pour la chasse. Ayres, 2020, paragraphe 16, s’appuyant sur Liedtke, 1989, p. 256-257, reprend l’idée suivant laquelle le tableau du Louvre serait le pendant du Portrait d’Anne de Danemark par Paul Van Somer (collection de S. M. la reine Élisabeth II, RCIN 405887). Les œuvres, en effet, sont de dimensions proches et le fils répondrait ainsi à la mère. Cette remarque a l’intérêt de rappeler l’importance possible de la figure maternelle dans les choix de Charles Ier. La difficulté, que ne souligne pas Sara Ayres, est évidemment que le Van Dyck relègue au rang d’image archaïque et dépassée le Van Somer, en cela parfaitement en accord avec la « procédure vandyckienne » habituelle de relégation à une classe inférieure des créations de différents artistes nordiques l’ayant précédé. Le cas de Daniel Mytens est le plus connu ; on peut aussi penser à l’esthétique de Michiel Van Mierevelt à La Haye. Que le Van Somer et le Van Dyck soient de dimensions très proches signifie peut-être simplement que Van Dyck, s’inscrivant dans une tradition, souhaitait susciter la comparaison, en sa faveur, avec l’œuvre, somme toute assez gauche, de son prédécesseur à la cour Stuart.

On reconnaît la Vie de saint Bruno, par Eustache Le Sueur, et la série des ports de France, par Joseph Vernet.

Cantarel-Besson, 1992, p. 124. Jean Honoré Fragonard, membre du conservatoire des Arts depuis janvier 1794 (grâce à l’intervention de Jacques Louis David) et chargé de l’administration du Muséum, se voit confier durant l’été 1797 le déménagement des œuvres (comme la mise en place du musée de l’École française à Versailles). Voir Martial Guédron, « Fragonard, Jean Honoré », Allgemeines Künstlerlexikon (2019), https://www-degruyter-com.bnf.idm.oclc.org/database/AKL/entry/_00069426/html, consulté le 30 mai 2020.

Voir Ducos, 2023, cat. 18, https://livres.louvre.fr/vandyck/cats/18, « Historique ».

Gautier, 1882, chapitre « Écoles allemande, flamande et hollandaises », p. 159. Consulter l’ouvrage sur la bibliothèque numérique de l’Institut national d’histoire de l’art : https://bibliotheque-numerique.inha.fr/collection/item/8352-guide-de-lamateur-au-muse-du-louvre.

Cat. 3

cat3_h4_0Historique

Vente « d’une riche collection d’articles curieux de tout genre » [Lespinasse d’Arlet], Paris, maison des divisions supplémentaires du Mont-de-Piété, 45 rue Vivienne, 11 juillet1803, organisée par Paillet et Delaroche, lot 335 : « Un très beau Tableau peint au pastel, par le célèbre Latour. Il représente Madame de Pompadour, de grandeur naturelle, en pied et assise, tenant un Livre de musique, et près d’un bureau où sont posés des Livres et autres accessoires. Ce morceau, le plus grand Ouvrage de cet Artiste, est recouvert par une belle Glace blanche faite exprès à Saint Gobain, et a appartenu à feu Louis XV. » Le portrait est à cette occasion acquis par Alexandre Joseph Paillet (1743-1814), l’un des deux organisateurs de la vente, pour la somme de 500 francs, et aussitôt revendu au Musée central des Arts[1].

cat3_h4_1Bibliographie

Salmon, 2018, cat. 90, p. 182-191 ; Ribeiro, 2020, p. 174-177, fig. 2 p. 175, note 4 p. 177.

1cat3_p_1Quentin La Tour fut un admirable pastelliste et un grand magicien de la couleur, la nature l’avait moins heureusement doté sous le rapport du caractère. Il était habituellement quinteux et fantasque. Très avancé dans les doctrines des Encyclopédistes, il affectait avec les grands une désinvolture frisant l’impertinence. On le voit reprocher au Dauphin que ses enfants sont fort mal élevés et qu’il se laisse duper par des fripons. Le roi lui-même doit subir ses boutades : pendant une séance de pose (Fig. 3-1), il fatigue Louis XV par un éloge outré des étrangers :

2cat3_p_2– Mais je vous croyais Français, lui dit le roi surpris. – Non, sire, répond hargneusement La Tour, je suis Picard, de Saint-Quentin.

3cat3_p_3L’exécution du portrait de Mme de Pompadour, notamment, est marquée de péripéties et d’incidents sans nombre. Quentin La Tour n’aime pas la favorite. De premières ouvertures lui sont faites en 1750, il les repousse ; prié de se rendre à Versailles auprès de la marquise, il se contente de répondre à l’envoyé :

4cat3_p_4– Dites à Madame que je ne vais pas peindre en ville.

5cat3_p_5Mme de Pompadour, dépitée, en écrit à son frère, le marquis de Marigny, qui est lié avec l’artiste. Son intervention amène un rapprochement et La Tour jette sur le papier deux préparations de son tableau. Puis il reste deux ans sans y travailler ; tous les prétextes lui sont valables pour se dérober. A Marigny qui le presse il écrit qu’il se sent en proie « à un abattement, à un anéantissement qui lui font craindre la fièvre », et il veut essayer « si l’air lui fera du bien ». Marigny se fâche alors, mais sans plus de résultat. Mme de Pompadour, qui tient à son portrait, essaye de la douceur : « Je suis, lui mande-t-elle, à peu près dans le même embonpoint où vous m’avez vue à la Muette et je crois qu’il serait à propos de profiter du moment pour finir ce que vous avez si bien commencé. Si vous pouvez venir demain, je serai libre et avec si peu de monde que vous voudrez. Vous connaissez, Monsieur, le cas que je fais de vous et de vos admirables talents. »

6cat3_p_6Vaincu par tant d’insistance, La Tour cède enfin et se rend à Versailles, sur la promesse qu’aucun fâcheux ne viendra interrompre le travail. Mais, en bon philosophe, il est bien résolu à « donner une leçon à ces gens-là ». Dès que la marquise est installée, il se met à son aise, enlève les boucles de ses escarpins, son col, sa perruque, ses jarretières et se coiffe d’un bonnet de taffetas. Survient le roi :

7cat3_p_7– Vous aviez promis, madame que votre porte serait fermée. – Je ne vous dérangerai pas, fait le roi souriant ; je vais rester là bien tranquille. Continuez. – Il ne m’est pas possible d’obéir à Votre Majesté ; je reviendrai lorsque madame sera seule : je n’aime point à être interrompu. Et il s’en fut.

8cat3_p_8Enfin, après trois ans d’efforts et de mécomptes, le portrait fut achevé et figura au Salon de 1855. Malgré l’évidente mauvaise volonté mise par La Tour à peindre la favorite royale, les témoignages du temps s’accordent à reconnaître qu’il mit de la galanterie à l’embellir. Combien différente et plus véridique est la « préparation » du tableau, qui se trouve aujourd’hui au musée de Saint-Quentin !

9cat3_p_9Mais, en dépit de son exécution volontairement flatteuse, ce portrait n’en est pas moins une œuvre de premier ordre, l’une des meilleures de La Tour. Sainte-Beuve lui a consacré une de ses pages les plus brillantes :

10cat3_p_10« C’est la personne même, écrit-il, qui est de tout point merveilleuse de finesse, de dignité suave et d’exquise beauté. Tenant en main le cahier de musique avec légèreté et négligence, elle est tout à coup distraite. Elle semble avoir entendu du bruit et retourne la tête. Est-ce bien le roi qui vient et qui va entrer? Elle a l’air d’attendre avec certitude et d’écouter avec sourire. Sa tête ainsi détournée laisse voir le profil du cou dans toute sa grâce et ses petits cheveux très courts, délicieusement ondés, dont les boucles s’étagent et dont le blond se devine encore sous la demi-poudre qui les couvre à peine. La tête nage dans un fond bleuâtre qui, en général, est celui de tout le tableau. L’œil est partout satisfait et caressé ; c’est de la mélodie plus encore que de l’harmonie. Il n’est rien dans ce boudoir enchanté qui ne semble faire sa cour à la déesse. Elle-même a les chairs et le teint d’un blanc lilas, légèrement azuré. Ce sein, ces rubans, cette robe, tout cet ensemble se marie harmonieusement. Tout dans la physionomie, dans l’attitude, exprime la grâce, le goût suprême, l’affabilité et l’aménité plutôt que la douceur, un air de reine qu’il a fallu prendre, mais qui se trouve naturel et se soutiendra sans trop d’efforts.[2] »

11cat3_p_11Mme de Pompadour se déclara satisfaite du pastel, mais quand vint l’heure du règlement, les difficultés recommencèrent. La Tour ne demandait rien moins que quarante-huit mille livres ! Après bien des pourparlers et des tiraillements, il dut se contenter de la moitié de cette somme, mais il ressentit de cette déconvenue une colère qui fut très longue à s’apaiser.

12cat3_p_12Le portrait de Mme de Pompadour passa, on ne sait comment, entre les mains du comte de Lespinasse d’Arlet, puis fut acquis, en 1797, par le Muséum des Arts. Il resta dans la poussière des réserves nationales jusqu’en 1838, date à laquelle il fut transféré au Louvre, où il figure aujourd’hui dans la salle des Pastels.

13cat3_p_13Hauteur : 1.70. – Largeur : 1.20. – Figure grandeur naturelle.

Voir sur le site des collections du musée du Louvre : https://collections.louvre.fr/ark:/53355/cl020213445 : « Données historiques ».

Bibliographie

Index

C

1indexcontenu_p_1Charles Ier d’Angleterre : Cat. 2

L

2indexcontenu_p_2La Tour, Maurice Quentin de : Cat. 3

3indexcontenu_p_3Léonard de Vinci : Cat. 1

P

4indexcontenu_p_4Pompadour, Jeanne Antoinette Poisson, marquise de : Cat. 3 § 3, Cat. 3 § 5, Cat. 3 § 6 et Cat. 3 § 11

R

5indexcontenu_p_5Rubens, Pierre-Paul : Cat. 2 § 3, Cat. 2 § 4, Cat. 2 § 9, Cat. 2 § 11

V

6indexcontenu_p_6Van Dyck, Antoon : Cat. 2

Catalogue

Introduction

Admirable musée du Louvre

1essai1_p_1Notre étonnement est toujours aussi grand, en parcourant notre admirable musée du Louvre, de le voir si peu fréquenté. Trop souvent le bruit des pas y résonne comme en un temple sans fidèles. Dans ce merveilleux sanctuaire d’art où, siècle par siècle, « l’idéal de tous les peuples » s’est, en quelque sorte, cristallisé en d’incomparables chefs-d’œuvre, bien rares sont les fervents qui viennent porter leur hommage et purifier leur goût. Parfois, sous la conduite d’un employé d’agence, des étrangers le parcourent et l’animent d’une rumeur passagère. Quant au Parisien, ne l’y cherchez pas : on l’y voit si peu !

2essai1_p_2Par la facilité même qu’il a d’entrer au Louvre à tout instant il remet toujours au lendemain la visite projetée. De même du provincial, venu à Paris pour ses affaires ou ses plaisirs. Il aura la plupart du temps tout vu, les promenades, les cabarets, les hippodromes, les théâtres, tout, sauf notre grand musée national.

3essai1_p_3À quoi tient cette indifférence de nos compatriotes pour les musées ? Serait-ce inaptitude à apprécier les œuvres d’art ? Je ne le pense pas, le Français ayant d’instinct le goût du Beau, d’ailleurs certifié par les merveilles d’art de notre pays. Alors ?

4essai1_p_4J’accuserais plus volontiers l’insuffisance actuelle de l’enseignement artistique dans les écoles, insuffisance qui permet à un jeune homme, d’ailleurs pourvu de parchemins, d’ignorer l’existence d’un Velázquez ou d’un Rembrandt. Que ce bon élève, un jour, pénètre dans le Louvre, il sera dès l’abord ahuri, confondu par l’entassement de ces peintures auxquelles il ne comprend rien, dont il ignore tout, l’origine, l’époque et jusqu’au nom de l’auteur.

5essai1_p_5Et ces notions élémentaires qui lui manquent, s’il lui prend fantaisie de les chercher, il ne les trouvera qu’en d’énormes volumes de critique, alourdis de considérations savantes et dont il ne pourra pas dégager la substance. Mais le guide précis, clair, facile à suivre, qui le renseignera brièvement sur la valeur d’une œuvre, la vie de son auteur, les traits essentiels de son talent, où se le procurer ? Inutile de le chercher dans les bibliothèques, il n’y existe pas. Il est encore à faire.

6essai1_p_6Ou, plutôt, il était encore à faire car, si la vanité ne nous aveugle pas, nous croyons pouvoir affirmer qu’il est fait maintenant et c’est ce guide nécessaire que nous vous présentons (Fig. 1 et Fig. 2).

7essai1_p_7La pensée directrice de cet ouvrage, c’est de propager le goût du Beau, de développer le sens artistique par la constante contemplation des plus admirables chefs-d’œuvre de la peinture. Posséder les musées chez soi, à portée de la main à toute heure, à tout instant, quelle heureuse fortune ! Le musée chez soi, c’est-à-dire évoquer la fidèle image de la toile qu’on aime, faire revivre et prolonger à son gré l’émotion ressentie devant les œuvres admirées jadis et qu’on ne reverra peut-être plus ! Quel précieux privilège de pouvoir contempler ainsi tous les tableaux célèbres, épars dans les musées les plus lointains, à Madrid, à Amsterdam, à Saint-Pétersbourg, à Rome !

8essai1_p_8Et quel concours miraculeux nous fournit la science moderne !

9essai1_p_9La photographie noire, sans lumière, uniforme de tons, a désormais vécu pour faire place à la photographie des couleurs.

10essai1_p_10Ah ! l’admirable découverte, en vérité ! Grâce à elle, la peinture nous est restituée tout entière ; c’est le tableau lui-même qui revit sous nos yeux. Regardez, tout s’y trouve, exactement rendu, le velouté des chairs, le chatoiement des étoffes, le scintillement des bijoux, la transparente légèreté des ciels, la profondeur lumineuse des ombres. Les nuances les plus fines, les frottis les moins appuyés y sont traduits avec la même précision que les plus forts empâtements. Cela n’est-il pas merveilleux, et n’est-il pas juste de dire que, possédant un tel ouvrage, on possède réellement le musée chez soi ?

11essai1_p_11Quelques lecteurs s’étonneront peut-être de rencontrer dans une sorte de désordre des œuvres très différentes d’époque, d’école et de genre. Mais cette apparente confusion n’est pas involontaire.

12essai1_p_12Elle est le résultat de considérations faciles à justifier. L’ouvrage que nous présentons au public n’est pas, en effet, purement didactique, au sens étroit du mot. Il est fait, certes, pour instruire, mais pour instruire sans ennui. Un volume d’enseignement, en matière d’art, implique généralement une classification soit par époques, soit par écoles, classification d’où se dégage toujours une certaine monotonie. Donner tout d’une traite l’école flamande, par exemple, c’est la redite obligatoire et continue des scènes d’intérieur et des scènes de cabaret, fatigantes à la longue, quelle que soit d’ailleurs la valeur intrinsèque de l’œuvre, de même que l’œil se fatiguerait aussi d’une suite ininterrompue de Madones italiennes ou de Descentes de Croix, fussent-elles signées des plus grands noms (voir Cat. 1).

13essai1_p_13Ici, au contraire, la fantaisie seule nous a guidés comme seule, dans un musée, elle guide les pas du promeneur qui s’arrête à son gré devant la toile qui l’attire, portrait, allégorie, scène d’histoire ou peinture de genre.

Une promenade pleine d’imprévu

14essai1_p_14Pareil à ce visiteur, nous n’avons prétendu faire qu’une libre promenade à travers le Louvre, promenade intéressante au plus haut point, toujours pleine d’imprévu, où chaque pas amène une surprise et une émotion nouvelles, fixant au passage les œuvres glorieuses qui rayonnent dans notre grand musée. N’est-ce point là la meilleure méthode et la plus attrayante ? Nous l’avons pensé et c’est elle que nous avons adoptée dans la présentation de ce volume.

15essai1_p_15Au hasard de la course, les époques, les écoles, les nationalités vont se confondre. L’école flamande (voir Cat. 2) voisinera souvent avec l’école française (voir Cat. 3), un Hollandais avec un Espagnol, un romantique avec un primitif, comme les fleurs les plus diverses dans un merveilleux jardin. Sans plus d’égards pour les genres, portraits (voir Cat. 1, Cat. 2, Cat. 3), allégories, sujets religieux, paysages, tableaux mythologiques alterneront au cours de ces pages, l’un nous reposant de l’autre et nous permettant de les mieux goûter tous. Ainsi conduite, la promenade est sans fatigue ; elle s’égaie de rencontres inattendues; elle puise le meilleur de son charme dans son infinie variété.

16essai1_p_16Variété qui n’enlève rien, d’ailleurs, à la portée éducative de l’ouvrage, bien au contraire, chaque planche étant accompagnée d’une notice explicative. Cette notice, nous l’avons voulue claire, précise, documentaire, débarrassée de considérations générales et dégagée des querelles d’école, assez courte pour n’être pas fatigante, assez longue pour être complète. Sur chaque œuvre reproduite elle dira tout ce qu’on en peut dire sous une forme résumée : l’événement qui en amena l’exécution, les qualités qui la distinguent, les particularités de la composition, du dessin ou du coloris, le tout fortifié par l’opinion autorisée d’un critique éminent. Du peintre lui-même nous saurons, dès le premier contact, ce qu’il importe d’en savoir, son caractère, son histoire, les anecdotes intéressantes de savie, les traits essentiels de son talent. Et lorsque le lecteur rencontrera plus loin un autre tableau du même peintre (voir Fig. 3-1), il le reconnaîtra de lui-même avant d’avoir lu le nom, sur la physionomie générale de l’œuvre, comme on reconnaît de loin un ami dans la rue avant même de distinguer les traits de son visage. Par la diversité des artistes et des œuvres, les similitudes et les différences de chacun d’eux se fixeront dans son esprit, et les classifications s’opéreront automatiquement, sans effort. Et, peu à peu, par une lente progression, sans même qu’il s’en aperçoive, il aura meublé son esprit et formé son goût. Un tel résultat suffirait à justifier cet ouvrage, ou plutôt cette série d’ouvrages, puisque, au Louvre, succéderont les Offices et le Palais Pitti de Florence, la National Gallery de Londres, l’Académie de Venise, le Prado de Madrid, les musées d’Allemagne et d’Autriche, etc.

17essai1_p_17Puissions-nous, par cette publication à la fois séduisante et éducative, avoir contribué à faire pénétrer dans le public français, d’une sensibilité artistique si grande, mais, cependant, il faut bien le reconnaître, trop souvent ignorant des merveilles qui peuplent nos musées nationaux et ceux de l’étranger, le goût de l’éternelle Beauté et le désir d’en pénétrer le mystère.

18essai1_p_18Armand Dayot

19essai1_p_19Inspecteur général des Beaux-Arts

Colophon

À propos

1colophon_p_1En publiant en ligne sa chaîne de publication d’ouvrages multiformat, le musée du Louvre poursuit son engagement vers l’accès gratuit, illimité et immédiat aux publications de la recherche scientifique. Les fonctionnalités de zoom et de manipulation des images numériques sont destinées à donner à l’édition scientifique en histoire de l’art son plein potentiel. Cet ouvrage est également disponible dans les formats ePub, PDF et en version imprimée. L’ensemble de ces formats lui garantissent maniabilité, pérennité, citabilité, référencement et présence dans les catalogues de librairies et de bibliothèques. Le musée du Louvre s’est attaché à produire un livre qui, dans tous ses formats, soit élégant et édité avec soin, afin d’offrir aux objets archéologiques et aux textes savants toute la qualité et la sensibilité attachées aux livres d’art.

Musée du Louvre

2colophon_p_2Christophe Leribault président-directeur

3colophon_p_3Kim Pham administrateur général

4colophon_p_4Francis Steinbock administrateur général adjoint

5colophon_p_5Aline François-Colin directrice des Expositions et des Éditions

Édition

colophon_h4_0Musée du Louvre

6colophon_p_6Laurence Basset directrice adjointe des Éditions

7colophon_p_7Camille Sourisse cheffe de projet, coordination et suivi éditorial

colophon_h4_1Collaborations

8colophon_p_8Nicolas Taffin C&F éditions, chef de projet, éditeur

9colophon_p_9Hervé Le Crosnier C&F éditions, suivi de projet

10colophon_p_10Julien Taquet conception et développement du site et de la chaîne de publication

11colophon_p_11Agathe Baëz conception graphique, intégration et mise en page

Informations éditeur

12colophon_p_12© musée du Louvre, Paris, 2026

13colophon_p_13https://www.louvre.fr

14colophon_p_14Ce livre est réalisé avec un assemblage d’outils libres, gratuits et open source permettant la génération de livres pour l’écran (site web) et le papier. Le site statique 11ty (https://11ty.dev). La mise en page de la version imprimée (PDF) de cet ouvrage a été réalisée avec Paged.js (https://pagedjs.org), bibliothèque javascript qui permet de transformer tout flux HTML en PDF prêt pour l’impression.

15colophon_p_15Cet ouvrage a été composé en Cooper et Basteleur.

16colophon_p_16La description des images à l’attention des personnes aveugles et malvoyantes a été réalisée par Camille Sourisse.

Obtenir cet ouvrage

17colophon_p_17Le livre est librement téléchargeable aux formats numériques ePub et PDF :

18colophon_p_18https://livres.louvre.fr/assets/louvre1912/demonstrateur.epub

https://livres.louvre.fr/assets/louvre1912/demonstrateur.pdf.

19colophon_p_19Pour une lecture optimale sur liseuse, l’ePub requiert un appareil pleinement compatible avec le format epub3.

Citer cet ouvrage

20colophon_p_20Armand Dayot (dir.), Sustainable Financing for Health. A User Guide for African Governments, Paris, musée du Louvre, 2026, https://livres.louvre.fr/louvre1912.

Foreword

1foreword_p_1For many decades, the question of how African countries can sustainably finance essential public health services has remained both urgent and complex. The continent’s development aspirations are ambitious, yet traditional financing sources have proven insufficient to meet the scale of current needs. Today, African governments simultaneously face the challenges of underfunded health systems and the escalating demands brought about by pandemics, rising incidents of non-communicable diseases, and other public health crises.

2foreword_p_2These pressures have compelled policymakers, development institutions, and financial advisors to rethink conventional approaches to public financing. The African Legal Support Facility (ALSF) recognises and supports the pressing need of governments to identify and implement tools that enable effective and sustainable health sector financing. Innovative instruments are now central to global conversations on how countries can responsibly mobilise resources while maintaining fiscal stability.

3foreword_p_3It is against this backdrop that the ALSF, with the support of the Gates Foundation, convened a diverse group of leading experts in law, finance, public health, and policy to develop “Sustainable Finance for Health: A User Guide for African Governments” (“the User Guide”). This first-of-its-kind resource responds directly to the growing interest in mechanisms such as health-focused bonds and loans, sustainability-linked debt instruments, debt-for-health swaps, and health PPPs - instruments that have been deployed globally to catalyse key investments in priority health programmes.

4foreword_p_4Despite their promise, these innovative health financing mechanisms remain underutilised, in some cases due to their legal and structural complexities. The User Guide aims to close that knowledge gap. It provides clear, practical guidance to support governments in navigating the full lifecycle of these instruments: from conceptualisation and policy alignment, to transaction structuring, documentation, negotiation, and implementation. Drawing on lessons from global initiatives such as the Global Fund to Fight Aids, tuberculosis and malaria (the “Global Fund”) and other pioneering models, it presents best practices in an accessible, actionable format.

5foreword_p_5As with previous ALSF knowledge products, this User Guide reflects the collective expertise of contributors, in this case, drawn from multilateral institutions, law firms, academia, global health organisations, and advisory practices. Their perspectives have been shaped not only by sectoral knowledge but by extensive on-the-ground experience working with and within African governments. The result is a balanced, multidisciplinary reference designed to strengthen institutional capacity across ministries of finance, health, and planning as well as among debt managers and policymakers. To ensure a collaborative and time-efficient drafting process, the User Guide was produced using the Book Sprint methodology, an intensive group writing workshop. This approach, grounded in discussion, experience sharing, and expert insight, has ensured that the final product is firmly relevant to Africa’s real-world challenges and opportunities.

6foreword_p_6We hope this User Guide will support African governments in making informed and strategic decisions as they work to scale up health sector investments and strengthen public financial management. While these materials offer guidance and practical tools, they are not a substitute for professional advice. They should be used in conjunction with tailored legal and transactional expertise - which the ALSF was established to provide and stands ready to offer.

7foreword_p_7On behalf of the African Legal Support Facility, I extend my sincere appreciation to all contributing authors, remote collaborators, facilitators, and reviewers whose dedication and expertise made this User Guide possible. I also acknowledge our partners and stakeholders across the continent, whose continued commitment to advancing sustainable financing for health consistently informs and inspires our work. In particular, I wish to express special thanks to the West African Institute for Financial and Economic Management (WAIFEM) and the Macroeconomic and Financial Management Institute of Eastern and Southern Africa (MEFMI) for their valuable support during the review process, as well as to the senior African government technical experts whose insights ensured that the User Guide reflects the practical perspectives, priorities, and collective voice of its intended end users, the African governments.

8foreword_p_8As African countries navigate a rapidly shifting global landscape, the ALSF remains steadfast in its support for solutions that promote responsible borrowing, strengthened health systems, and long-term socio-economic development. We trust that this User Guide will be a valuable resource in advancing those goals.

9foreword_p_9Olivier Pognon

Director and CEO

African Legal Support Facility

THE AFRICAN LEGAL SUPPORT FACILITY

10foreword_p_10The African Legal Support Facility (ALSF) is an international organisation which broadly aims to remove asymmetric technical capacities between public- and private-sector stakeholders. The ALSF was initially established in response to the rise in vulture fund litigation against African sovereigns, but quickly expanded to assist African governments in negotiating complex commercial transactions. The ALSF intervenes in matters related to sovereign debt, power, infrastructure and the extractive sectors.

11foreword_p_11www.alsf.org

12foreword_p_12NB: This User Guide is issued under the Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International Licence (CC BY-NC-SA 4.0), which allows anyone to copy, excerpt, rework, translate and re-use the text for any non-commercial purpose without seeking permission from the authors, so long as the resulting work is also issued under a Creative Commons Licence.

A User Guide for African Governments

1homepage_p_1Sustainable Financing for Health: A User Guide for African Governments (the Guide) is a practical resource designed to support African governments in financing priority health investments in a fiscally responsible and sustainable manner. It is written primarily for Ministries of Health (MoHs) and Ministries of Finance (MoFs) and is intended to strengthen collaboration between them as they identify health priorities, assess financing options, and structure transactions that align with national development plans and macro-fiscal frameworks. The Guide responds to growing demands from governments for clear, action-focused guidance at a time of tightening fiscal space, rising debt pressures, shifting donor support, and increasing health system demands.

2homepage_p_2The Guide does not introduce new instruments. Rather, by building on established global practices and African experiences, the Guide demonstrates how existing financing mechanisms can be applied effectively to health priorities. It examines debt-for-health swaps, sustainability-linked and use-of-proceeds instruments, public-private partnerships (PPPs), and credit enhancement tools, explaining how each can be structured, governed, and implemented within national legal and institutional frameworks. Through case studies, practical tools, and structured guidance, the Guide helps officials assess readiness, manage risks, understand documentation and process requirements, and adapt these instruments to country-specific fiscal conditions and health sector needs.

Préface

1preface_p_1Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nulla sed nunc enim. Vivamus eget nibh enim. Proin sed erat nulla, et pharetra massa. Ut malesuada pharetra malesuada. Aliquam at elit ut quam adipiscing accumsan. Quisque nisl lorem, adipiscing sed feugiat vel, rutrum eu arcu. Nullam aliquet metus ut lectus egestas ornare vitae quis justo. In velit odio, scelerisque sed egestas ac, cursus ac velit." Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nulla sed nunc enim. Vivamus eget nibh enim. Proin sed erat nulla, et pharetra massa. Ut malesuada pharetra malesuada. Aliquam at elit ut quam adipiscing accumsan. Quisque nisl lorem, adipiscing sed feugiat vel, rutrum eu arcu. Nullam aliquet metus ut lectus egestas ornare vitae quis justo. In velit odio, scelerisque sed egestas ac, cursus ac velit." Lorem ipsum dolor sit amet, consectetur adipiscing elit. Nulla sed nunc enim. Vivamus eget nibh enim. Proin sed erat nulla, et pharetra massa. Ut malesuada pharetra malesuada. Aliquam at elit ut quam adipiscing accumsan. Quisque nisl lorem, adipiscing sed feugiat vel, rutrum eu arcu. Nullam aliquet metus ut lectus egestas ornare vitae quis justo. In velit odio, scelerisque sed egestas ac, cursus ac velit."

Executive Summary

1exec-sum_p_1Sustainable Financing for Health: A User Guide for African Governments (the Guide) is a practical resource designed to support African governments in financing priority health investments in a fiscally responsible and sustainable manner. It is written primarily for Ministries of Health (MoHs) and Ministries of Finance (MoFs) and is intended to strengthen collaboration between them as they identify health priorities, assess financing options, and structure transactions that align with national development plans and macro-fiscal frameworks. The Guide responds to growing demands from governments for clear, action-focused guidance at a time of tightening fiscal space, rising debt pressures, shifting donor support, and increasing health system demands.

2exec-sum_p_2The Guide does not introduce new instruments. Rather, by building on established global practices and African experiences, the Guide demonstrates how existing financing mechanisms can be applied effectively to health priorities. It examines debt-for-health swaps, sustainability-linked and use-of-proceeds instruments, public-private partnerships (PPPs), and credit enhancement tools, explaining how each can be structured, governed, and implemented within national legal and institutional frameworks. Through case studies, practical tools, and structured guidance, the Guide helps officials assess readiness, manage risks, understand documentation and process requirements, and adapt these instruments to country-specific fiscal conditions and health sector needs.

Why This Guide, and Why Now?

3exec-sum_p_3The timing of this Guide is critical. Many African countries are experiencing sharp reductions in Official Development Assistance, heightened debt burdens and lingering post-COVID fiscal constraints. Simultaneously, the continent faces significant population growth, persistent health service delivery gaps, and a need to increase domestic health investments. Meeting these challenges requires not just more funding but smarter financing.

4exec-sum_p_4This Guide fills an important gap in existing resources by offering an Africa-specific, government-facing tool that brings together legal, fiscal, and technical dimensions. It seeks to enhance collaboration between MoHs and MoFs, and to foster a shared understanding of what instruments are appropriate, feasible, and impactful in various circumstances.

1. Key Features

- exec-sum_ul_0

- exec-sum_li_0Modular design. The Guide is structured so that users can consult individual chapters or specific financing instruments as needed, depending on their context and role in the financing process.

- exec-sum_li_1Country ownership. Emphasises country-led planning and health sector prioritisation as the foundation for any financing solution.

- exec-sum_li_2Capacity building. Encourages institutional strengthening through embedded tools, guidance, and references complementary to ALSF and partner resources.

- exec-sum_li_3Legal clarity. Outlines the relevant legal frameworks, documentation requirements, and workflow processes required to support each instrument and related transactions.

2. Chapters

5exec-sum_p_5The Guide is designed for use by cross-functional teams of policymakers, legal experts, and technical officials working across MoHs and MoFs. It walks users through:

- exec-sum_ul_1

- exec-sum_li_4Key considerations when selecting financing instruments, including fiscal implications, regulatory requirements, and institutional capacity;

- exec-sum_li_5Practical structuring pathways and steps to design transactions that deliver tangible health impacts;

- exec-sum_li_6Decision tools to help with planning, negotiation, and implementation; and

- exec-sum_li_7Risk mitigation and governance approaches to safeguard public interest and improve execution.

6exec-sum_p_6The Guide is organised into the following nine chapters.

CHAPTER 1: SETTING THE SCENE

7exec-sum_p_7This chapter establishes the context and rationale for the Guide. It outlines the structural pressures facing African health systems, including persistent underfunding, growing disease burdens, demographic change, constrained fiscal space, and evolving donor priorities. The chapter explains why governments must move beyond reliance on traditional budgetary allocations and external aid alone, and instead take a more strategic, coordinated approach to financing health. It clarifies the purpose of the Guide as a practical tool to support MoHs and MoFs in jointly identifying, assessing, and operationalising financing solutions that are aligned with national priorities and fiscal realities.

CHAPTER 2: FINANCING FOR HEALTH

8exec-sum_p_8This chapter provides the conceptual foundation for the rest of the Guide. It explains how health financing systems function, including revenue collection, pooling of funds, and purchasing of services. It examines the different sources of health financing, domestic public expenditure, private expenditure, and external assistance, and discusses their implications for sustainability and equity. The chapter also sets out the respective and complementary roles of MoHs and MoFs, highlighting the importance of coordination between sectoral planning and macro-fiscal management. By mapping the institutional architecture and key actors involved in health financing, the chapter anchors later discussions of specific instruments within the broader system in which they must operate.

CHAPTER 3: COMMON CONSIDERATIONS

9exec-sum_p_9Chapter 3 focuses on the cross-cutting conditions that must be in place for financing instruments to be effective and sustainable. It highlights the legal, regulatory, and institutional frameworks that shape health financing decisions, including public financial management systems, debt management rules, procurement frameworks, and approval processes. The chapter underscores the importance of regulatory alignment, fiscal risk assessment, transparency, and inter-ministerial coordination. It also addresses institutional capacity, governance arrangements, and the need to tailor financing solutions to country-specific legal and fiscal contexts. This chapter serves as a readiness lens, helping officials assess whether the enabling environment can support the instrument under consideration.

CHAPTER 4: HEALTH FINANCE AND KEY PERFORMANCE INDICATORS

10exec-sum_p_10Chapter 4 links financing to outcomes. It begins by situating national health financing within the broader global health architecture, including the role of major international institutions and financing partners that support health investments across Africa. It then outlines the main categories of health expenditure and typical programmatic areas financed within the sector. The central focus of the chapter is the role of key performance indicators (KPIs). It explains how measurable indicators are used to connect financing to results, particularly in performance-based, sustainability-linked, and results-oriented instruments. By clarifying how KPIs are defined, monitored, and verified, the chapter provides the analytical bridge between financial structuring and measurable improvements in health outcomes.

CHAPTER 5: SUSTAINABLE FINANCE INSTRUMENTS

11exec-sum_p_11Chapter 5 aims to guide officials from MoFs and MoHs, as well as practitioners, on the design and implementation of sustainable financing instruments - specifically use of proceed and sustainability-linked bonds and loans, and impact bonds as mechanisms to mobilise public and private capital for health objectives. It explains core structuring elements, including the identification of eligible health expenditures or measurable KPIs and sustainability performance targets, and highlights the importance of credible monitoring, reporting, and verification systems aligned with market standards.

12exec-sum_p_12The chapter also addresses the supporting legal and transactional frameworks for such instruments, including the preparation of sustainable finance frameworks, external reviews, and the incorporation of binding use of proceeds, reporting, and performance related provisions in bond or loan documentation. It sets out enabling conditions, inter-ministerial coordination requirements, and includes practical checklists and workflow processes to guide governments from preparation through issuance and ongoing compliance.

CHAPTER 6: DEBT-FOR-HEALTH SWAPS

13exec-sum_p_13This chapter explains the structure and rationale of debt-for-health swaps, under which a portion of external debt is cancelled, reduced, or restructured in exchange for a commitment to invest agreed amounts in priority health programmes. The chapter distinguishes between bilateral debt swaps, concluded between official bilateral creditors and debtor governments, and commercial debt conversions involving private creditors, often supported by intermediaries or credit enhancers. The chapter outlines the potential benefits, including fiscal space creation and targeted investment in health, as well as key risks such as complex negotiations, governance and fiduciary challenges, and possible implications for credit ratings and future market access.

14exec-sum_p_14In addition, the chapter sets out the transaction architecture and process steps required to operationalise a swap. It describes the preparatory phase, including debt stock analysis, identification of eligible obligations, stakeholder mapping, and alignment with national health priorities. It outlines the negotiation and structuring phase, including term sheet development, creditor engagement, and the design of governance and oversight arrangements for the health investment component.

15exec-sum_p_15Finally, the chapter highlights the legal documentation typically required, such as framework agreements, swap agreements, trust or fund arrangements, and implementation protocols, as well as monitoring and reporting mechanisms to ensure transparency, accountability, and measurable health outcomes. Practical process maps and checklists are provided to guide ministries through feasibility assessment, negotiation, documentation, and post swap implementation.

CHAPTER 7: THE USE OF PUBLIC-PRIVATE PARTNERSHIPS IN HEALTHCARE PROJECTS

16exec-sum_p_16Chapter 7 provides structured guidance on the application of PPPs in the health sector. Part 1 of this chapter clarifies the defining features of health PPPs, the policy objectives they can serve, and the circumstances in which they are suitable. It emphasises value for money, fiscal affordability, risk allocation discipline, and the need to align PPP structures with national health priorities and public financial management frameworks.

17exec-sum_p_17Part 2 sets out the full PPP lifecycle, from project identification and screening through feasibility analysis, structuring, procurement, contract award, and long-term contract management. The chapter includes practical tools such as project screening criteria, feasibility and affordability assessment guidance, risk allocation matrices, procurement integrity safeguards, and contract management checklists. It also highlights the key legal considerations underpinning health PPPs, including enabling legislation, procurement compliance, contractual documentation, performance and payment mechanisms, dispute resolution provisions, and ongoing monitoring and reporting obligations. Together, these tools and process maps are intended to guide officials in structuring bankable, transparent, and accountable health PPP transactions.

CHAPTER 8: CREDIT ENHANCEMENT

18exec-sum_p_18Chapter 8 explains how credit enhancement can improve access to finance for health by reducing perceived risk and lowering the cost of capital. It sets out the main credit enhancement options used in practice, including partial and full guarantees, political risk insurance, liquidity facilities, reserve accounts and cash collateral structures, and other forms of risk sharing with development finance institutions and insurers. The chapter guides officials on how to select an appropriate instrument based on the underlying transaction, the risk being addressed, and the intended impact on pricing, tenor, and investor appetite.

19exec-sum_p_19The chapter also provides practical guidance on structuring and implementation. It outlines key questions for assessing feasibility, including the trigger conditions, coverage scope, claims process, and interaction with the base bond or loan terms. It highlights the main legal and governance considerations, including authority to issue or accept guarantees, approval and procurement requirements, disclosure and reporting obligations, and recording contingent liabilities in line with public debt and fiscal risk management frameworks.

CHAPTER 9: RECOMMENDATIONS

20exec-sum_p_20The final chapter provides recommendations aimed at strengthening the enabling environment for health financing transactions and improving decision-making. It separates recommendations for MoHs and MoFs, focusing on planning, cross government collaboration, realistic budgeting, and stronger risk and contingent liability management.

Key recommendations at a glance

21exec-sum_p_21Recommendations for MoHs include:

- exec-sum_ul_2

- exec-sum_li_8Advocate for fair and realistic allocations to health.

- exec-sum_li_9Take a long-term, strategic view in financing health priorities.

- exec-sum_li_10Build credible execution capacity and data-driven delivery.

- exec-sum_li_11Collaborate closely with the MoF to design and execute health financing instruments.

22exec-sum_p_22Recommendations for MoFs include:

- exec-sum_ul_3

- exec-sum_li_12Put blended finance tools at the centre of national borrowing plans.

- exec-sum_li_13Ensure visibility over budget execution for the health sector.

- exec-sum_li_14Standardise and improve health finance data.

- exec-sum_li_15Establish a task force to mobilise credit enhancement for health funding.

- exec-sum_li_16Build the capacity of the MoF and the MoH to jointly engage in innovative financing instruments.

23exec-sum_p_23Overall, the Guide supports governments to make better structured choices, grounded in law, public finance rules, and implementation capacity. It encourages early collaboration between health and finance teams, careful use of indicators and safeguards, and disciplined use of advisors and documentation so that financing decisions translate into deliverable health outcomes.

Contributing Authors

Chapter 1: Setting the Scene

1chap1_p_1Health is central to sustainable development. Across Africa, governments face the dual challenge of improving health outcomes and access to healthcare while preserving fiscal sustainability. Historically, African countries have relied heavily on Official Development Assistance (ODA) to finance their health objectives, with ODA accounting for 30-50% of Total Health Expenditure (THE) in low-income settings. Yet, global aid is contracting and health support is declining even faster, reaching its lowest level in over a decade.

2chap1_p_2This comes at a time when public health emergencies are on the rise (a report by Africa CDC: Africa’s Health Financing in a New Era - April 2025, reports a 41% increase, from 152 in 2022 to 213 in 2024), exposing chronic underinvestment in health infrastructure and in healthcare workers (HCWs). The COVID-19 pandemic highlighted that health is not only a social priority but also a foundation of economic resilience and national security. Meanwhile, global health institutions such as the World Health Organisation (WHO), the Global Fund to Fight Aids, tuberculosis and malaria (Global Fund), Gavi and the World Bank continue to play a pivotal role in financing and technical assistance. Still, their focus is shifting toward catalytic funding models (a type of financing that seeks to create positive social and environmental impacts in addition to generating financial returns), co-financing requirements and greater country ownership, underscoring the need for governments to mobilise sustainable domestic resources and to leverage innovative financing instruments.

Objectives of the User Guide

3chap1_p_3This User Guide is a practical, action-oriented resource for African governments, particularly for ministries of health and finance, on designing, negotiating and implementing sustainable health financing solutions - in particular sustainable financing instruments, debt swaps and public-private partnerships. It simplifies these complex tools and provides clear frameworks for assessing readiness, structuring transactions and ensuring long-term value for health systems. While the Ministry of Finance (MoF) leads on fiscal and debt-related engagements, the Ministry of Health plays a critical role in defining the investment case, aligning interventions with national priorities and ensuring that the proceeds of innovative financing directly strengthen health outcomes and systems. The User Guide promotes a shared understanding of how finance and health authorities can collaborate to leverage financial innovation for tangible benefits to population health and resilience.

Note on One Health and Cross-Sectoral Collaboration4chap1_p_4Throughout this Guide, references to the “Ministry of Health” should be understood in a broader context that aligns with the One Health approach. In many countries, the health sector includes several line ministries and government agencies working across human, animal, and environmental health. While the Ministry of Health is typically the lead actor, successful health financing strategies often require coordination with other relevant ministries, including those responsible for agriculture, environment, social protection, and infrastructure. This Guide encourages governments to adopt inclusive approaches that reflect their national institutional arrangements and health priorities. 5chap1_p_5For more details on the One Health approach and its implications for health financing and cross-sectoral coordination, the reader is referred to the World Health Organization (WHO), Food and Agriculture Organization (FAO), and World Organisation for Animal Health (WOAH) joint One Health framework, which highlights the interdependence of human, animal, and environmental health sectors and the importance of integrated planning and resource mobilisation at https://www.who.int/health-topics/one-health |

How the User Guide Complements Existing Tools

6chap1_p_6While several frameworks and publications exist on health financing, this User Guide provides an African-led perspective on health systems and their funding challenges. It also suggests frameworks for undertaking transactions with deliverable financing instruments that are grounded in legal and institutional realities. It builds on existing strategies and tools by bridging the gap between planning and execution, offering practical guidance on additional options for revenue mobilisation, deal structuring and legal considerations. It complements national health financing strategies, expenditure frameworks and toolkits developed by the WHO, Gavi, the Global Fund and other partners.

How to Use It

7chap1_p_7Rather than being read from cover to cover, the User Guide is organised in a modular format. Users can engage with specific instruments or tools based on their needs, stage of the financing process or institutional role. The resource can be used in several ways:

- chap1_ul_0

- chap1_li_0As a capacity-building tool, it aims to deepen understanding of instruments like thematic and sustainability-linked bonds, debt-for-health swaps and health-related public-private partnerships (PPPs).

- chap1_li_1As a readiness assessment tool, it guides policymakers in understanding and evaluating the enabling conditions, fiscal space and institutional preparedness required to obtain such financing.

- chap1_li_2As a legal and negotiation reference, with model clauses and checklists to support transaction teams.

- chap1_li_3As a decision-support guide, it helps policymakers assess the appropriateness of different instruments in light of fiscal realities and health priorities.

- chap1_li_4As a coordination guide, supporting joint planning between MoHs and MoFs, other government departments and agencies and other stakeholders.

8chap1_p_8Throughout, the User Guide draws on real-world examples. Importantly, however, it is intended to complement, not replace, national policies, legal frameworks or planning processes.

9chap1_p_9Users are also encouraged to consult related resources such as the ALSF Sovereign Debt Handbook and ALSF Debt Document Commentaries for technical insights into legal structuring and compliance, in particular, the ALSF Sustainability Financing Debt Guide and the ALSF Debt Swaps Guide.

What This User Guide Is Not

10chap1_p_10While this User Guide provides a robust foundation for understanding and applying health financing instruments, it does not purport to contain all the information each user may require on such instruments. It is also not a substitute for professional legal, financial or technical advice. The design and execution of complex transactions, especially those involving PPPs or sovereign borrowing, require the expertise of qualified professionals. Governments are strongly encouraged to seek such support in all phases of implementation.

Chapter 2: Financing for Health

1chap2_p_1This chapter provides the background and rationale for the User Guide. It explains why health is central to sustainable development, outlines the current financing challenges related to health systems in African countries and introduces the key financing instruments outlined in the resource. It also begins to identify everyday health expenditures and indicators that lend themselves well to these external financing options, as well as key considerations that governments must take into account when choosing the indicators.

Why Health Matters

2chap2_p_2Health is both a moral imperative and a foundation for economic and social development. The global community’s commitment to health is enshrined in the Sustainable Development Goals (SDGs), particularly SDG 2 (Zero Hunger) and SDG 3 (Good Health and Well-being). These set ambitious goals to substantially and sustainably improve the health of all people. Yet, beyond moral obligation, the case for investing in health is also profoundly economic. Healthier populations are more productive, more resilient and more capable of driving long-term national growth.

3chap2_p_3Evidence from across regions shows that investments in health yield among the highest returns of any public expenditure. Global analyses from the World Health Organisation (WHO) and the Global Fund suggest an average return on investment exceeding 30:1. These gains reflect the multiple channels through which health fuels development, from reducing absenteeism and increasing labour productivity to enhancing children’s learning outcomes and enabling women’s greater participation in the workforce.

4chap2_p_4Most importantly, health remains one of the issues citizens care about the most. The 2024 Afrobarometer survey found that health ranks second, on average, among the most critical problems for governments to address, behind only unemployment. This demand reflects a simple reality: when people are healthy, communities thrive, economies function and social contracts are strengthened.

5chap2_p_5For policymakers, therefore, investing in health is not just about meeting humanitarian goals; it is about safeguarding the very foundations of growth and stability. Recognising this link between health and prosperity is essential for both Ministries of Health (MoHs) and Ministries of Finance (MOFs) as they navigate the choices and trade-offs that shape national development.

The Funding Crisis

6chap2_p_6Over the past two decades, Africa has made remarkable gains in health: access to care has expanded, maternal and child mortality have fallen, and coverage of key services, such as immunisation, human immunodeficiency virus (HIV) treatment and other disease programmes, has increased significantly. These achievements reflect the dedication of governments, communities and development partners working to strengthen health systems and broaden service reach.

7chap2_p_7Much of this progress has been underpinned by external financing. For years, organisations such as the Global Fund, Gavi, the World Bank and significant bilateral donors have provided the resources that have helped to close domestic funding gaps.

8chap2_p_8That financial landscape is now changing rapidly. In 2024, total Official Development Assistance (ODA) from the Organisation for Economic Co-operation and Development - Development Assistance Committee members declined by 7.1% in real terms. In 2025, countries in sub-Saharan Africa are expected to see a 16-28% reduction compared to 2021, the most significant reduction among all regions. Additionally, health-specific aid is declining at a faster rate than other sectors. The most prominent donors, accounting for 80% of bilateral health and population aid, are expected to reduce their ODA contributions, with the United States alone providing over half of the historical contributions. These contractions occur at a time when health systems are under increasing pressure, as evidenced by the 41% increase in public health emergencies between 2022 and 2024.OECD. (n.d.). Official development assistance (ODA). Organisation for Economic Co-operation and Development. https://www.oecd.org/en/topics/policy-issues/official-development-assistance-oda.html

9chap2_p_9The decline in donor funding is exacerbated by a dramatically tightening fiscal space within African governments. At least 22 countries on the continent are now in or at high risk of debt distress, and more than 30 countries pay more annually on debt servicing (the total amount of money required to pay the interest and principal on existing debt) than on their health sectors.

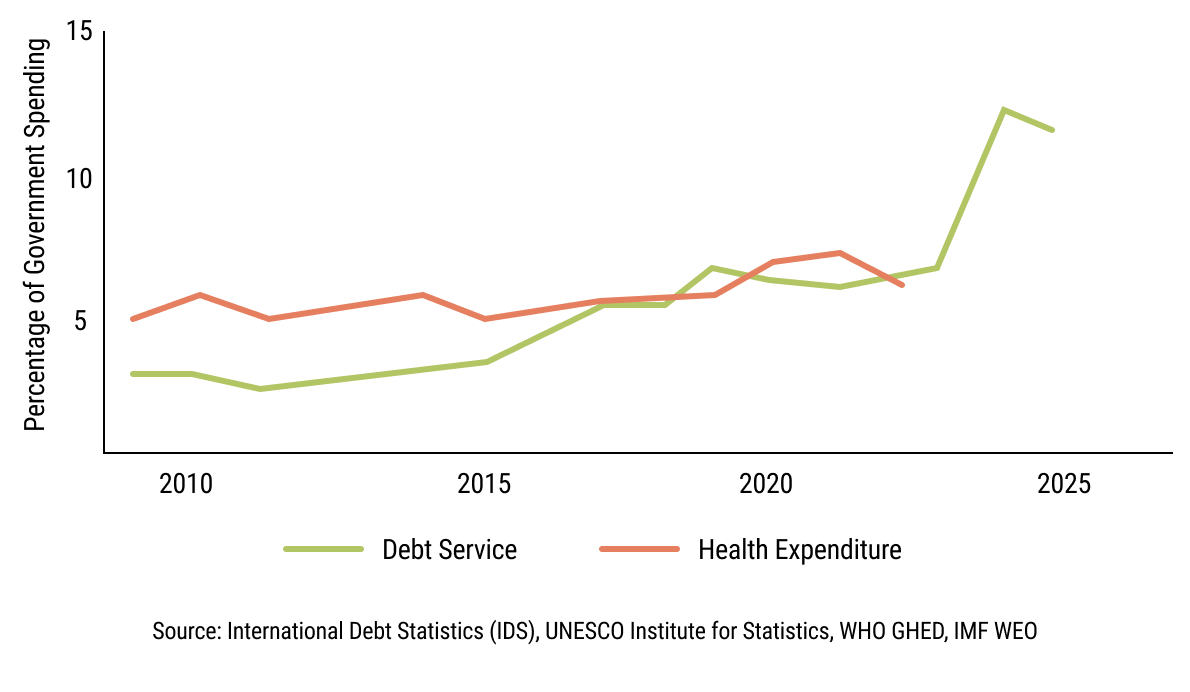

chap2_img_0

chap2_img_010chap2_p_10This triple pressure - shrinking external support, increasing healthcare needs and increasing debt servicing on existing debt obligations - forces governments to balance the imperative of improving health outcomes with the need to preserve macroeconomic fiscal stability. The result is a growing mismatch between what citizens need and what national budgets can sustainably deliver.

11chap2_p_11This is where collaboration between MoHs and MoFs becomes essential. Together, they must look beyond traditional budget allocations to identify and implement financing instruments, such as public-private partnerships (PPPs), debt swaps and other sustainable debt instruments that can expand fiscal space for health while maintaining financial sustainability. They should also consider the shifting roles of major health funders, such as the Global Fund, Gavi and the World Bank, as described in Chapter 4: Health Finance and Key Performance Indicators.

Case Study: Situating This User Guide Within National Health Financing Strategies12chap2_p_12Every country’s path to universal health coverage (UHC) is unique, but the principles of sound health financing remain the same. Health financing strategies are designed to chart a financially feasible pathway toward UHC, ensuring that everyone can access the health services they need without suffering financial hardship. Progress is measured along three dimensions: the range of services provided, the share of the population covered and the extent to which individuals are protected from out-of-pocket costs. 13chap2_p_13Within this broader framework, this User Guide offers practical options for governments seeking to increase health expenditure and move closer to UHC sustainably. It focuses on three financing instruments - PPPs, debt swaps and sustainable debt instruments - that can help countries mobilise and channel additional resources for health. However, these options are not stand-alone solutions. They should be considered complementary tools that operate within and are guided by a country’s overarching health financing strategy. 14chap2_p_14As the WHO Health Financing Guide explains, effective financing systems rely on three interconnected functions:

15chap2_p_15The instruments discussed in this User Guide primarily strengthen the first of these functions - resource mobilisation - while also linking to aspects of strategic purchasing, particularly through the PPP approach and impact bonds. 16chap2_p_16It is important to emphasise that this User Guide is not a substitute for a comprehensive health financing strategy. MoHs should continue to lead on developing and updating such strategies as a roadmap toward UHC - setting priorities, defining service packages and identifying reforms that improve efficiency and effectiveness. This includes maximising the impact of existing budgets through better prioritisation, stronger budget execution and more effective provider payment mechanisms. 17chap2_p_17Ultimately, the guidance provided here is intended to complement those broader efforts - equipping MoHs and MoFs with the tools, language and frameworks needed to explore new financing opportunities, while maintaining alignment with national health goals and fiscal sustainability. |

Proposed Solutions

Overview of Financing Structures

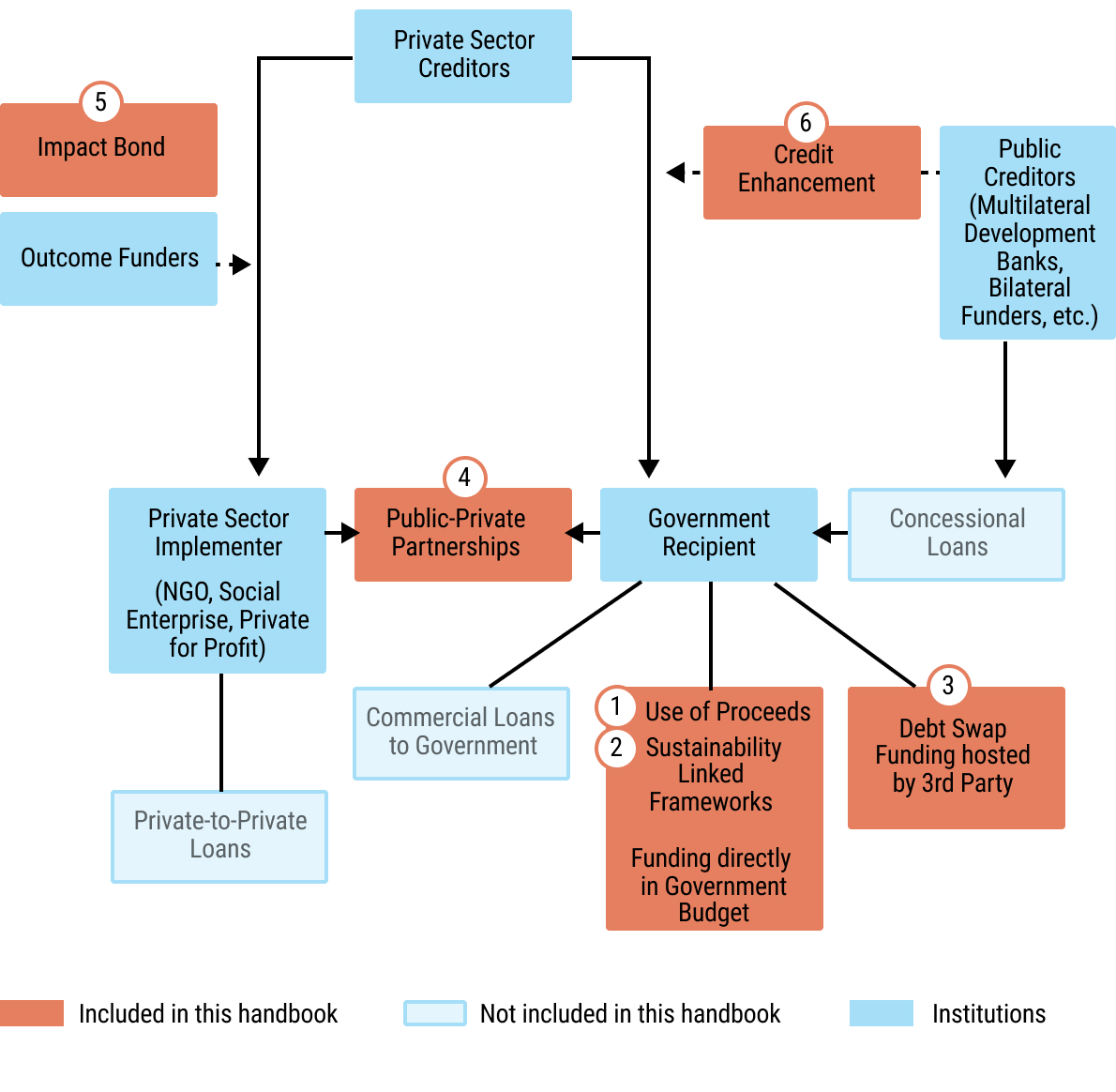

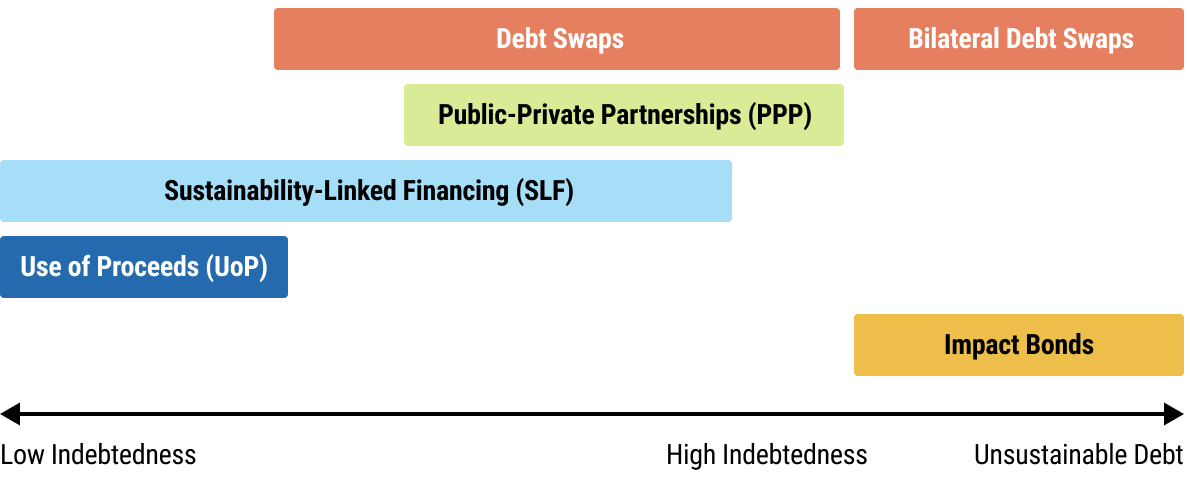

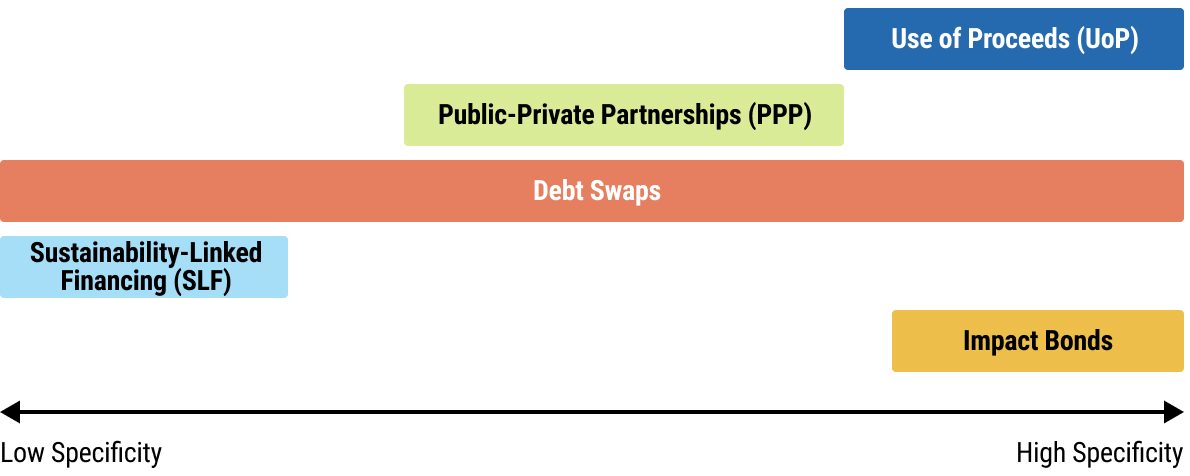

18chap2_p_18Several potential solutions exist for filling the financing gap that can be used simultaneously. This User Guide focuses on three categories of instruments, some of which have been rarely used in the health sector. However, they provide promising new opportunities for additional funding in the health sector. The User Guide does not address private funding that is channelled towards private sector implementers, but instead focuses on raising funds for the public sector. These instruments have been prioritised based on the African Legal Support Facility’s (ALSF) experience in responding to country requests for technical assistance in exploring and implementing them.

chap2_img_1

chap2_img_1

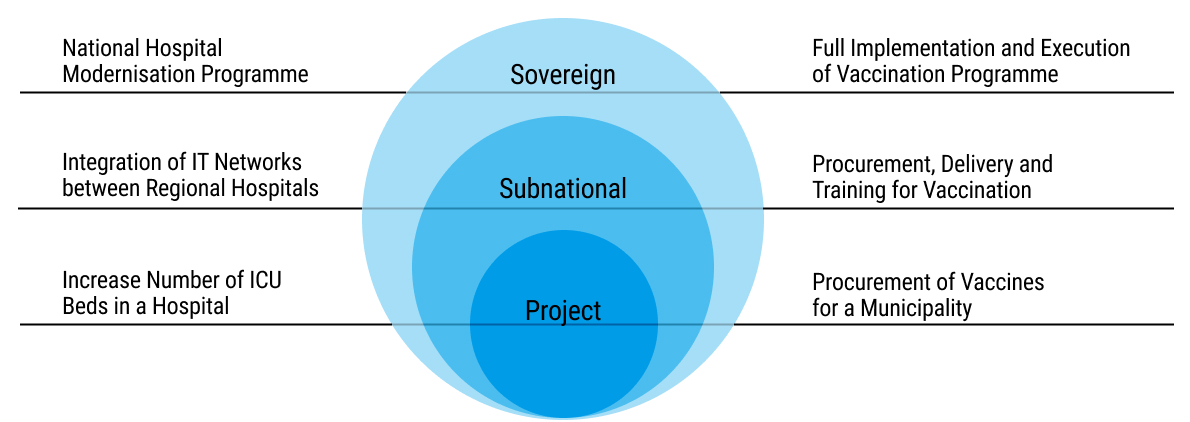

19chap2_p_19These instruments can be applied across different levels: the sovereign level (I.e. national level), sub-sovereign level (I.e. state or county level) or based on a specific project:

20chap2_p_20

chap2_img_2

chap2_img_2

Financing Instruments

21chap2_p_21Some of the financing solutions discussed in this User Guide are novel to the health sector but have already been successfully used in other sectors. For instance, sustainable financing solutions often include those focused on deforestation or renewable energy, as well as debt swaps for marine conservation or education. PPPs, in contrast, have been in use in the health sector since the 1980s but have received more attention recently.

22chap2_p_22This User Guide outlines the following instruments:

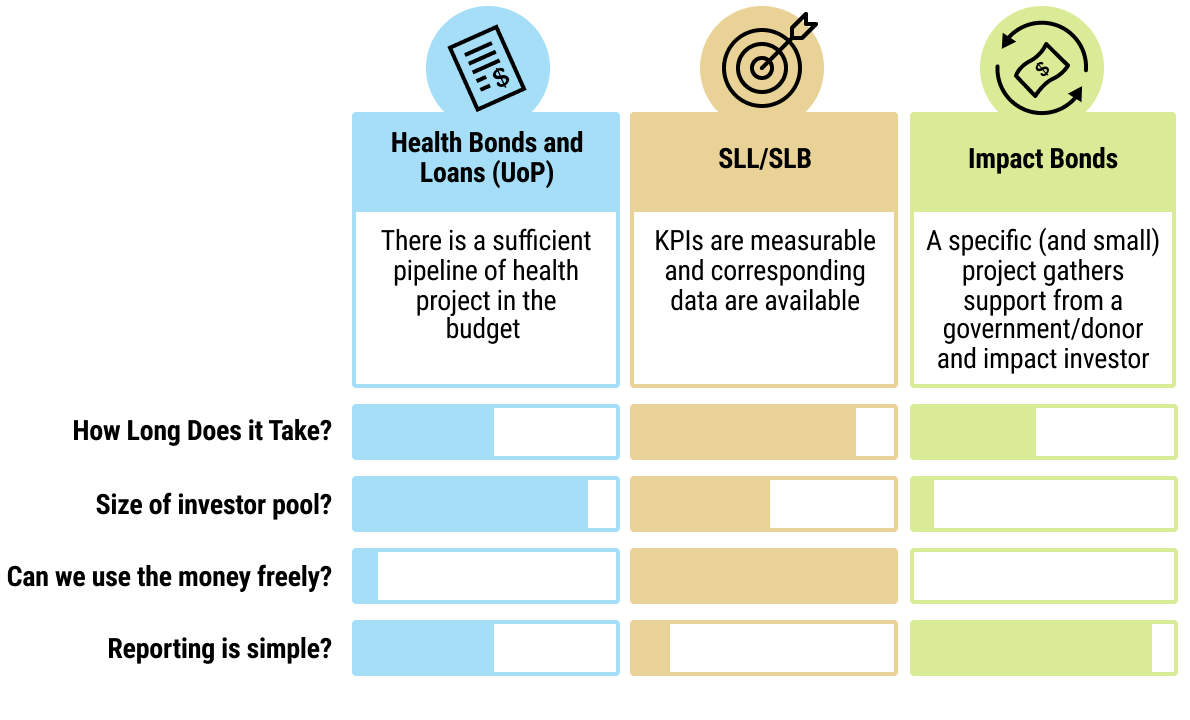

Use of Proceeds Bonds or Loans

23chap2_p_23A use of proceeds loan or bond ties financing to specific projects and expenses (see Chapter 5: Sustainable Finance Instruments for a detailed description of use of proceeds loans and bonds).

24chap2_p_24Such instruments typically follow market best practices (e.g. relevant International Capital Market Association (ICMA) and Loan Market Association (LMA) Principles), as described in Chapter 4: Health Finance and Key Performance Indicators, as well as Chapter 5: Sustainable Finance Instruments.

Sustainability-Linked Financing (SLF): Sustainability-Linked Loans (SLL) And Sustainability-Linked Bonds (SLB)

25chap2_p_25An SLF is new funding, such as a loan or a bond, that is tied to specific Key Performance Indicators (KPIs), which are the basis for setting Sustainability Performance Targets (SPTs). The proceeds from the SLF will be allocated to the general budget.

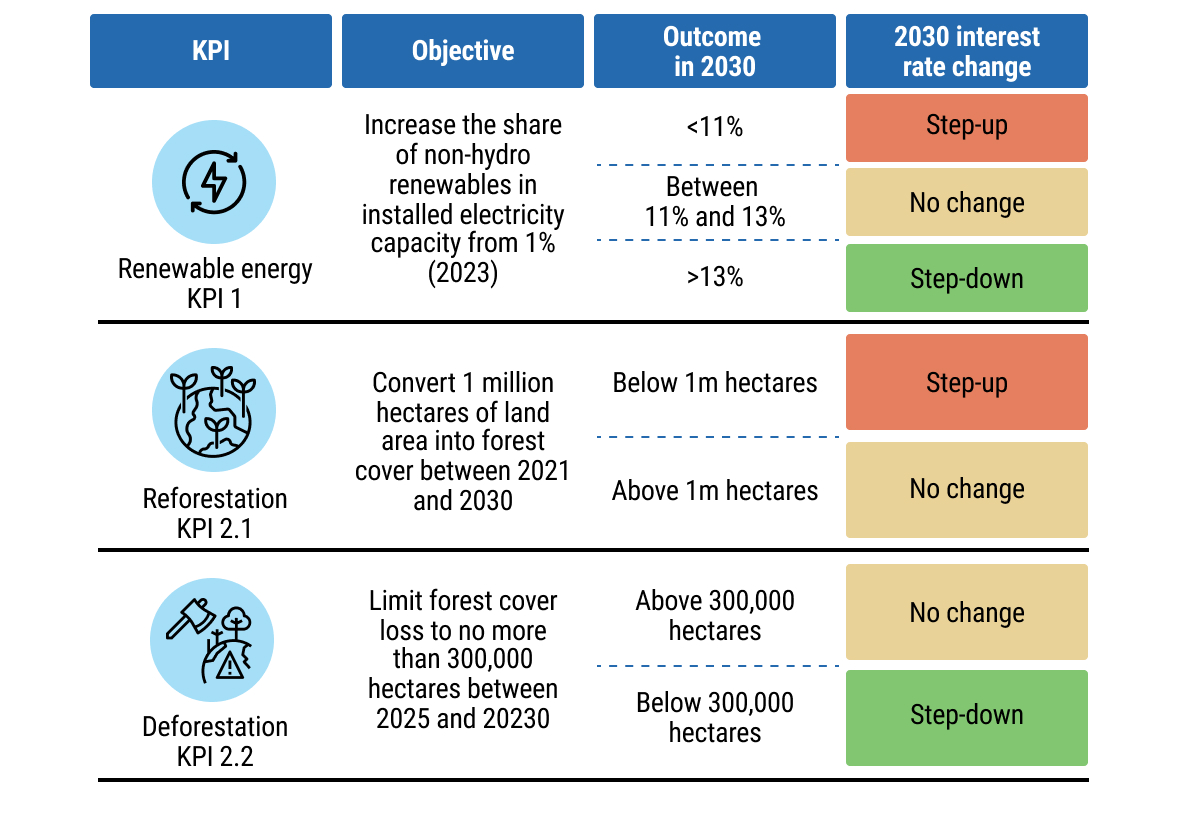

26chap2_p_26The key component of an SLF, as opposed to a plain loan or bond (the distinction between loans and bonds is described in more detail in Chapter 5: Sustainable Finance Instruments), is that the investor is interested in the country achieving agreed performance metrics. Accordingly, the level of interest payments on the instrument will increase or decrease depending on whether the SPTs are met. For example, the SLF may outline a Human Immunodeficiency Virus (HIV) prevention performance target to be achieved within 5 years. Regular monitoring will be necessary for the performance metrics, and the country may be incentivised or penalised for over- or underachieving against these targets.

27chap2_p_27Such instruments are structured in accordance with market best practices (e.g. relevant ICMA and LMA Principles), as described in Chapter 5: Sustainable Finance Instruments.

Impact Bonds

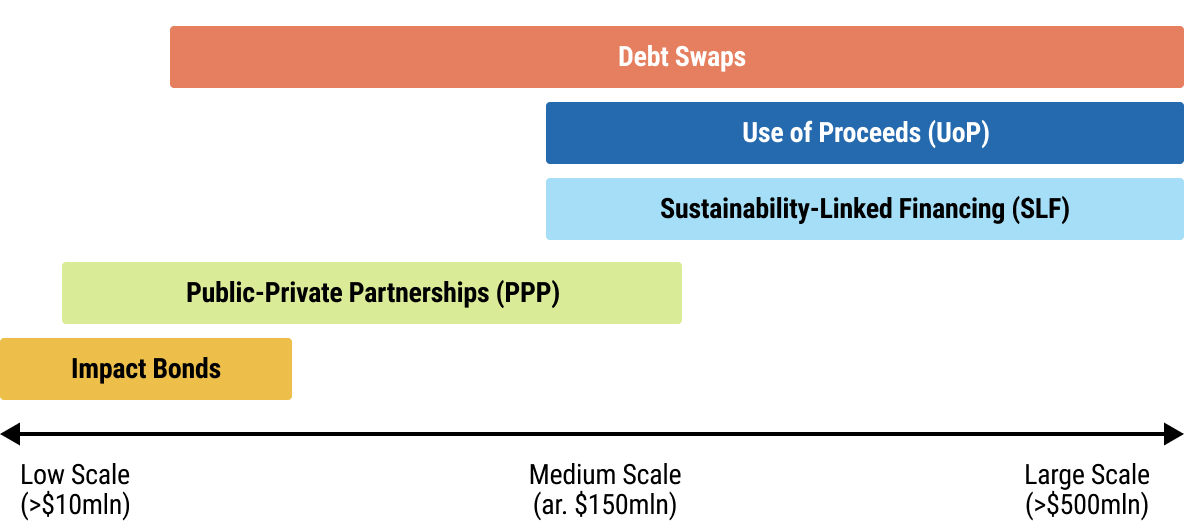

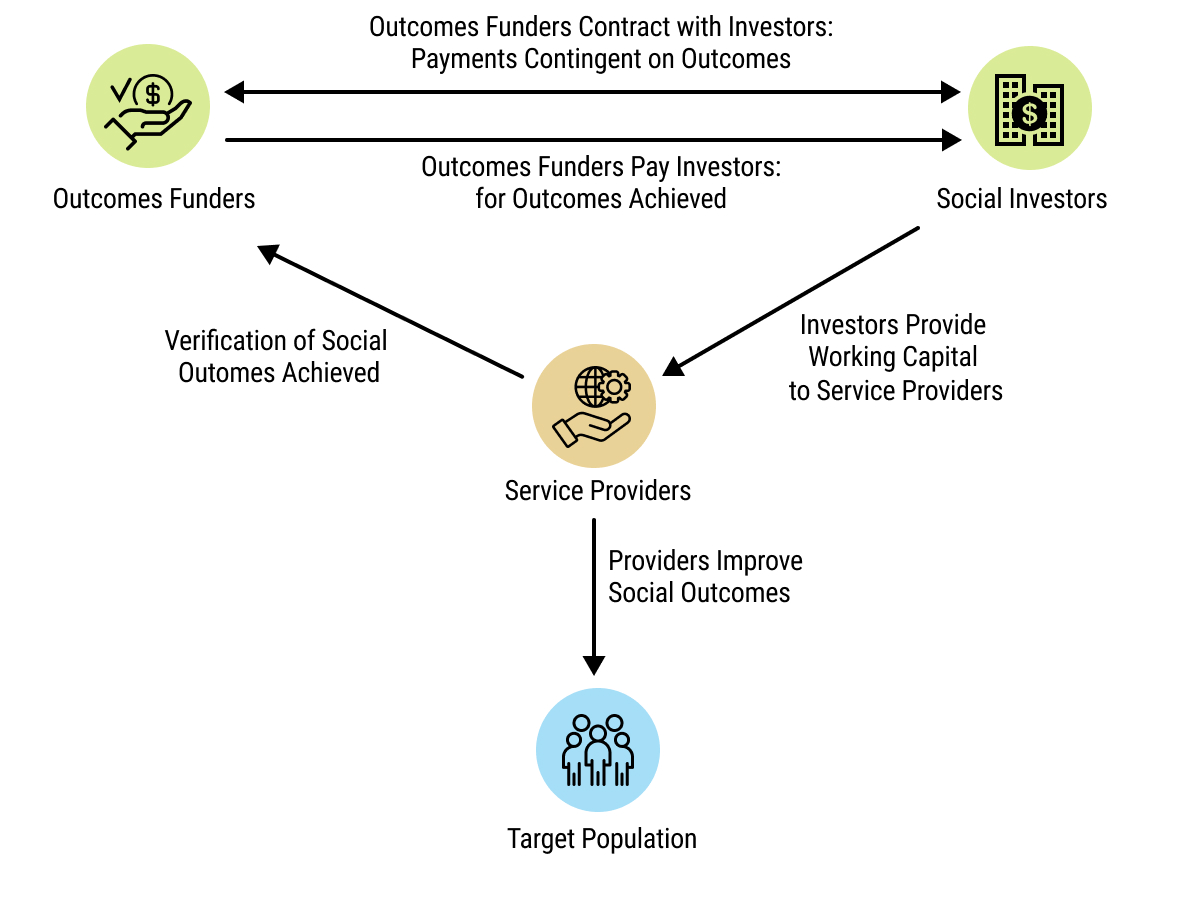

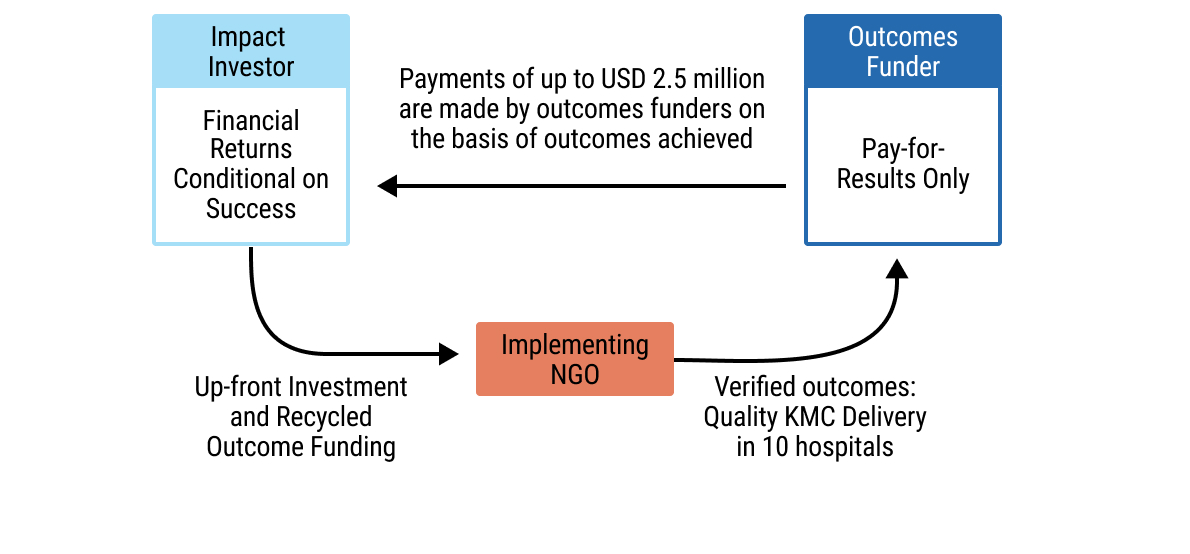

28chap2_p_28An impact bond is a results-based financing arrangement between a government or grant funder, an investor and a service provider. The investor provides upfront funding for service delivery, and the funder only pays if pre-agreed health outcomes are achieved. Although named as a “bond”, it is not a tradable instrument; rather, it is a private investment where returns depend entirely on whether the agreed-upon outcomes are met. Impact bonds are typically small in size, usually under USD 10 million.

Debt Swaps

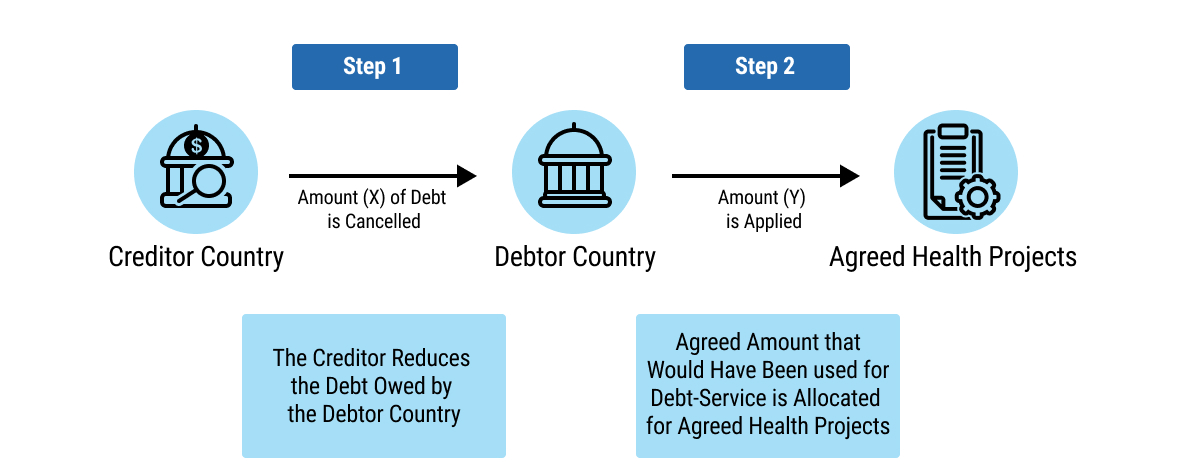

29chap2_p_29A debt swap is when part of a country’s debt is cancelled or replaced with cheaper debt, and the government agrees to use some, or all, of the money it saves to fund specific priority programmes. In effect, the transaction creates fiscal savings that are allocated to health expenditures. Debt swaps enable governments to earmark regular, predictable government spending over a long period, and are well-suited for funding long-term health priorities.

30chap2_p_30Two forms of debt swaps are covered in this User Guide:

- chap2_ol_1

- chap2_li_3Bilateral debt swaps. A bilateral debt swap is an agreement between a debtor country and a creditor government to cancel or convert part of the debt owed in exchange for the debtor investing an equivalent amount in agreed national projects or programmes.

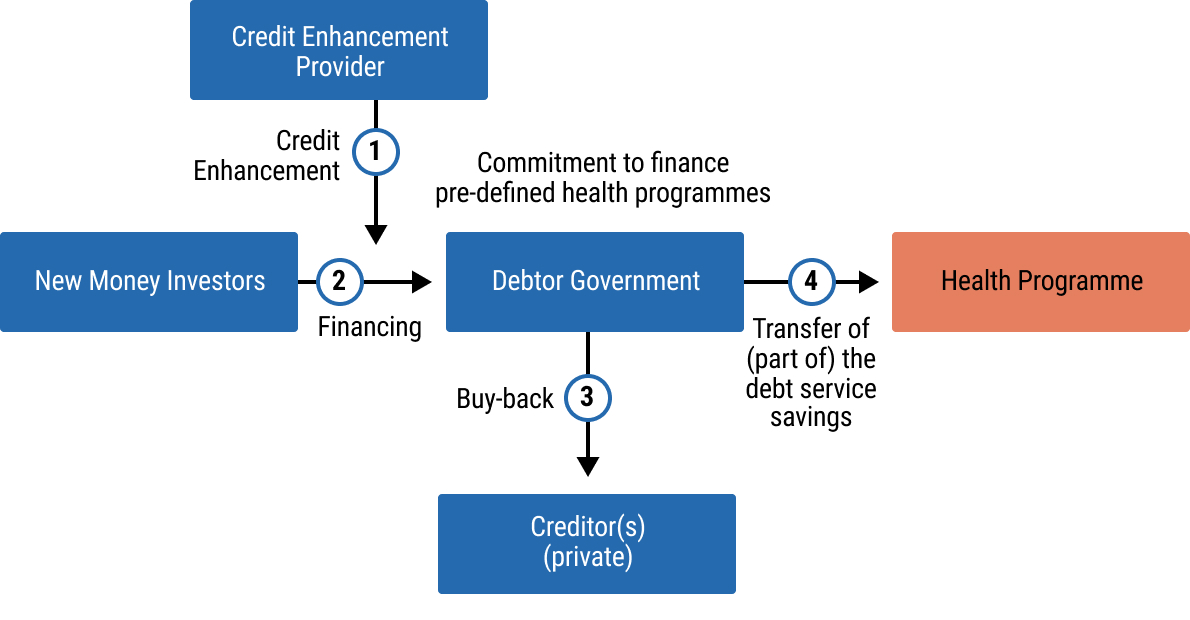

- chap2_li_4Commercial debt conversions. This occurs when private sector debt is replaced with a new instrument (e.g. a new loan) under more favourable terms. Some or all of the money saved through the lower interest rate (obtained through the involvement of a credit support provider) and potentially a debt reduction is then contractually obligated to be utilised on specific spending or outcomes.

Public-Private Partnerships

31chap2_p_31A PPP is a mechanism that mobilises private funding for delivering public infrastructure and/or services. Blending commercial funding with government grants and/or concessional loans helps improve the financial viability of PPPs where projects are economically or socially essential but not commercially attractive enough for private investors.

32chap2_p_32Financing may come entirely from public sources, such as national programmes to control infectious diseases, from private sources, such as out-of-pocket expenditure for elective procedures or dentistry and from a mix of both, such as public insurance that pays for services delivered by private providers.

|

33chap2_p_33Instrument |

34chap2_p_34Primary Objective |

35chap2_p_35Typical Scale |

36chap2_p_36Relevance to Health |

37chap2_p_37Chapter |

|

38chap2_p_38Health Bonds & Loans |

39chap2_p_39The borrowed amount has to be spent on equivalent health-related expenditures |

40chap2_p_40Medium - Large |

41chap2_p_41Incentivise the increase in the health budget |

42chap2_p_42Chapter 4: Health Finance and Key Performance Indicators |

|

43chap2_p_43SLFs |

44chap2_p_44Tie borrowing costs to measurable health outcomes |

45chap2_p_45Medium - Large |

46chap2_p_46Incentivise performance and accountability |

47chap2_p_47Chapter 4: Health Finance and Key Performance Indicators |

|

48chap2_p_48Impact Bonds |